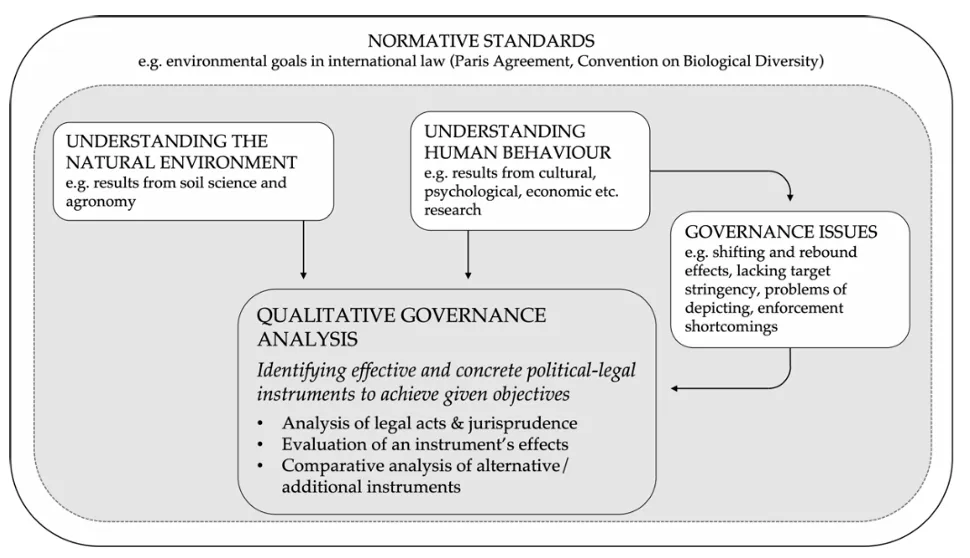

2.1. Methods

This article contributes to the interdisciplinary sustainability (and especially law and governance) literature around border adjustments. Besides legal compliance issues, it seeks to show how the CBAM adopted by the European Union in correspondence to the EU ETS scheme can meet sustainability goals set out in the Paris Agreement. To that end, we use the method of quantitative governance analysis (QGA) explained in various articles since 2018. It triangulates social sciences and natural sciences to understand human behavioral tendencies, and these lead to governance problems which, unless addressed by the policy, hinder the full scaling of a sustainability policy [

9], the following graph () explaining the QGA can be found in [

34,

40].

. Methodology of the Qualitative Governance Analysis.

First, the analysis begins with identifying a normative goal against which the policy in question, the CBAM, can be assessed (see picture above). To address anthropogenic climate change, legally binding targets (as mentioned earlier) were set in Article 2 PA to keep global warming well below 2 degrees Celsius above pre-industrial levels and preferably below 1.5 degrees Celsius [

3,

6,

35,

41]. As of now, January 2025 recorded an 1.75 °C temperature increase relative to pre-industrial times, thereby supporting the vast amount of literature evidencing that current global and national climate policies are insufficient to meet the PA goals [

1]. Assuming a high compliance probability of 83% 1.5 degrees Celsius, the remaining greenhouse gas budget for industrialized countries has already been exceeded; this applies even more if, instead of a global per capita distribution, aspects of the economic capabilities and historical climate change causation of individual states are taken into account [

3,

4,

5,

7,

8].

Furthermore, as early as 1993, the world assembled to address concerns of human activity threatening biological diversity understood as the “variability of living organisms from all sources,” including ecosystems on land and underwater and the variety of species and ecosystems under the Convention on Biological Diversity (CBD) and to state a legally binding obligation to preserve biodiversity (Article 1 and 2 CBD). However, biodiversity is still declining on a global scale. For instance, biodiversity is not sufficiently addressed as a metric in environmental impact assessments of the aluminum sector [

42]. Biodiversity is not the major topic of the present [

33,

43], but given similar drivers of destruction—fossil fuels and livestock farming [

33,

34]—and the interdependencies of climate change and biodiversity loss, we will also keep this challenge in mind in the following.

Second, the environmentally harmful effect needs to be adequately scoped. For that, a literature review on the natural scientific and economic backgrounds of three of the CBAM regulated sectors will be performed, notably focusing on GHG emissions and, to a lesser extent, biodiversity considerations of the aluminum, electricity, iron, and steel production outside of the EU. The review focuses on international scientific literature from natural science, climate change science, economic and trade literature, and product-specific literature to understand sources of environmental impacts in the production of the goods.

Third, from human sciences such as psychology, sociology, economics, social anthropology, sociobiology, and cultural studies applied in various methodological settings, we know that human behavior is driven by several key factors [

9,

34,

44]. Knowledge plays a minor role in behavioral motivation of consumers, politicians, enterprises, and other actors, while emotions are probably the most difficult to influence while having the greatest influence. Other factors include conceptions of normality, values, path dependencies, and problems of collective goods, as well as self-interest calculations [

9,

44,

45]. These behavioral analyzes lead to the below mentioned governance problems, such as depicting sectoral, special, and other shifting and rebound effects as well as lack of rigor and enforcement [

32,

33,

34]. Quantitative governance instruments directly or indirectly regulating the quantity of, for instance, emission-intensive goods can effectively address these problems while securing a high level of freedom, implementing the polluter pays principle, and maintaining cost-efficiency [

9,

32,

46]. However, this requires a thorough design. Hence, in this third step, a detailed design issue analysis will shed light on the type of instrument, scope, timing, and stringency of the CBAM [

34] (p. 9). This will then be connected with the analysis of typical governance problems identified above that will need to be addressed in order to create long-lasting impacts that further sustainability.

Fourthly, the CBAM will need to be firmly rooted in the legal context and withstand legal scrutiny to unfold its sustainable effects. Thus, a legal compliance analysis of the (contentious) compliance of CBAM with international trade law principles will be conducted. Legal interpretation of legal norms and concepts is (like ethics or practical philosophy) normative science, not empirical science. Law makes statements of ought rather than statements of being. Therefore, legal interpretation does not require experiments, collecting data and facts,

i.e., legal interpretation is not a case study as a case study empirically describes a process (see in detail [

3] also on the criticism of empiricism in epistemology that, since the 17th century, sometimes suggests that science can only deal with facts, not with norms). Legal norms are interpreted grammatically, systematically, teleologically, and historically,

i.e., according to their literal meaning, their relation to other legal norms, their purpose, and their evolution. Usually, grammatical and systematic interpretation is applied since the other two approaches have several shortcomings. In the Anglo-Saxon legal sphere, case law would also serve as an interpretation source, implying a case would, as such, be seen as a source of law, which it cannot reasonably be. This is different in the continental legal sphere we are based in.

2.2. Literature Review on the GHG and Biodiversity Impact in the Electricity, Aluminum and Iron and Steel Sectors

To understand the effectiveness of the CBAM in achieving its normative goals, the GHG and environmental problems associated with the three focus sectors need to be highlighted, also considering their societal relevance and production methods. This is essential to help the understanding of the qualitative governance analysis. The industries sourcing and processing iron and steel, aluminum, and electricity have, especially since industrialized times, led to significant improvements in all areas of life, providing infrastructure and powering industrialized nations to achieve greater levels of welfare [

47]. However, intensified sourcing and production within these sectors, alongside the effects of globalization, has led to significant global warming from GHG emissions and biodiversity loss [

29,

48]. Among the many global players who have a stake in and drive these problems, we will focus on the EU and its relationship with key importers of selected goods. EU consumption drives the use of fossil fuels globally, as the EU accounts for less than 7% of the worldwide population but for 10% of fossil fuel use [

20]. The CBAM regulated sectors account for a total of 5.3% of the EU’s imports while being among the most emission-intensive [

36]. In their relative shares, iron and steel account for 53%, aluminum for 24%, electricity for 14%, and fertilizers, chemicals, and cement jointly account for 9% of the imports covered by the CBAM [

36].

GHG emissions vary by sector and measurement. Cement and electricity have the highest carbon intensity, followed by aluminum, ensued by fertilizers and iron and steel, while scores are mostly higher for goods produced in non-EU rather than in EU countries, except for fertilizers and in the case of steel, emission intensity levels are equal (comparing OECD and non-OECD country conditions [

16,

25], for a comparison of the metal industry [

49,

50]). It is to be noted that quantifications of the electricity, aluminum, iron, and steel sector’s GHG emissions and biodiversity impact are complex and may not be generalizable due to variations. For instance, CO

2 measurements vary depending on local infrastructural availabilities and the scope and mode of assessment (see details in [

16,

42] for reviews of different studies assessing the impact of aluminum using Lifecycle Assessments), production methods, materials sourced, and environmental conditions, such as water, soil, nutrient cycles, and factor inputs [

34].

Therefore, the focus lies on environmental impacts and current global GHG emission contributions of the aluminum, electricity, and iron and steel sectors on a global scale while zooming into the local conditions of some of the largest exporters of the respective good, the source of emissions per sector and obstacles to reduce emissions and to address environmental problems (see [

51] for a detailed explanation of anthropocentric activities generating emissions and of the term of overall pollution and differences between global GHG emissions and on-site emissions). As a brief overview, China became worldwide the largest producer of aluminum after 1990, nowadays accounting for 50% of the aluminum sector’s global emissions GHG emissions [

47,

52,

53] while also being the largest producer of iron and steel, followed by an increasingly productive India in areas of both iron and steel as well as aluminum [

29,

54]. Together with Turkey, followed by the UK and India, China remains the largest importer of iron and steel into the EU [

55]. However, interestingly, when considering the impact of CBAM on countries beyond mere export volume, Ukraine emerges as the highest impacted [

55]. When it comes to aluminum, China and Turkey exported similar amounts, followed by India, the UK, and Russia into the EU [

55]. While the EU has enough productive capacity to meet its own electricity demand, it imports electricity mainly from Switzerland, Norway, the UK, and Serbia to balance the electricity grid [

55,

56,

57]. As the former three have an ETS-like system and are likely exempt from CBAM, only Serbia will be considered [

58].

2.2.1. Aluminum Production: Production, Consumption Patterns, GHG Emissions and Other Environmental Impacts

Firstly, aluminum production has the following emission and environmental effects. It produces the GHG CO

2, PFC, methane (CH

4), nitrogen dioxide (N

2O), tetrafluoromethane (CF

4), and hexafluoroethane (C

2F

6), as well as air pollutants sulfur dioxide (SO

x), nitrogen oxide (NO

x) and particular matters (PM) 2.5 and 10 [

52,

53,

59,

60,

61]. NO

x includes N

2O and NO [

62]. While pollutants and GHG emissions broadly synergize, they might vary in trends in the aluminum sector [

53]. Aluminum production is one of the two largest sources of the GHG PFC [

63]. While data on specific measurements of PFC of EU imports, for instance, is scarce

, total global emissions from aluminum production in 2024 reportedly rose to 5853.947 kt CO₂e of PFC [

64,

65]. The direct and indirect CO

2 emissions of the aluminum sector accounted for 1 GT CO

2 of 36.5 Billion Tonnes or Gt in 2022, representing 2.7% of global carbon emissions [

66,

67]. GHG emerged during the refinement of bauxite ore to gain alumina via the Bayer process, accounting for 166 Mio tons of CO

2 e, and electrolysis using the Hall-Héroult process, which was responsible for 791 Mio tons of CO

2 e in 2023 [

49,

53,

68,

69]. The largest shares of direct CO

2 are emitted during the refining and smelting of aluminum and during anode production, while most PFC emerges during “anode events” [

59,

66,

69]. At the same time, reliance on fossil fuels in the generation of electricity and thermal energy for energy-intensive steps in primary production like aluminum refinement and electrolysis drives its high indirect emissions [

42,

47,

66,

70,

71]. Even if aluminum is a highly recyclable property, incurring only 3–5% of the primary production’s emissions, reliance on fossil fuels keeps indirect emissions below the best possible emission level, and limited availability of scrap from in-product aluminum is a major limitation to recycling becoming the modus operandi of aluminum production [

66,

72]. Of course, aluminum cannot be endlessly recycled. Detailed information on recycling rates and share of aluminum being still in use in [

72]. Moreover, the nature of recycled aluminum substantially influences the GHH emissions of the produced aluminum. When scrap is sourced from industrial production (so called pre-consumer or process scrap), its GHG emissions are equal to aluminum from primary production, whereas post-consumer scrap incurs considerably lower emissions and is thus recommended for a carbon-free future [

73,

74]. In addition, demand for (primary) aluminum will continue to rise [

75], partly because it is a commodity most commonly used in the EU for mobility, construction, building, and packaging [

42,

50,

75], but also since clean energy technology is increasingly adopted [

72,

76]. While institutions like the International Aluminum Institute find that increasing demand has not provoked a gain in total CO

2 emissions due to reduced emission intensity [

77], for global warming to stay below 2 degrees, a 77% reduction of emissions remains necessary [

50]. The literature suggested adopting technologies such as well-tested clean energy sources (

i.e., hydrogen) during the mining activities [

69], reuse of waste heat emerging from the smelting [

78], and adopting energy-efficient production processes (such as hydropower) during the aluminum electrolysis (details in [

79]).

Aluminum production has considerable non-GHG environmental impacts. It requires high freshwater consumption [

78] and is responsible for air pollution [

79] (SO

2, Nox, and PM) [

53], which is problematic as more than 75% of primary aluminum is produced in developing countries [

80], increasing local water scarcity and amplifying air quality problems [

53] partly because of lower regulators standards and less emission efficient production technologies [

52]. Besides energy consumption and GHG emissions, health risks from air pollutants (such as premature deaths, diseases,

etc. [

53], deforestation of native and tropical rain forests, dust and noise leading to (among others) habitat destruction during bauxite mining, disposal of bauxite residues, liquid effluents, and solid waste from smelting and recycling are essential environmental and biodiversity related concerns [

81].

2.2.2. Electricity Production from Coal, Oil and Gas: Production, Consumption Patterns, GHG Emissions and Other Environmental Impacts

Secondly, the electricity sector produced 13.8 Gt CO

2 in 2024, accounting for 36.9% of total annual emissions in 2024 [

67,

82]. Emissions from electricity generation vary by the type of technology and fuel employed in the process and the technologies’ respective thermal efficiency, being the amount of fuel necessary to generate 1 kWh of electricity and the load factor [

83,

84]. Especially non- CO

2 emissions are dependent on the type of instrument utilized [

85]. Globally, fossil fuels dominate, with oil (30%), coal (28%), and natural gas (23%) supplying 81% of the energy supply in 2022 [

86]. The three main importers into the EU reflect this trend, while Serbia relies mostly on fossil fuels (a total 84.2% of the total energy supply in 2022 was generated based on fossils) [

87] (for an overview of this trend is reflected in the other countries [

88,

89])] In Serbia, coal, oil and gas respectively contributed 60%, 23.3% and 14.5% to Serbia’s total CO

2 emissions in 2024 with coal having the highest emission intensity of 25.26 Mio tons, oil 9.87 Mio tons and gas 6.14 Mio tons [

90]. Generally speaking, emissions arise during fuel provision, including mining, plant operation, such as combustion and from infrastructure [

91], and to reduce GHG emissions, energy efficiency must be increased and its use rationalized, while the share of energy from renewable sources must rise [

92]. However, due to common usage and the need for a reliable energy supply, the electricity sector, just like the steel and iron sector, remains “difficult-to-decarbonize” [

93] (p.1).

Electricity generation from the different fossil fuels generates GHG and environmental impacts as follows. During the generation of electricity from coal, coal combustion is responsible for the largest shares of direct CO

2 emissions but also smaller amounts of N

2O and marginal amounts of sulfur hexafluoride (SF6), PFC and hydrofluorocarbons and air pollutants, including SO

x and NO

x, while the mining operations consume large amounts of energy, emit PM and heavy metals such as mercury and potent CH

4 emissions [

84,

91,

94,

95,

96,

97]. Measures to reduce GHG and pollutant emissions include the adoption of modern technology with lower GHG emissions, such as coal gasification, selection of lower emission-intensity fuels, and proper administration of flue gas cleaning and energy recovery [

91,

94,

98]. Moreover, environmental concerns from coal-powered electricity production are residues of solid waste in the form of different ashes [

97]. Also, the mining operations (of coal and gas) cause coal to have high marine and freshwater aquatic ecotoxicity potential [

99]. Moreover, heavy metal emissions to the air and soil of coal (but also gas) present an ecotoxicity risk to terrestrial life [

99].

Electricity generation from crude oil or comparable petroleum products releases CO

2 and SO

2 (from fuel provision, see [

91]) during the combustion process, with diesel combustion being the largest source of CO

2 among all fossil fuels and large energy consumption during the extraction process [

94,

96,

97]. Moreover, the release of fine particulates increases the risk of respiratory problems [

97]. Crucial for mitigating GHG emissions is the type of energy recovery system under use since the base load power plants have 30% to 40% more energy recovery efficiency than peak load power plants, which therefore have overall higher GHG emission scores [

91]. Currently, there is little other options besides the use of diesel, which is widely available [

97].

Electricity production from natural or liquefied natural gas is less carbon emission intensive than coal-powered electricity generation and has been suggested as a measure to reduce Serbia’s GHG emission footprint [

92,

97]. Yet, during gas extraction MH

4 and CO

2 emerge, while during liquidation and transport of LNG processing, even higher GHG emissions emerge, accompanied by high water consumption and freshwater toxicity, which is challenging for water-poor regions [

91,

97]. For natural gas, most studies found large shares of energy consumption and CH

4 emissions occurring also during extraction and transportation of the fuels provided for the processes [

91]. Overall, the amount of air pollutants and emissions depends on the energy efficiencies of different turbines essential in electricity production [

91]. Lastly, electricity generation from nuclear power, which, albeit rare, is under common use in major importing countries like Switzerland. Numerous studies have found that nuclear reactions themselves are carbon neutral, while the processes of refining uranium ore and powering and constructing nuclear reactors composed of steel and cement produce large amounts of CO

2 ([

89,

91], see review in [

96]).

2.2.3. Iron and Steel Production: Production, Consumption Patterns, GHG Emissions and Other Environmental Impacts

Thirdly, iron and steel production releases GHG emissions such as CO

2 and air pollutants such as sulfur dioxide (SO

x), nitrogen oxide (NO

x), and particular matters [

100]. Globally, iron and steel constituted 8% of the global energy-related GHG in 2023 (WEF, Net Zero Industry Tracker, 2023), accounting for 8% of total final energy use in 2021 with an expected increase as demand rises over the next years [

51,

54,

100]. In the steel sector, direct emissions from primary iron-making account for at least 80% of the total CO

2 emissions ([

21] and (WEF, Net Zero Industry Tracker, 2023)). After the industrial revolution, the sector turned from renewables to relying heavily on fossil fuels such as coal and natural gas to generate the high temperatures needed for steel production, resulting in high indirect emissions [

51,

54,

93]. Steel demand is constant and rising in reflection of trends in the aforementioned goods. On the one hand, steel and iron are commonly used in the construction sector [

21], while on the other hand, global demand rises as emerging countries’ domestic demands in India increase in the coming years [

54]. To reduce emissions, the literature supports the adoption of “breakthrough” technological innovation, for instance, by using electric arc furnace (EAF) to recycle scrap steel for secondary steel production [

101] (p.4), which, if fueled by clean hydrogen or electricity, yields the potential for drastic CO

2 reductions. Yet, this method is only marginally used and continues to face infrastructural, competitive, and financial hindrances, for instance, as it cannot supply the high-temperature energy needed for steel production and continues to be pricy [

51,

54,

93,

102,

103,

104,

105,

106]. For instance, EAF accounted for only 23% of global steel production in 2017 and decreased to 10% in China due to a lack of scrap [

107]. Importantly, the GWO of scrap steel recycling depends on the share of ore-based inputs and the electricity mix [

108]. While heat reduction during the process seems impossible, CO

2 reductions from efficiency improvements have reached the optimum in several places [

51,

54,

109].

While the recycling of scrap seems as equally necessary as breakthrough technologies [

101], scrap availability is limited as scrap supply grows at a slower pace than steel demand [

54,

109] so that, in sum, the sector has yet failed to meet the 50% reduction in direct CO

2 emission target to reach the PA goals [

54,

110]. In addition to high energy consumption and GHG emissions, the toll of steel and iron production on the environment and biodiversity is considerable; notably as contaminated waste from mining, after breaking dams, led to several environmental disasters polluting water systems, ecosystems, and land [

51,

111]. The surroundings of steel factories also record continuously elevated levels of heavy metal contamination in soil, air, and water [

54,

112]. Moreover, in China, for instance, the steel industry is the biggest industrial source of air pollutants, resulting in major health hazards [

51,

54].

Overall, it has been held that technological advances can, to certain degrees, reduce direct and indirect emissions of the three sectors. However, financial and competitive barriers, as well as, increases in demand, often prevent our out scale the potential effects of such large-scale implementations of such measures [

93]. Thus, frugality changes such as coordinated integration and coordination of operations among the providers of the three goods may seem necessary [

9,

93]. Frugality measures can be realized using various policy measures, especially an ambitious ETS, and which bears the question of to what extent challenges regarding competitiveness will be addressed under the CBAM.

3.1. Qualitative Governance Analysis

Cap-and-trade schemes and tariffs are economic instruments directly or indirectly regulating the quantity of (emission-intensive) goods and can effectively address governance problems [

9,

32]. However, the extent of governance problems avoided and, eventually, the degree to which a given policy achieves its sustainability goal depends on the choice of an appropriate design involving scope, methods for assessing carbon contents, the ambition of the cap, and utilization of the revenues of the carbon border tax [

32,

113]. The instrument’s coverage, stringency, and timing influence rebound, enforcement, and sectoral, geographic, or resource related shifting effects, such as carbon leakage [

9,

114,

115]. Furthermore, problems of depicting and lack of ambition through overly broad terms, loopholes, and exemptions further limit the effectiveness of any sustainability economic instrument [

32,

34]. Overall, the wider the sectoral and geographical scope, including upstream production, the more ambitious the caps and the easier governance units can be grasped, the more effective will be a quantity regulating economic instrument [

9]. This bears the questions: what does this mean with regard to CBAM?

3.1.1. CBAM as Quantity Governance Instrument

First, the CBAM in the CBAM Regulation is an economic instrument regulating quantity to reduce carbon leakage and thus level the competitiveness playing field. The four main policy instruments of environmental regulation are regulatory or “command and control” instruments, voluntary and educational measures, as well as subsidies and market-based or economic measures, and CBAM belongs to the latter [

46,

116] (on the regulatory nature Recital 20 CBAM Regulation, CBAM Proposal [

117]). Among the economic instruments, CBAM can be considered as an additional carbon regulation [

115,

118] and will require importers of goods into and sold in the EU domestic market [

119] to pay a price equal to the ETS imposed by the EU domestic carbon price for the embedded emission arising during the production process upon import beginning 2026 (Article 1 (1), Article 2, Recital 15 CBAM Regulation [

120,

121,

122]). Thereby, if properly designed, CBAM will regulate quantity and impose indirect price pressure on the norm addresses, which are in line with the principles of liberal democracy and guided by the polluter pays principle, free to choose flexibly between efficiency, consistency, and sufficiency [

9,

32,

118].

3.1.2. Depicting, Shifting, and the Relevance of Scope and Governance Units

Second, the scope of CBAM includes its norm addresses, carbon content, sectoral and special scope, and governance units. The literature holds that, generally, the extent to which CBAM captures carbon and a wide range of products while putting an adequate price on imports is key to preventing shifting effects as well as challenges for competitiveness [

118]. The norm addressees included in the scope of CBAM [

35] are any global importers of cement, electricity, fertilizers, iron and steel, aluminum, and hydrogen (Recital 27 CBAM Regulation) [

120,

123] or processed products containing these goods, when they are imported from third counties into the customs territory of the Union including any other structure in the exclusive economic zone (12 miles) of a Member state of the European Union, which is bordering said customs territory (Article 2, Recitals 18, 32–40, Annex I CBAM Regulation). The scope of CBAM is thus sector-specific, targeting the industries of “utmost concern” [

118,

124] (p. 238), and is intended to be gradually extended beyond the six emission-intensive sectors prone to carbon leakage to including other sectors and products vulnerable to this problem (Recital 13 CBAM Regulation) [

120] eventually meeting the sectoral scope of the ETS Directive by 2030 to include more emission-intensive sectors (Recital 67 CBAM Regulation) [

28,

123]. Though, there remains criticism from civil society organizations about the scope of CBAM not being expansive enough [

120,

125].

The governance units of the CBAM are GHG emissions of the different goods expressed in CO

2 equivalents (Annex IV CBAM Regulation), together with the GHG measurement procedures, which are essential to addressing the governance problem of depicting. This problem describes the challenges of determining and quantifying the amount of GHG of a specific good and, if not addressed, is inducive to other governance problems such as carbon leakage or shifting effects [

126]. Hence, the question is which GHGs are included in the scope of the CBAM and to what extent the measurement mechanism proposed accurately captures the GHG emissions of the goods of the three sectors aluminum, steel and iron as well as electricity.

The GHGs included in the scope of CBAM are carbon dioxide (CO

2), nitrous oxide (N

2O) and perfluorocarbons (PFC), which is a long living and highly potent GHG (around 7000 to 11,000 times the strength of CO

2) (Annex IV CBAM Regulation) [

63,

127]. More precise definitions of goods, of the goods falling under the sectors and methods of emission calculation emissions are specified in the Implementing Regulation of the CBAM (Article 7 (1)–(4), Recital 7 (a), Annex IV, CBAM; Annex II and III CBAM Implementing Regulation, as relevant to the calculation of embedded emissions of complex goods, Amendment No. 3 of the European Parliament changing Annex IV, point 3, para. 1, subpara. 5 [

38]). These GHGs have different global warming potentials (GWP), that is, the amount of energy that 1t of a specific gas emitted will absorb in x time, compared to 1t of CO

2 [

128]. CO

2 has a GWP of 1, whereas N

2O has a GWP of 273 for 100 years, and PFCs range between 0.0004 and 12.400, with overall at least 7.380 [

129]. It can be criticized that together with other potent emissions and air pollutants arising from the production of iron and steel, aluminum and electricity, methane, the second largest GHG after CO

2, which accounts for approximately 30% of global warming with a GWP of 29.8 [

129] is not included in the scope, especially, as 40% of total methane emissions are attributable to the energy sector (which is limited to CO

2) [

86]. This seems largely at odds with the GHG included in the scope of the EU ETS, which also covers Methane, Hydrofluorocarbons (HFCs), and Sulphur Hexafluoride (SF6) and bears the question to what extent imported products receive differential treatments (Annex II, ETS Directive). Moreover, despite extensive research on GHG emission measurements, the problem of accurately depicting GHG persists. Notably, because emission measurements depend on a variety of factors beginning with the methodology [

48], conditions of the production site such as type of fuel, climatic circumstances, and technology [

83]. Furthermore, due to lagging infrastructure, high-quality measurement and reporting of indirect emissions is limited in several countries [

130].

It becomes relevant then to ask how GHG measurement is operationalized in the case of the CBAM. The CBAM covers simple goods, where only input materials are required during the production process, or complex goods (Recital 7 (a), Annex IV (1)). The amount of CBAM certificates depends on imported goods’ embedded GHG emissions (Article 1 CBAM Regulation) [

20,

131], meaning the direct emissions arising from the production process until the import and indirect emissions generated from the electricity input during the production process calculated based on default values (Articles 2, 7, Recital 19 CBAM Regulation) [

124]. Embedded emissions should be actual, and for simple goods, that means the sum of direct and indirect emissions attributable to the installation where a good was produced divided by the amount of goods produced in the installation (Annex IV, 2 CBAM Regulation). In the case of complex goods, the relevant embedded emissions of input materials are also added to the attributed emissions (Annex IV, 3 CBAM Regulation). After the amendments, this calculation no longer includes input materials as relevant to the system boundaries of the production process but only those precursors as listen in Annex I and originating in countries other than those excluded pursuant to Annex III point 1 [

38]. Currently, the majority of emissions are captured at the production level and upstream emissions, which is recommended, while in the future, the emission from downstream production may be covered more extensively (Recital 28 CBAM Regulation; exemptions apply for aluminum and steel precursors’ embedded emissions, see below and Article 1 (5), Recital 13 Proposal for CBAM Regulation Amendment). A major critique points to the limited coverage here: currently, these conditions make that no semi-finished or finished goods are included while, especially, semi-finished products in the steel sector [

132] are prone to carbon leakage [

133]. Importantly, by dispensing with the production process system boundaries, the CBAM excludes and makes the calculation of embedded emissions of complex goods less flexible or adaptive and more shoe-box based. It will be questionable whether this simplifies a challenging process of calculating emissions or whether it makes the CBAM less ambitious and more vulnerable to circumvention practices. The CBAM avoids the common challenge of defining what a direct emission is, as it accumulates the emissions from different outlined production steps, and it will be the importers’ duty to report and verify emissions (see more here [

134]). Moreover, emission measurement is facilitated for emission-intensive and trade-exposed sectors covered in the initial phase, where publicly available data is readily retrievable [

135]. Additionally, the CBAM’s focus on GHG emissions other than exclusively carbon emissions and the inclusion of process emissions in addition to combustion emissions, if correctly monitored, yields large potential in terms of accurately depicting and preventing carbon leakage for a more complete carbon pricing [

135,

136]. However, a major limitation to the boundaries of GHG measurement during the initial phase of the CBAM is, that the exclusion of indirect imports also excludes a majority of imported fossil fuel from being captured by CBAM [

16,

20]. While focusing on capturing the direct emissions of such energy-intensive sectors seems intuitive, this risks incentivizing carbon leakage by outsourcing energy production [

131,

134].

However, where actual emissions cannot be determined and for the calculation of indirect emissions, default values grounded in the “best available data” should be used (Article 7, Annex IV, 4 CBAM Regulation). Following the Commission Amendment Proposal, default values will be calculated based on the “average emission intensity of the ten countries with the highest emission intensities for which reliable data exists” [

137] (p.21). This thus marks a departure from hybrid country-and-goods and installation-based tariffs to a purely country-based one-for-all tariff (Annex IV (4) CBAM Regulation), which simplifies reporting, is less cost-efficient globally and more vulnerable to carbon leakage [

18,

118]. Moreover, reliance on default factors can diminish incentives to invest in clean energy technologies and risk distorted end results [

138]. However, under the amendments, importers will be able to choose between calculating actual embedded emissions or using such default values with a markup, which might yield incentives to prove individual actual emissions along the argumentation of an “individual adjustment mechanism” proposed by Mehling and Ritz [

137,

138].

The calculation of emissions is delineated for aluminum, steel and iron as well as electricity, complex goods, goods with precursors subject to the ETS and upstream aluminum, iron and steel production stages. In the cases of aluminum, iron and steel, as well as electricity, only direct emissions are included (Annex II CBAM Regulation). To further narrow down the emissions of electricity captured by the CBAM, under the Parliament Amendments No. 1 and 2, electricity generated in the exclusive economic zone of an EAA Member State or upon direct import into the Union customs territory was excluded from the CBAM scope (Article 2 para. 3b new) [

38]. Direct emissions of electricity include carbon emissions from the combustion of carbon containing fuels (incl. waste; Annex III. B.9.1. CBAM Implementing Regulation; Article 1 (26) Proposal for Amendment of the CBAM Regulation; see also [

137]) and process emissions from flue gas treatment calculated based on default values (Annex II, 3.19. CBAM Implementing Regulation). The exclusion of indirect emissions, in addition to wider use of countries-specific default values, makes the CBAM more vulnerable to cost-shifting and has more negative repercussions for the importers ‘competitiveness and welfare [

18]. To avoid double counting, the embedded emissions of complex goods should not include embedded emissions of any precursor or input material if they are subject to an EU ETS or comparable price systems fully linked with the ETS (Article 1 (27), Recital 14 Proposal for Amendment of the CBAM Regulation; [

137]). Also, the manufacturing (upstream) stages of some aluminum and steel goods will be excluded from the calculation of actual embedded emissions (Article 1 (13), CBAM Amendment). The rationale, according to the Commission, is that the administrative burden of operators can be reduced because embedded emissions from precursor production, such as bauxite mining and refinement, contribute to the largest extent to the actual embedded emissions of the imported good while the later manufacturing stages have only minor emissions [

137] (pp. 21–22).

The scope of CBAM is subject to some further limitations. On the one hand, CBAM’s reporting duties will be largely eliminated for small importers (such as individuals and SMEs) of goods below accumulated 50 tones net mass or less than 100 tones of embodied CO

2 emissions annually in the four sectors of iron and steel, aluminum, fertilizers, and cement but not electricity and hydrogen (Article 1 (1) (b) Proposal for CBAM Regulation Amendments) [

137,

139,

140,

141,

142,

143]. The reason was that the baseline expectation of the number of importers subject to CBAM turned out to be 10 times too low. Instead of 20,000 importers, 200,000 were included in the scope of CBAM [

137] (p.4). Under the Amendment, the overly large group of addressees will be reduced to facilitate enforcement, exempting 90% of the SME importers and narrowing down the applicability of CBAM to the largest emitters among the importers, thus keeping the scope of embodied emissions covered at 99% and replace the existing exemption of goods below 150 euro thus using a better proxy for embedded emissions than monetary value as previously envisioned [

137,

140,

141,

143]. Moreover, large CBAM importers will be able to delegate the capacity to submit CBAM declarations to a third party [

137].

On the other hand, CBAM lays out exemptions from the purchasing and surrendering obligation of certificates under three conditions. First, importers from countries where a carbon tax, which is linked to the EU ETS system, results in a carbon price being “effectively paid” on the good are exempted or receive reductions (Article 2 (6) (a–b), Recital 16 CBAM Regulation, see also Article 1 (26) Proposal for Amendment of the CBAM Regulation) [

144]). The wording of “effectively paid” currently lacks clarity [

145] and likely excludes any non-market based measure and “positive indirect carbon pricing” while welcoming command and control measures as long as any of these are oriented towards the carbon amount of the product and thus more easily verified [

146,

147] ([

148] (p.173)). Alternatively, exemptions apply until 2030 and under specific conditions where an electricity market is fully integrated into the Union’s internal market and where technical hindrances obstruct the application of CBAM (Article 2 (7), Recital 56 CBAM Regulation, see also Article 1 (26) Proposal for Amendment of the CBAM Regulation). Lastly, CBAM declarants are exempt or receive reductions when they have “effectively paid” a carbon price in the embedded emissions country of origin, which may soon also apply to importers of goods who have effectively paid a carbon price in third countries other than the country of origin of the imported good (Recital 17 CBAM Regulation). An annual default average carbon price will be calculated for such a third country to alleviate the burden of companies to calculate the countries price (Article 9 (1), Recital 46 CBAM Regulation; Article 1 (7) Proposal for Amendment of the CBAM Regulation) [

140,

148]. Reporting duties accompany all three circumstances (Article 2 (8), Article 9 (2)–(3) CBAM Regulation).

3.1.3. Level of Ambition and Timing of Introducing Tariffs

Third, the timing of introducing tariffs like CBAM matters [

114]. CBAM targets the sectors with the highest potential for impact. First, that is, the greatest risk for carbon leakage, and the regulatory grip tightens from reporting only to the duty to surrender certificates (Article 1, Recitals 30–32 CBAM Regulation) [

124,

149,

150]. Concretely, importers of emission-intensive goods are beginning to become acquainted with CBAM during the transition phase, which started in 2023 and ends in 2025, in which they have to report the embedded emissions of their imported goods (Article 32, Recital 44 CBAM Regulation) and during which reports and amendments concerning products down the value chain can be proposed (Article 30 (3)–(4) CBAM Regulation) [

145]. During its “definitive phase” beginning in 2026, authorized CBAM declarants will be under a certification obligation. That is, they are allowed and required to purchase and submit CBAM certificates to the importing authorities for the preceding year until February 2027 (Articles 4–6; Article 22 (1), Recital 45–48 CBAM Regulation; Article 1 (14) Proposal for Amendments of the CBAM Regulation) [

30,

141,

149,

150,

151].

Article 31 qualifies Article 22, as CBAM certificates are allocated free of charge in correspondence to the gradual phase-out of free allowances available to European producers in the six emission-intensive sectors under the EU ETS until 2034 to avoid favorable treatments of Union goods over imported goods (Article 31 (1), Recital 12 CBAM Regulation) [

30,

36,

119,

149]. Moreover, special regulations apply depending on the nature of the imported goods and importer (

i.e., “processed goods resulting from the inward processing procedure” and “indirect customs representatives” appointed by the importer) (Article 34 and 35 CBAM Regulation). However, the delayed implementation nine months later than initially suggested by the European Commission in conjunction with the postponed end of the phaseout of the ETS free allowances by 2034 and the recent 1-year delay in the purchasing obligation will push back the point of full effectiveness of CBAM [

35,

119,

151].

3.1.4. Level of Ambition and Target Stringency

Fourth, an important design aspect of carbon tariffs is their level of ambition or the lack of target stringency [

115,

126]. Authorized CBAM declarants (or their direct customs representative) pay a price that depends on the actual embedded emissions of the imported goods and the weekly average of the ETS allowances auction. Thus tariff differentiation occurs only in relation to actual emissions and not based on the sector or country of origin (Article 21, Recitals 49, 28 CBAM Regulation) [

124]. CBAM declarants can apply for reductions received as outlined above to prevent double counting. Moreover, the CBAM certificates cannot be banked and traded, which would incentivize the storage of credits to delay emission reductions. Excess certificates can be repurchased (Article 23 CBAM Regulation) while on the 1 July of every year, all certificates remaining on the CBAM declarant account are cancelled (Article 24 CBAM Regulation).

As the price paid by importers depends on actual emissions, and as they will be able to choose between the application of default values or calculation of actual embedded emissions, assuming that the former is high enough, they are incentivized to reduce emissions [

16]. When considering the price elasticity of carbon leakage, with increases in carbon price, the marginal reactivity to the adjustment and the marginal reduction in emission rises but then declines, indicating that higher prices are not necessarily more effective [

152]. Overall, the literature agrees that to equal competitiveness, the price must be equal to the difference between the regulated and unregulated regions or countries carbon prices [

96]. Yet, this would pose problematic in a later WTO law analysis where it is essential that the environmental goal of the CBAM is implemented before and only realized by levelling out competitiveness. Thus, other studies may be worth considering, which find that the price must be high enough relative to the social cost of carbon and the fuels under taxation, which is not fully accounted for under the CBAM and would necessitate a near skyrocketing price increase [

153]. This may again be problematic from a WTO law perspective, pointing out that a legally compliant CBAM may not always be the most environmentally effective [

154].

3.1.5. Enforcement Problems

Fifth, the question arises whether and how CBAM is effectively enforced and enforceable [

35,

115]. CBAM is a unilateral EU policy enforced by the respective Member State customs authorities, who, in specific instances, can report to the EU Commission [

113]. Also, CBAM is a Regulation and thus directly applicable (Article 288 TFEU) and with direct effect in the Member States (see no need for implementing measures in the Member States as a condition for direct effect in Van Gend & Loos, 1963, para. 17). Problems of enforcement in governance theory arise where “laws or political measures are not effectively implemented in practice” and depend on the norm addresses as well as the complexity of the law or policy measure [

34].

Enforcement (problems) can occur in relation to the regulated norm addressees; importers of iron and steel, aluminum and electricity from countries like China, India and Serbia, who need to effectively apply for the status of an authorized CBAM declarant (once), apply and pay for a sufficient amount of certificates (annually) and ensuring that enough certificates are on the importers account (quarterly) [

130]. It has been held that the CBAM, as of now, is overcomplex and would impose administrative and financial burdens on SME importers of the aluminum and steel sector,

i.e., during the reporting phase, which is why these will be excluded from the CBAM following its amendments [

155]. Moreover, an increased use of default values in hard to measure sectors like electricity will ease the administrative burden of accounting for emissions on the side of importers. Importantly, recent literature focused on countries with lower capacities, which will not be able to respond to the incentives set by the CBAM and instead risk falling behind in the global strive for emission reductions [

25,

30,

156].

Norm addressees might prevent the full effectiveness of the CBAM by opposing the unilaterally imposed CBAM, with claims of protectionism and inequality playing a key role [

149,

157,

158]. Based on the amount of exports into the EU and their relative importance to the EU relative to the amounts of exports from the EU to specific countries, Overland et al. predict the greatest resistance from countries like China, India and Russia [

159]. This is interesting since the research predicted that the burden shifted to different countries in terms of impact on GDP is positive for China, which might record slight net gains, while countries like Serbia lose to a much greater extent (GDP decrease of 1%) [

23] (p. 13). Means of opposition might include negotiations or WTO- based litigation under the Multi-Party Interim Arbitration Agreement for countries with lesser economic weight, while large economies may simply absorb the loss without substantial change and subsidize the national importers, which are subject to the CBAM tariffs [

55,

145,

159]. Moreover, in line with current political tensions between the US government and the democratic West, retaliatory trade measures are likely, especially in the steel sector (see on tariff wars [

36,

55,

149]). Following economic theory, such retaliation may arise wherever the share of exports targeted by the CBAM presents a negligible share of the countries’ total production (as will be the case for India’s steel production) [

113] (for further research on potential scenarios of trade retaliation [

160]). Moreover, countries in Eastern Europe and Africa might lack the infrastructure to respond to the administrative needs of reporting adequately, thus incurring economic consequences from not being able to prove their lower emissions [

23,

130,

149]. These countries might be impacted to relatively larger extents than countries like China or the US, which have larger investment capabilities to divert the increasing costs by means of carbon efficient and reducing technologies or implementations of carbon pricing systems [

23,

28,

55]. However, research also held that foreign capital investment would be attracted in such cases and lead to improvements in clean energy technology [

36].

As CBAM remains an additional cost, the importer might seek to avoid CBAM through circumvention practices, which pose a major enforcement problem [

161]. Within the meaning of CBAM, circumvention occurs where trade patterns are changed in order to partially or entirely avoid the CBAM obligations for which there are insufficient other economic reasons through, for instance, the slight modifications of goods or artificial splitting of consignments (Article 27, Recital 66 CBAM Regulation) [

137,

148,

162]. To encounter such avoidance, the EU Commission can adopt delegated acts to expand the scope of CBAM to include modified goods without the administration of penalties [

119]. Thereby, more downstream products might be included [

137,

163]. Moreover, replacing the current consignment-based regime with an annual cumulative mass-oriented

de minimis quantitative threshold will address competitive distortions between large-scale one-off and small-scale repeated importers while, thanks to its cumulative nature and continuous monitoring of these exempted importers as “occasional CBAM importers”, address circumvention practices and keep up origin-neutrality ([

27] (p. 429)) ([

137] (p. 4)). However, circumvention practices vary by sector. For instance, resource-shuffling in the electricity sector occurs when GHG emissions are shifted to other less regulated entities, thereby creating the false appearance of emission reductions for buyers of more regulated regions while net emissions of the product remain the same [

164,

165,

166]. This practice is projected to be adopted particularly by developing countries [

29]. In the aluminum sector, “the scrap hole” needs to be addressed, especially as main producers such as China are predicted to enter a “booming aluminum scrap age” ([

53] (p.10)) [

167]. Currently, ferrous scrap is excluded from the CBAM (Annex I, 72), while pre-consumer scrap should be differentiated from post-consumer scrap and is recommended for the production of aluminum to reduce emissions [

73]. Without differentiation, product shuffling is encouraged, whereby scrap content shares are raised to circumvent full payment under the CBAM [

168]. Despite the amendments, several cases of circumvention cannot be adequately captured by the CBAM. For instance, cases that go beyond slight modifications of goods where goods are fully transformed into others, for instance, steel into cars, to cases of imports under the inward processing procedure, where goods produced with foreign materials become cheaper than those produced with domestic materials subject to the ETS system or circumvention practices of product mixing or transshipment and dual production or sales practices (see for further explanation [

161].

In order to effectively implement CBAM, non-compliance needs to be effectively penalized and reduced [

161]. Custom authorities can punish norm addressees under the following three scenarios with administrative or financial penalties (Recital 80 CBAM Regulation). First, where importers or respective indirect customs representatives have not duly fulfilled the reporting obligation during the transition phase (see Article 35 (1–2) and (3–5) CBAM Regulation). Then, the customs authority is required to impose an “effective, proportionate and dissuasive penalty” corresponding to at least 10 Euro per t of unreported emissions (Article 35 (5) CBAM Regulation; Article 16, Recital 13 CBAM Implementing Regulation) [

161]. Second, where an authorized CBAM declarant failed to fulfill the certification obligation of CBAM in due time, the penalty consists of a payment of a fine corresponding to those for excess emissions under the ETS Directive, starting with 40 and increased to 100 Euro, which is due per lacking certificate (Article 26 (1), Recital 26 CBAM Regulation). Thirdly, where someone else other than the authorized declarant imported goods into the customs union, penalties increase to up to 5 times compared to the second scenario, taking into consideration the circumstances of the unauthorized import and setting the amount of the penalty high enough to be “effective, proportionate and dissuasive” (Article 26 (1)–(2), Recital 26 CBAM Regulation). All the while, the overdue certificates remain due (Article 26 (3) CBAM Regulation), and specific notification obligations have to be fulfilled by the respective national authority (Article 26 (4), Article 35 (5) CBAM Regulation). That means that all penalties other than the one for underreporting are based on minimal requirements set out by the CBAM Regulation and thus not uniform across MS, while, however, data collection on, for instance, the incorrect reporting during the transition phase is effectively centralized with the European Commission [

161]. Moreover, to impose effective penalties, a fine higher than the current ETS price seems adequate, which has reached a peak of 105.73 Euro in 2023, thus making avoidance of the CBAM cheaper than compliance. It has to be noted that the ETS price fluctuates and, as of the state of knowledge in March 2025, is 68.5 € lower than the potential fine with a projected rise in the future [

169]. If the ETS price rises beyond the available penalties, the question will be how high penalties will be to be “effective, proportionate and dissuasive”.

Major enforcement problems for the governing authorities may be caused by the number of addressees and the monitoring capabilities of the customs authorities. Currently, the CBAM addresses 200,000 instead of the planned 20,000 importers. To reduce this overly large group and facilitate monitoring and controlling activities of the respective national authorities, the European Commission introduced the mass-based

de minimis threshold [

44,

137]. In addition, data gathering, verification, and management pose challenges to the enforcement of import sustainability policies [

161]. Calculating the (actual or default value-based) embedded emissions of imports in an age of long and complex global supply chains requires substantial amounts of data and administrative capacities on the side of enforcing authorities, which are often not readily available [

113,

134]. Focusing on emission-intensive and energy-exposed goods where the potential for carbon leakage is largest is the first step while categorizing them into aggregates subject to the same carbon tariff has been suggested as an effective second step [

134]. Yet because this would undermine potential incentives for individual producers to reduce emissions [

134], CBAM cuts short on the second step by requiring payments for actual emissions while aggregating goods into categories (Annex I) and employing default values, for instance, in the case of electricity where tracing the emissions to a country of origin is difficult due to the interconnectedness of the energy markets (Recital 52 CBAM Regulation) [

22].

However, the extent to which accurate data can be obtained, based on truthful and precise registration in the registry, remains the Achilles heel of successful enforcement of the CBAM [

161]. Beyond an increased use of default values, the CBAM Amendment suggests ways to improve communication channels between national and European authorities and enhance the data processing abilities of the Commission.

3.1.6. Can CBAM Avoid Shifting Effects?

After having analyzed the design of CBAM and challenges with regard to typical sustainability governance problems of enforcement, ambition, and depicting, including already some remarks regarding shifting effects, the major question remains to what extent the CBAM will address spatial, sectoral, and resource-related shifting effects [

9] and rebound effects [

9] and how they might be offset by coalition building with equal power and feedback loops [

170,

171]. Shifting effects can occur on both the consumption and production side where “use of resources or emissions is shifted from the companies and citizens concerned to other areas of life or places or other resources are used more all the more intensively” [

9] (p.252).

The CBAM seeks to address the case of spatial emission shifting or carbon leakage where “for reasons of costs related to climate policies, businesses in certain industry sectors or subsectors transfer production to other countries or imports from those countries replace equivalent products that are less intensive in terms of greenhouse gas emissions” (European Union, 2023, Preamble, Rec. 9). Leakage can occur through four channels: indirectly through the energy or fossil fuel market [

16,

118,

131,

136,

145], directly through the competitiveness channel [

16,

131,

145] either operationally for instance through relocation, albeit technically and financially unfeasible [

136,

172], or through hard to detect investments [

172] and depending on regional variations in production emission intensity and international trade [

16,

96]—and rarely through technology spillovers [

16]. In addition, commodity price fluctuations and supply chain disturbances can be considered leakage, though it has to be noted that the complexity of the shifting phenomenon might extend beyond the listed elements [

156,

173]. If not addressed, leakage will offset the carbon emission reduction and competitiveness target of CBAM and obstruct compliance with the PA [

135].

The foregoing analysis provided an understanding of the CBAM elements that might lead to carbon leakage and those that might reduce this risk. Advantageous is the expansive scope of CBAM, especially as free allowances under the ETS are phased out [

55], which, together with possibilities of covering more downstream production, the inclusion of non-carbon GHG emissions, albeit incomplete, and the consideration of process emissions in addition to combustion emissions point to a reduced leakage risk under the CBAM. However, the CBAM omits important sources of GHG emissions by excluding indirect emissions for most of the goods covered in the initial phase, which creates incentives for carbon leakage and reduces incentives to adopt environmentally meaningful modes of production (

i.e., including a greener energy mix), (see also [

16,

47]). The mechanism charges imports based on a country and not production-based default value, especially as the production system boundaries were excluded as a means of calculating embedded emissions for complex goods, thereby increasing the risk for carbon leakage. Yet, this effect has to be weighed against the mitigative effect of measurement of emission intensities based on export countries instead of at the industry level([

23] citing the EC Impact Assessment). Further downsides of the CBAM are that focusing on imports, as might be the legally most viable solution, risks a substitution effect where exporting countries increase emission-intensive activities in the domestic market and decrease the activity level in the export market, which, theoretically, may be expected following increases in domestic for aluminum in India [

174]. While some suggest that the CBAM yields potential for positive spillover effects such as technology transfers through partnerships and resource sharing [

175], research showed that such technology spillovers from the EU to non-Eu countries under the CBAM are unlikely [

176], which, as demand increases globally, prevents other and developing countries from adopting climate-friendly and green technologies further widening the gap between different countries’ availabilities to realize carbon reductions [

177].

Precise measurement of carbon leakage is difficult due to persistent problems of depicting [

33]. Carbon leakage has been expressed in terms of change in foreign emissions compared to emissions reduced in the domestic unilaterally regulated area [

16,

96]. Based on computable general equilibrium models, which are most commonly used in carbon leakage research, it was confirmed that the aluminum and steel industries exhibit high leakage rates (between 20 and 70%) (in reference to the literature [

16]). Research investigating the effects of the CBAM on carbon leakage found that despite the limited carbon coverage, the CBAM might save annually 40 million tons of CO

2eq, effectively curbing carbon leakage in adopting countries and generally [

23] (for a review of the literature confirming this statement [

96,

178]). Research on leakage in the international trade of iron and steel confirms these findings, with large declines in CO

2 experienced by India (following Ukraine) [

19]. While setting an incentive for GHG emission reductions in steel production, the method most effective to that end, scrap recycling using the EAF method, also yields environmental benefits [

104]. To address leakage, the fossil fuel market should be targeted [

152], and since the CBAM does not include indirect emissions of most goods, it will not be able to capture structural changes shifting emissions at the electricity generation level [

17]. However, recent research summarizing previous studies held that the CBAM is very effective at reducing leakage through the competitiveness channel [

96]. Yet, production-based competitive leakage resulting from the aluminum scrap hole and resource reshuffling in general and the energy sector in specific remain a major source of carbon leakage [

133]. The ability to report actual emissions might yield an incentive to reduce actual emissions (D.2. CBAM Implementing Regulation) [

16].

Recent research summarizing reactions of the export countries included in this analysis implies that CBAM yields positive financial incentives pushing countries towards decarbonization; both India and China either consider expanding or implementing their own ETS like scheme while increasing investments in clean energies, and countries begin shifting their production into areas of clean energy, carbon capture storage, and hydrogen availability to minimize emissions (for confirming literature [

156,

158]). This, for instance, corresponds to the literature on economic theory suggesting that the Nash equilibrium in light of unilaterally imposed measures will, in different scenarios, not lie with retaliatory but rather adaptive measures like the one laid out above [

15]. While literature repeatedly held that under border adjustments, the burden shifted from regulated to unregulated countries [

17], the combined policy package of the CBAM and the ETS regulatory cap may discourage relocation of producers to regions with less stringent environmental regulation [

179]. Smaller trade partners like African countries otherwise negatively impacted by the CBAM might shift their exports to other markets [

149]. Overall, the EU is not projected to suffer economically. As the major trade partners of the EU adopt more green technologies and reduce differences in emission intensities [

180,

181], there are fewer incentives to relocate, and leakage through the competition channel is reduced [

16]. This suggests that the risks of direct carbon leakage through relocation to improve competitive advantages and by redirecting investments, as well as trade diversification and the aforementioned substitution effect, are smaller than expected and that the CBAM can effectively realize emission reductions and level the playing field [

156,

179].

To counteract shifting problems by additional means, the research suggests “equal powered coalition building” [

171] in [

115]. Indeed, the CBAM encourages action as part of a “Climate Club”, a coalition of the willing to promote the adoption of carbon pricing, including high-quality monitoring, reporting and verification, and transparency worldwide in a voluntary and inclusive way geared towards high-impact climate action to achieve the goals of the PA (Recital 72 CBAM Regulation). Some argue that opening up the possibility for exemptions of obligations under the CBAM to countries that are linked to the ETS system or where a comparable carbon price has effectively been paid amounts to a rather involuntary de facto Climate Club [

182]. However, as the CBAM recognizes command and control instruments in addition to regular market-based domestic instruments, adopting countries may face an additional source of revenues, which may be welcomed by developing countries, together with the potential of rerouting the European revenues to them (reviewing the literature [

118,

146] ) . Currently, Germany, the US, and Japan are exploring common border adjustments [

69]. When comparing different scenarios of such a multilateral Climate Club to unilateral action alone by the EU, even a G7-led Club including the EU and the G7 or a coalition between China, the US and the EU all committed to 33% emission reduction targets will not yield the required emission cuts necessary to meet the PA pathway for 2 or 1.5 degrees [

178]—of course, since countries such as Germany already exceeded their budget as shown in the introduction of this article. Furthermore, some researchers held that the CBAM might be more suitable as a temporary solution, as the increasing number of participants in carbon border mechanisms increases the border crossing frequencies and administrative toll of managing different taxation systems while the strategic value of the mechanism reclines([

96] reviewing studies).

3.2. Legal Compliance Analysis—Especially with Regard to WTO Law

At this point, some additional legal compliance analysis is required, with a special focus on WTO law. After the EU and its Member States signed the PA in 2016, the European Commission set out a strategy for achieving net zero emissions by 2050 in the form of the European Green Deel in 2019 and reaching the PA goals (Recital 1–3 CBAM Regulation) [

183]. The EU set itself the target to reduce net GHG by a minimum of 55% compared to 1999 in 2030 (Recital 4 CBAM regulation) [

35,

184]. This was codified and rendered binding for all Member States in the form of a Regulation called European Climate Law in 2021 (Recital 5 CBAM Regulation) [

185]. Thereafter, a legislative package called “Fit for 55” was proposed (Recital 10 CBAM regulation) and created the framework, including the CBAM, to achieve the PA goals. The ETS predates the package but is included therein in a reformed way. The 2003 adopted ETS addresses emission-intensive industries and was revised on multiple occasions. It is considered “paramount” and the point of departure of many countries’ ambitions towards net zero emissions ([

21] (p. 295)) [

186]. However, shifting effects remained a major problem under the ETS, despite the allocation of free allowances, and as seen in the introduction above, the reduction pathway is clearly insufficiently measured against the Paris target [

35,

120].

Further EU legislation included a reformed ETS 1 [

187], together with the ETS 2 [

12], the Social Climate Fund (SCF) [

188], and the CBAM which seeks to prevent carbon leakage to reduce emissions and support the PA goals, while incentivizing other third country operators to reduce emissions, complementing the ETS and reinstalling the competitiveness of European producers (Article 1 (1–2), Recital 7 CBAM Regulation) [

35,

184,

189]). The effectiveness of the ETS and the EU in fulfilling its obligations under the PA are thus dependent on massively raising the level of ambition of especially the ETS—and on the success of the CBAM [

120,

189].

The CBAM is subject to European and international legal requirements and, unless compliant with many of these, risks legal challenges, as initiated by Russia in May 2025 in front of the WTO [

190]. The legal basis of the CBAM is Article 192 (1) TFEU, which grants the EU competencies in the adoption of environmental legislation [

191]. Where such competencies are conferred to the EU, standards of subsidiarity and proportionality limit their exercise (Article 5 TEU) [

192]. Subsidiarity concerns seem easily satisfied in light of the transborder dimension of climate change and carbon leakage, in addition to the trade element of the law [

120,

193]. The question of proportionality, however, remains more contested, requiring that the content and form of the Union measure should not exceed what is required to achieve prevention of “the risk of carbon leakage” (Article 5 (4) TEU, Article 1 (1) CBAM Regulation) [

120,

192,

193]. Research on the proportionality of the CBAM is rare. Generally, for an EU measure to be proportional, it must be firstly suitable and secondly necessary to the achievement of the legitimate objective, while thirdly also proportional strictu sensu (not imposing an excessive burdens relative to the overarching goal) [

194,

195]. However, the EU legislation enjoys broad discretion in the interpretation of the proportionality principle in the regulation of environmental problems [

193]. Moreover, the European Court of Justice has accepted the legislators wide discretion in areas entailing “political, economic and social choices” (C-558/07, S.P.C.M. and Others; Case C-491/01, British American Tobacco, paras. 123 respectively) [

120,

196,

197]. Therefore, the pending action for annulment brought by Poland in 2023 on grounds of a wrong legal basis of the CBAM (

i.e., its contents that the CBAM is a fiscal rather than environmental in nature) will probably not be successful [

198].

WTO law poses more important legal challenges to CBAM. Primary general international rules are those other than the specific WTO rules and create international obligations that do contain a State obligation to maintain an equal playing field or competitiveness [

123]. While it is relevant to investigate the effect of the CBAM on bilateral trade agreements between the EU and any country, these often make reference to WTO law, specifically provisions of the General Agreement on Tariffs and Trade 1994 (GATT) [

199]. For instance, Serbia, India and China are, with some specific conditions applying to China, members of the WTO and subject to the GATT [

200]. Thus, the question turns to the compliance with and interpretation of the CBAM in light of the GATT. While the GATT was concluded before the foundation of the WTO, it is now one of its key pillars [

201]. The GATT pursues the purpose of fostering prosperity through international trade by reducing trade barriers and by ensuring equal and fairness-based treatment of all WTO/ GATT parties with special consideration of developing countries [

202,

203]. Global free trade by reducing tariffs and non-tariff barriers is thus only a means to several ends, including “raising standards of living, ensuring full employment and a large and steadily growing volume of real income and effective demand, and expanding the production of and trade in goods and services” (WTO Agreement, Preamble) [

31,

201].

Trade restrictions under the WTO are thus allowed for environmental purposes as long as they are not overly (“excessively”) restrictive [

144] (p.150). Taking into account that an ecological race to the bottom between nation states would be harmful even from an economic point of view, the GATT presents an inherent compromise between free trade and unilateral national (non-discriminatory) regulations as long as there are no comprehensive global environmental standards [

189]. The two most foundational principles of the GATT are the principle of non-discrimination, which finds expression in the Most Favored Nation (MFN) principle (in Article I) and the National Treatment Principle (NT) (in Article III) [

203]. These were raised by Russia as its legal basis. Russia’s challenge also considers several other Articles such as Articles II: 1 (a) and (b), X: 3 (a) and XI: 1 of the GATT and Articles 1.2, 1.3, and 3.2 of the Agreement on Import Licensing Procedures as legal bases for claiming that the CBAM constitutes a trade barrier disguised as “measures disguised to combat climate change” in contravention of international trade law [

190] (p.2). Moreover, Russia challenges the legal basis of the ETS, which we will not analyze in greater detail as the present research centers around the legality of the CBAM. We will analyze the legal challenges, focusing on the aforementioned MNF and NT principles in order to cover the most potent legal arguments against the CBAM as reflected in the literature. We will also assess which potential justifications can be raised by considering Article XX, notably XX:g, but also XX:a and XX:b GATT.

The first legal question is whether the CBAM creates a situation that amounts to a violation of the MFN principle. Article I GATT stipulates that “customs duties or charges of any kind imposed on [..] importation, […] any advantages, favor or privilege […] granted by any contracting party to any product originating in or destined for any other country shall be accorded immediately to like products originating in […] territories of all other contracting parties” (Article I,1 GATT [

199]). That means that all trade benefits must be granted equally to all other trade partners in an immediate and unconditional fashion [

122,

202,

203] (Belgian Family Allowances, para. 3 [

204]). If the products in question are like and discriminated against based on their origin, the CBAM would need to be justified under Article XX GATT [

146,

189,

205]. However, formal differential treatment does not constitute less favorable treatment and has to meet minimal provisions (Korea—Various Measures on Beef, paras. 137-8 [

206]). Exceptions to this rule are free trade and tariff unions such as the EU (Article XXIV, GATT) [

202]. Importantly, the assessments of likeness and the NT principle occur on a case-by-case basis, and thus a final assessment remains with the Courts (Philippines—Taxes on Distilled Spirits, paras. 115, 117 [

207]). Likeness is determined based on the Report of the Working Party on Border Tax adjustments (para. 18) [

208] and subsequent case law (such as Japan—Alcoholic Beverages, p. 20 [

209]), which sets out four criteria: a product’s end uses, consumer habits, the property, nature and quality of the product as well as the classification of the two goods in the tariff regime and the competitive relation of the goods of comparison [

189,

205]. The latter criterion was added by case law and can be determined with reference to the cross-price elasticity [

189] or substitution of the good [

203]. It is noted elsewhere that likeness depends on the legal context and thus may require a different analysis under Article I:1 than Article III:2 (Japan—Alcoholic Beverages [

209]) [

203]. However, case law held that these two are comparable (Indonesia—Automobile Industry, para 14.141 [

210]).

As of now, it is highly unlikely that the carbon content of a good would suffice to differentiate between two goods [

146](summarizing literature [

211]). Following WTO case law, such as US—Tuna I (para.5.14 [

212]), the notion of differentiating products based on such non-product related production and process methods (NPR PPM) was rejected [

31,