1. Introduction

Green finance is the process of making financing and investment decisions while taking the environment into account and encouraging ecological sustainability. It includes a range of financial products, technologies, and tactics designed to promote and aid in a sustainable economy. The private and public sectors are not distinguished in this scenario. Green finance includes funding that considers environmental preservation and seeks to support long-term economic objectives. Fiscal policies, central banking, carbon market instruments, green bonds, green banks, and financial technology that promote energy efficiency, renewable energy, and other environmental activities are a few examples of green finance projects (Sachs et al., 2019) [

1].

Green finance has gained prominence recently due to the agreement on environmental protection, climate change initiatives, and the 2030 Sustainable Development Goals (SDGs) [

2]. Green finance is sometimes referred to as “sustainable finance”, “environmental finance”, “climate finance”, or “green investment”. In order to achieve the SDGs, green finance aims to boost the amount of money flowing from financial institutions to economic actors engaged in environmental preservation initiatives and activities [

3]. The relevance of green finance peaked in 2016 at the eleventh G-20 summit in Hangzhou, China, when it was extensively discussed [

4]. The G20 research group defines green finance as “the financing of initiatives that generate environmental advantages within the framework of ecologically sustainable development” [

5]. In addition to their related advantages, these environmental benefits include decreased pollution of the air, water, and land; decreased greenhouse gas (GHG) emissions; enhanced energy efficiency while optimizing the use of available natural resources; and mitigation and adaptation to climate change. It is a first step in addressing numerous environmental issues and uniting economies on a sustainable course [

6]. Diversities in understandings and interest in green finance result from different conceptions of the idea that reflect the aspects of the topic that are important to the researcher.

Due to established protocols that firms must comply with, developed nations can better manage the environmental repercussions of economic development. While it is true that the world’s environmental catastrophe is caused by the enormous energy and material consumption in wealthy nations, it is also sustained by lax laws in emerging nations. International trade creates connections with emerging nations, which exacerbates environmental issues globally. Due to noncompliance with business regulations, which generally include (a) the disposal of industrial waste; (b) the use of antiquated machinery; (c) inadequate maintenance of plants and equipment; and (d) a lack of accountability from governing bodies, the severity of environmental issues is significantly higher in developing nations [

7].

While promising for sustainability, the circular economy presents distinct challenges for green finance. Compared to linear business models, circular approaches involve complex resource flows and longer investment cycles, making it difficult to model financial returns or establish standardized performance metrics. Measures such as pay-per-use and product-as-a-service often complicate collateralization and risk assessment, leading to hesitancy among traditional financiers. In the Indian context, the lack of quantifiable long-term benchmarks for resource recirculation further deters mainstream adoption, reflecting a broader challenge observed in developing regions of Africa and Southeast Asia [

8]. The goal of the circular economy and the concept of a green economy are very similar from an economic and environmental standpoint. The transition to a green economy involves the economical and efficient use of energy, natural resources, and new technologies, which leads to economic growth and the generation of jobs. If international commitment and a well-thought-out structure for international investment incorporate both rich and developing countries, implementing a green economic model could be successful [

9].

With an emphasis on sectors like renewable energy, energy efficiency, and climate-resilient agriculture, green finance initiatives aim to advance laws and corporate practices that are environmentally friendly. Nonetheless, there remain obstacles to the expansion of green financing, such as the requirement for clear definitions to avoid greenwashing [

10]. Notwithstanding these challenges, green finance is regarded as an essential step in the direction of sustainable development, providing a balance between environmental preservation and economic growth. Accessible information is becoming more and more necessary as the discipline develops to assist a broader audience in comprehending and navigating this area [

11].

Significantly, green finance intersects deeply with social goals such as gender equity, financial inclusion, and bridging regional disparities. Initiatives for expanding green finance in India must consider that women and marginalized communities often lack equitable access to formal financial services, limiting their participation in climate mitigation and sustainable development efforts. Several studies underscore that progress in green finance is uneven across Indian states, reflecting disparities in digital infrastructure, financial literacy, and gender norms [

12]. Promoting gender-responsive green finance and regionally inclusive policies can increase resource flows, enhance local empowerment, and magnify the social impact of sustainability investments [

13]. Addressing these social dimensions within green finance strategies is therefore essential to further SDGs and ensure that benefits reach traditionally underserved populations.

2. Literature Review

Numerous researches have been conducted regarding the uptake and persistence of green financing.

The researchers [

14] conducted the study and identified two key challenges in green financing: ethical investment challenges and lack of expertise and training. These obstacles present significant hurdles that must be addressed to facilitate the widespread adoption and effective implementation of sustainable financing practices.

The researchers [

15] identified several challenges in green financing within the context of Bangladesh. These challenges include an inability to identify the financial implications of reducing environmental risks, inadequate entrepreneurial interest in green projects, and a lack of skills to internalize environmental externalities.

The researchers [

16] conducted a study in the Malaysian context that revealed two significant barriers hindering the progress of green projects: insufficient capital commitment from sponsors and a dearth of comprehensive databases dedicated to these environmentally-conscious initiatives.

Uncertainty surrounding governmental policies, low financial institution involvement in the biomass sector, the short-term focus of available financial instruments, and a lack of technical know-how and awareness of financing options within businesses are some challenges facing the green finance sector. The expansion and uptake of sustainable financial techniques are severely hampered by these issues [

17].

In addition to regulatory and cost barriers, the operationalization of green finance in emerging markets relies on a variety of financial mechanisms. Carbon markets enable the trading of emission allowances, thereby creating economic incentives for emissions reduction. ESG-based investing channels capital toward projects with high environmental, social, and governance performance, while blended finance attracts private investment by de-risking projects through public or philanthropic capital [

18].

Furthermore, risk mitigation instruments, such as guarantees or insurance products, address the volatility and uncertainty inherent in green investments, especially in evolving markets. However, their adoption in India has been limited, paralleling similar implementation challenges in other developing economies [

19].

The author’s [

20] trend analysis revealed that the primary challenges associated with green financing in China were excessively short loan periods from banks, insufficient capacity within financial institutions, a lack of a comprehensive taxonomy for green finance, and inadequate policy signals to guide and incentivize sustainable investments.

Inadequate public awareness of green finance, disparate definitions and criteria across frameworks, disjointed policy coordination for green finance initiatives, conflicting regulations, and a lack of lucrative incentives for investors and financial institutions interested in climate change mitigation efforts are some of the challenges facing the shift to green finance [

21].

The researcher [

22] noted a number of current obstacles in the field of green finance. These issues include the dearth of thorough data, the difficulty of measuring and tracking the effects of green finance schemes, the lack of uniformity in rating criteria and reporting formats for these schemes, and the difficulties of valuing biodiversity and natural capital. Several issues must be resolved for green financing efforts to be implemented and evaluated effectively.

The researchers [

23] utilized bibliometric analysis to study the challenges associated with green financing. The research revealed that the high costs involved and the lack of comprehensive data for tracking environmental impact posed significant obstacles within this domain.

The researchers, using quantitative analysis techniques, found a number of significant obstacles to the successful execution of green finance programs. They notably emphasized the presence of technological obstacles that make it difficult to accurately quantify and report the sustainability benefits of different initiatives and projects. A major barrier to precisely measuring the environmental impact and determining the actual scope of sustainability initiatives is the absence of reliable technology solutions. The researchers also discovered the widespread problem of “greenwashing”, in which businesses use dishonest marketing and communication strategies to project an appearance of environmental responsibility without taking meaningful steps or producing noticeable outcomes [

24].

The researchers [

25], in their recent study employing Bibliometric Analysis, identified a significant challenge within the realm of green finance: the lack of standardization in green finance regulations. The absence of standardized regulations can lead to inconsistencies and ambiguities, hindering the effective implementation and adoption of green finance practices across various jurisdictions.

The primary research publications that served as the foundation for this study’s efforts to create a preliminary list of challenges in green financing are highlighted in .

.

Literature Review.

| S. No. |

Challenges as Per Themes |

Authors |

Year |

Methodology |

| A. Regulatory and Policy Barriers |

| 1 |

Lack of Policy Signals |

Jung Wan Lee |

2020 |

Trend Analysis |

| 2 |

Lack of Taxonomy of Green Finance |

Jung Wan Lee |

2020 |

Trend Analysis |

| 3 |

Lack of Standardization in Green Finance Regulations |

Krastev B. & Krasteva-Hristova R. |

2024 |

Bibliometric Analysis |

| B. Technological and Data Challenges |

| 4 |

Lack of Databases in Green Projects |

Amran A. et al. |

2018 |

Qualitative Analysis |

| 5 |

High Costs and Inadequate Data for Environmental Impact Tracking |

Mohanty S. et al. |

2023 |

Bibliometric Analysis |

| 6 |

Technological Barriers for Measuring and Reporting Sustainability Impacts |

Ayaz G. & Zahid M. |

2024 |

Quantitative Analysis |

| C. Market and Financial System Constraints |

| 7 |

Lack of Capital Commitment from Sponsor |

Amran A. et al. |

2018 |

Qualitative Analysis |

| 8 |

Too Short Terms of Loan Periods from Banks |

Jung Wan Lee |

2020 |

Trend Analysis |

| 9 |

Lack of Capacity of Financial Institutions |

Jung Wan Lee |

2020 |

Trend Analysis |

| D. Institutional Capacity and Awareness Gaps |

| 10 |

Ethical Investment Challenges |

Islam M. et al. |

2014 |

Qualitative Descriptive Analysis |

| 11 |

Lack of Expertise and Training |

Islam M. et al. |

2014 |

Qualitative Descriptive Analysis |

| 12 |

Inability to Identify Financial Implications to Reduce Environmental Risks |

Rashid M. & Uddin M. |

2018 |

Systematic Review and Descriptive Statistics |

| 13 |

Inadequate Entrepreneurial Interest in Green Projects |

Rashid M. & Uddin M. |

2018 |

Systematic Review and Descriptive Statistics |

| 14 |

Lack of Skills to Internalize Environmental Externalities |

Rashid M. & Uddin M. |

2018 |

Systematic Review and Descriptive Statistics |

| E. Governance and Transparency Issues |

| 15 |

Greenwashing and Lack of Transparency in Projects |

Ayaz G. & Zahid M. |

2024 |

Quantitative Analysis |

The reviewed literature on green finance barriers has evolved notably over the last decade. Earlier studies (2014–2018) primarily emphasized institutional weaknesses, including ethical investment challenges, lack of expertise, and entrepreneurial apathy. These concerns reflect a formative stage in green finance, where awareness and capacity-building were critical gaps. From 2020 onward, the focus shifted toward systemic and structural issues such as regulatory fragmentation, lack of taxonomy, and short loan durations. These studies (e.g., [

20,

25]) reflect a growing demand for consistency and clarity in green finance policies. In recent years (2023–2024), attention has expanded to technological and data challenges [

23,

24] and transparency concerns like greenwashing, highlighting the increasing complexity of measuring and validating environmental performance.

The current study aligns with and extends this progression by offering a systematic structural interpretation of these barriers. It emphasizes the cascading influence of regulatory deficiencies, which indirectly affect data reliability, investor awareness, and cost structures—a layered dynamic not explicitly addressed in previous studies. Unlike much of the literature that examines barriers in silos, this paper integrates these dimensions through a hierarchical ISM model, revealing how root causes like weak regulations generate downstream consequences, including greenwashing and high verification costs. This approach offers a more interconnected understanding and identifies priority intervention points for policy reform.

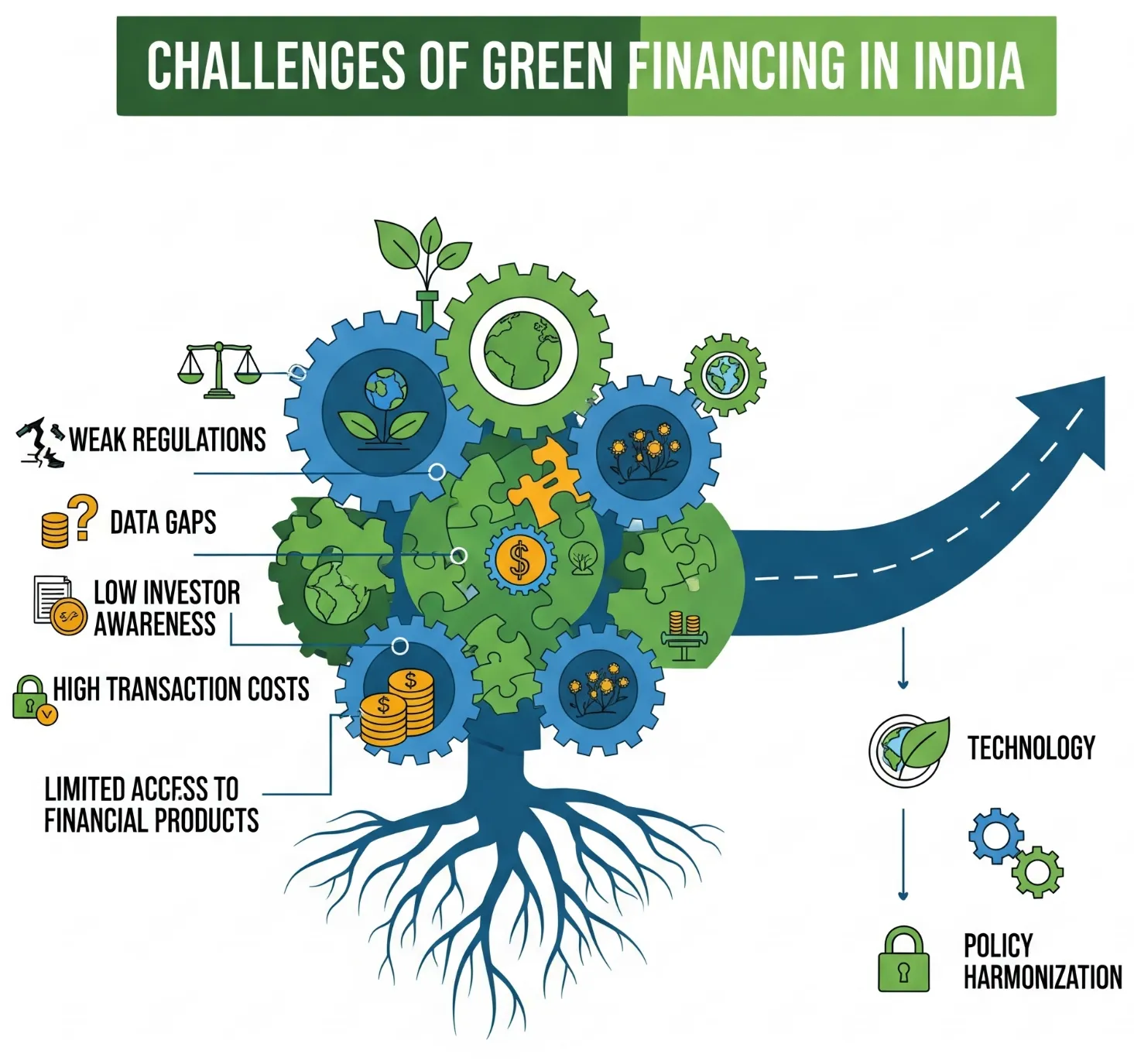

3. Problem Description

A confluence of structural, regulatory, and market-specific issues intrinsically complicates green financing in India. One major obstacle hindering the comprehension and uptake of green funding mechanisms is stakeholders’ lack of knowledge and experience. This unfamiliarity with sustainable finance solutions frequently results from a lack of access to effective case studies that highlight the observable advantages of such projects, as well as insufficient educational and training opportunities. As a result, decision-makers and possible beneficiaries might find it difficult to understand the subtleties and complexity involved, making it more difficult for them to negotiate the complex world of green funding successfully. To accelerate the adoption of these essential financial instruments and ultimately advance the transition to a more resilient and sustainable future, it is imperative that this knowledge gap be filled through extensive capacity-building programs, the sharing of best practices, and the promotion of cross-sector collaboration.

Furthermore, green initiatives sometimes have large upfront costs, which makes it challenging for developers and small and medium-sized businesses (SMEs) to finance such expenditures. Regulatory gaps, such as uneven rules, inadequate incentives, and the lack of standardized frameworks further hamper the flow of green financing. Financial institutions view green ventures as high-risk because of technological uncertainty, lengthier payback periods, and a lack of data on project viability. Furthermore, there aren’t many investors in products like green bonds because the Indian green finance business is still in its infancy. These problems are worsened by India’s difficulty in striking a balance between environmental objectives and urgent socio-economic demands like job development and poverty reduction. Thus, the issue of green financing in India is extremely complex and multidimensional due to these interconnected elements. A complex environment has been generated by the nation’s rapidly expanding economy and population and the urgent need for sustainable development. To solve environmental issues and foster economic growth at the same time, financial resources must be wisely deployed.

By integrating techniques such as Interpretive Structural Modeling (ISM) to comprehend hierarchical linkages among numerous aspects, the systems approach to problem-solving in green finance in India can successfully address its complexity. According to this method, green finance is a system comprising interrelated elements, including investors, financial institutions, end users like SMEs, technology providers, and regulatory frameworks. ISM offers a clear hierarchy and is especially helpful in identifying and organizing various elements according to their effect and dependency [

26]. ISM can classify features like policy frameworks as foundational drivers. This hierarchy aids decision-makers in determining which elements require urgent attention to have a systemic impact. Stronger regulations or fundamental incentives, for instance, can lower perceived risks and promote increased involvement from financial institutions and investors. To forecast the results of interventions, prioritize actions, and match green funding projects with India’s socio-economic and environmental objectives, the systems approach methodology known as ISM can significantly expedite the decision-making process. Decision-makers can use this potent analytical tool to break down complex systems into their component parts and create hierarchical linkages between them. This methodical approach encourages strategic, well-informed decision-making for successful, sustainable finance scaling. Consequently, decision-makers can prioritize actions based on their relative importance and potential impact, optimizing resource allocation and ensuring strategic alignment with national objectives.

4. Materials and Methods

4.1. Nominal Group Technique (NGT)

The NGT stimulates participation from all panel members and neutralizes/diffuses the negative impacts of group dynamics by preventing group participants from dominating the discussion session [

27]. Small-group structured discussions, or NGTs, are used to get participants to agree on research priorities. According to research, NGT is significantly better than other interactive group exercises, such as brainstorming to produce ideas or problem-solving techniques [

28]. The optimal composition of a NGT’s group comprises four to seven participants, with a permissible range of two to twenty individuals per group [

29]. If necessary, the group will participate in a collaborative dialogue if more discussion or clarification is necessary. This procedure could entail looking for more details, asking insightful questions, or asking for clarification on particular issues. To streamline the conversation and promote a more concentrated and effective exchange of ideas, the group will also take on the duty of combining any overlapping or identical points of view [

30]. By adopting this strategy, the organization hopes to foster an atmosphere that encourages idea sharing, the investigation of many viewpoints, and the creation of a body of collective knowledge. Participants then rank, vote, or rate the points on the list in order of priority [

31]. The facilitator then determines the overall group priorities by condensing the final mean scores. As a result, these NGT technique stages are helpful for generating a wide range of opinions and concepts in an organized and methodical manner. As a result, NGT simplifies decision-making tasks and incorporates formal brainstorming [

32].

Application of NGT in this research work: For this research study, the key stakeholders in the relevant field were initially identified based on the researchers’ judgment. Once these major players had been determined, formal invitations to participate in the project were extended. Experts who responded with interest and acceptance to the researchers’ outreach were then engaged to directly contribute to and inform the work. The domain experts were shown the factors influencing green financing (from the literature review) in the first session of NGT. Finalizing the list of elements to be used in the structural analysis was the aim of the first NGT session. The creation of a matrix outlining the pairwise contextual relationships between the elements and the checks/adjustments for conceptual inconsistencies in the final model were the focus of the second and third sessions, respectively. Every session started with a triggering question and a purpose. Each session allowed for an anonymous, individual ranking of issues before group discussion. This minimized the impact of dominant personalities and encouraged independence of thought. After initial aggregation and presentation of group judgments, points of disagreement were collectively discussed, allowing experts to adjust their views in light of alternatives. The discussion continued until a consensus was attained, ensuring a comprehensive understanding and alignment on the matter. Pre-defined rules dictated the inclusion of relationships in ISM matrices. For example, relationships were accepted if ≥70% of experts agreed; borderline cases were flagged for focused re-examination or secondary voting. This deliberate approach created a culture of active participation where a range of viewpoints were accepted and combined to reach a consensus that embodied the group’s collective knowledge. highlights the profiles of 10 domain experts engaged in the study. describes the purpose, triggering question, and output of three NGT sessions.

.

Profiles of the domain experts participated in NGT sessions.

| Profile |

Number of Experts |

| Investment fund Managers/Individuals |

3 |

| Banking professionals |

2 |

| Academicians and Researchers |

2 |

| Green Technology innovator |

1 |

| Corporate governance expert |

1 |

| Start-up founder |

1 |

| Total |

10 |

.

Details of NGT sessions conducted.

| NGT Sessions |

Purpose |

Triggering Question(s) |

Outcome |

| Session 1 |

To finalize the list of elements based on the list derived from the literature review to be taken forward for analysis |

After referring to the list of factors, which factors do you think affect the adoption of green finance and should be considered relevant for analysis? |

Out of a list of 15 factors, experts finalized 9 elements. |

| Session 2 |

To define the pairwise relationship among the finalized elements |

Based on the rationale, clarify how each element is related to the other based on the ability to influence. |

The consensus-based judgments on 36 pairwise selections of elements were used to develop the SSI matrix. |

| Session 3 |

To make checks for any conceptual inconsistency in the generated ISM result. |

Do any of the links in the model have any conceptual inconsistencies? |

Experts concluded that there were no conceptual inconsistencies. |

4.2. Interpretive Structural Modelling (ISM)

The ISM technique was introduced by Warfield [

33] to construct a structural hierarchy among elements for a particular contextual relationship. Since ISM for the components focuses on contextual interactions to describe complex systems, it is a step forward in systems analysis. According to the researchers [

34], a systems research project necessitates the identification of appropriate elements or factors as well as the interactions—that is, the contextual relationships among those specified elements within the system in question. ISM has been seen as one of the techniques for systems modeling, which is a subset of Interactive Management (IM) [

35], in general. The ISM process transforms complex mental models that are poorly expressed and ambiguous into more straightforward models that are well-defined, observable, and rationally expressed [

36]. The purpose of ISM is to facilitate decision making by the policy makers, stakeholders, and decision makers in general. ISM gives decision-makers a comprehensive picture of complicated situations by methodically integrating several data sources and accounting for a variety of elements and their interdependencies [

37]. This method makes it easier to make well-informed, rational decisions supported by data and in line with the objectives and priorities of the company. The clear mental models with hierarchical linkages help to determine the nature of influence of crucial drivers upon the dependent ones [

38]. Therefore, the reduction of complexity is the primary motive behind the systems approach to problem solving. Over time, systems researchers seeking a flexible approach to handle social science problems began to focus heavily on the ISM.

Application of NGT in this research work: The ISM and MICMAC have been used in this study. The process of developing ISM-MICMAC starts with defining pairwise contextual relationships among the identified elements of green finance. To improve reproducibility and traceability, all pairwise contextual relationships were analyzed using SmartISM 2.0 software [

39], which follows a rule-based approach to generate Self-Interaction and Reachability Matrices. This technological integration minimized user-based inconsistencies and supports the repeatability of findings by future researchers. These measures significantly reduce individual bias and enhance the robustness of derived hierarchies.

5. Results

5.1. Identification of Elements

The outcome of first NGT session came out to as the finalized list of elements ().

.

List of final elements.

| S. No. |

Element Name |

Description |

| 1 |

Lack of Standardization in regulations |

Inconsistent regulations and fragmented policies hinder global adoption of green finance. |

| 2 |

Greenwashing |

The prevalence of misleading claims about sustainability undermines trust and complicates product assessment. |

| 3 |

Limited Investor Awareness |

Many investors are unaware of green finance opportunities and their benefits. |

| 4 |

Regulatory Deficiencies in Developing Countries |

Insufficient frameworks in emerging markets restrict green financing growth. |

| 5 |

High Costs |

Initial Investment Costs, Cost of Compliance, risk premium, transaction costs, etc. |

| 6 |

Access to Financial Products |

Limited availability of green financial products in emerging markets constrains investment options. |

| 7 |

Data Gaps and Technological Barriers |

Lack of reliable data and challenges in measuring and reporting sustainability impacts hinder effective decision-making. |

| 8 |

Measuring Environmental Returns |

Quantifying the environmental benefits associated with financial returns remains a complex issue. |

| 9 |

Circular Economy Integration |

Difficulty incorporating circular economy principles into financial strategies poses additional challenges. |

5.2. Contextual Relationship among Elements

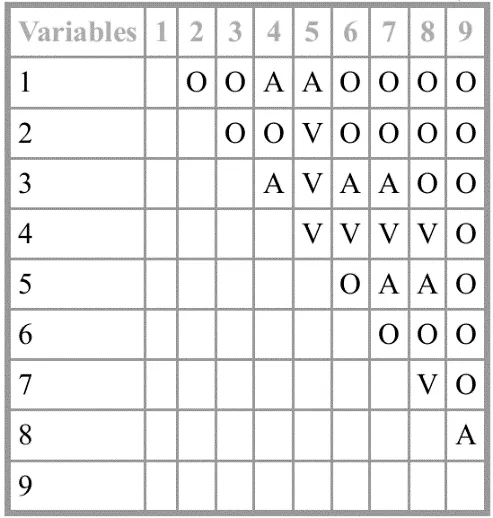

5.2.1. Structural Self-Interaction Matrix

The relationships based on the nature of influence are defined based on pairwise selection. V indicates ‘i’

th row element influences column element ‘j’; A indicates ‘j’

th influences ‘i’; X indicates both row element ‘i’ and column element ‘j’ influence each other; O indicates parameters ‘i’ and ‘j’ have no influence or these are not related. The experts discuss and decide on each pairwise selection of elements. Only the upper diagonal part of the matrix is taken for this task. Refer .

. Structural Self Interaction Matrix (Source: SmartISM 2.0 software).

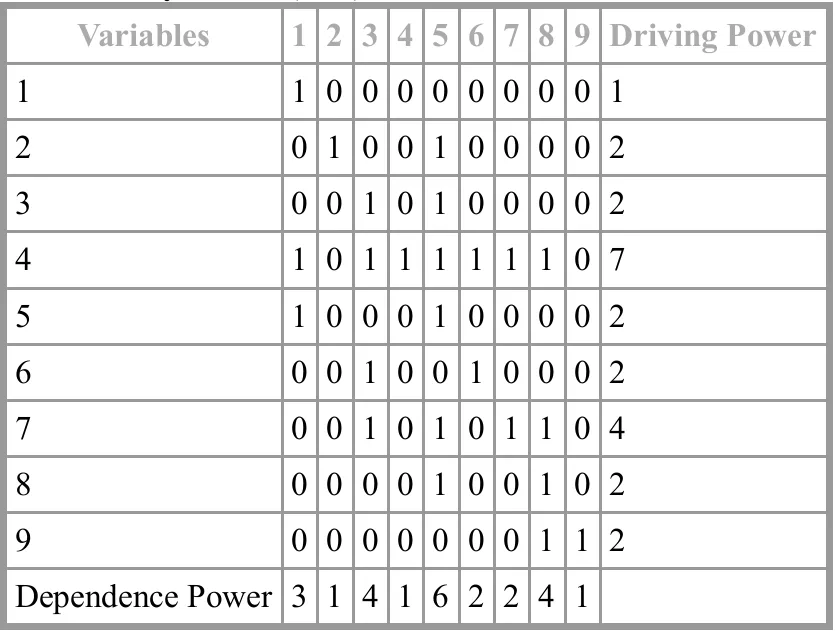

5.2.2. Initial Reachability Matrix

Rules of transforming to initial reachability matrix () are as follows:

-

-

If (i, j) entry in SSIM is V, then (i, j) entry in the reachability matrix becomes 1, and (j, i) entry becomes 0.

-

-

If (i, j) entry in SSIM is A, then (i, j) entry in the reachability matrix becomes 0, and (j, i) entry becomes 1.

-

-

If (i, j) entry in SSIM is X, then (i, j) entry in the reachability matrix becomes 1, and (j, i) entry also becomes 1.

-

-

If (i, j) entry in SSIM is O, then (i, j) entry in the reachability matrix becomes 0, and (j, i) entry also becomes 0.

. Initial Reachability Matrix (Source: SmartISM 2.0 software).

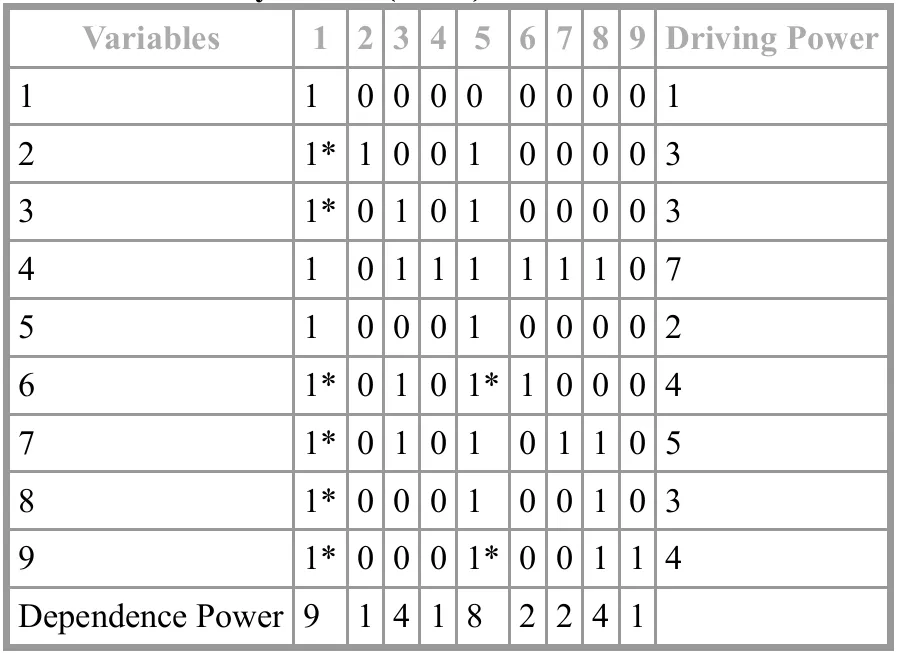

5.2.3. Final Reachability Matrix

The initial reachability is transformed to a final reachability matrix (

) following the transitivity checks. Transitivity check means that if experts have defined that Element ‘A’ influences ‘B’ and Element ‘B’ influences ‘C’ but did not consider that Element ‘A’ will also influence ‘C’. This kind of associations are traced at Final reachability matrix stage and all such 0s are converted to 1

∗ (to highlight the converted ones).

. Final Reachability Matrix (Source: SmartISM 2.0 software).

5.2.4. Deriving Final ISM

To attain final ISM, some crucial transitive links may be retained, but preferably to have a clear model with less complexity, unrequired transitivity are removed. The required links in the model are kept as 1 in the reduced conical matrix (

). This matrix also classifies the levels allotted to each element in the hierarchy. The conical matrix is formed by setting the elements as per their position in the hierarchy from top to bottom.

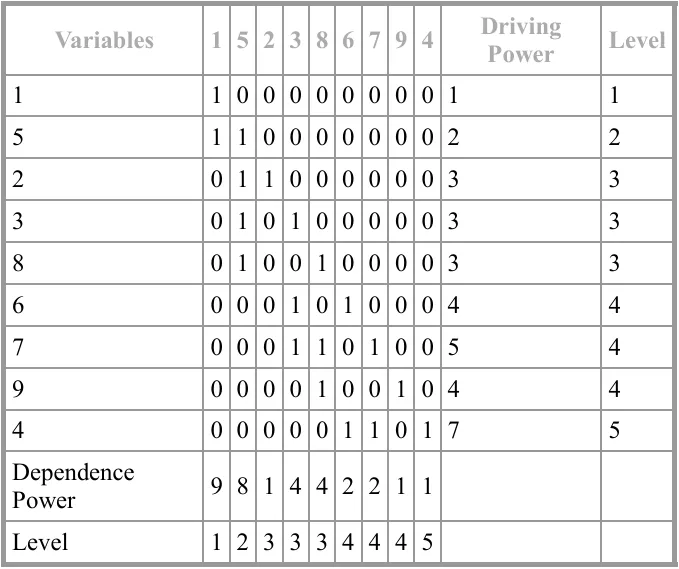

. Reduced conical matrix (Source: SmartISM 2.0 software).

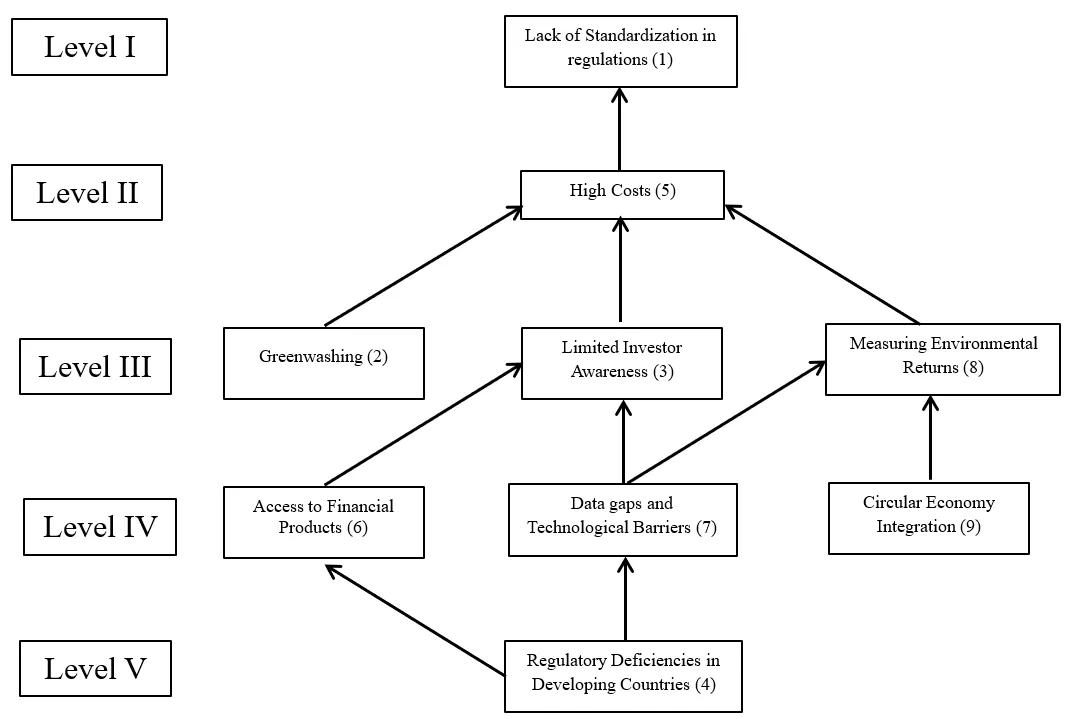

The final ISM can be seen as

.

. Interpretive Structural Model (Source: SmartISM 2.0 software).

The hierarchical relationships identified in the ISM model can be better understood through institutional theory, which explains how institutional environments—including norms, regulations, and governance structures—shape organizational behavior and market evolution. Regulatory deficiencies, placed at the foundational level of the model, reflect institutional voids that hinder the standardization and enforcement necessary for effective green finance deployment. These voids create uncertainty, reduce trust, and disincentivize private sector participation, ultimately cascading into challenges like inadequate data, high transaction costs, and limited investor awareness. Additionally, stakeholder theory provides insight into how various actors—governments, investors, civil society, and financial institutions—interact and prioritize interests within green finance ecosystems [

40]. The presence of greenwashing, positioned as a mid-tier amplifier, reflects asymmetries in transparency and accountability between stakeholders, reinforcing the need for cohesive policy frameworks and stakeholder alignment.

Moreover, green finance is intrinsically tied to the objectives of climate finance and the United Nations Sustainable Development Goals (SDGs), particularly SDG 13 (Climate Action), SDG 7 (Affordable and Clean Energy), and SDG 9 (Industry, Innovation, and Infrastructure). The theoretical connection emphasizes that green finance is not only a financial mechanism but a policy and institutional conduit for long-term sustainability transitions. By framing the ISM findings within these broader frameworks, the study provides a more persuasive, generalizable narrative on how structural enablers—or the lack thereof—determine the success of climate-aligned financial flows in emerging economies like India.

6. Discussion

While India faces distinct regulatory, market, and data-related barriers in scaling green finance, comparable challenges have been reported across emerging markets. For instance, Southeast Asian economies such as Indonesia, Malaysia, and Vietnam also grapple with financing gaps, fragmented regulatory frameworks, and the need for cohesive climate-related disclosures [

41].

Efforts to promote green bonds or integrate sustainable development objectives are often constrained by limited institutional capacity and a lack of standardized taxonomies, much like in India [

42]. Integrating such cross-country perspectives underlines that many obstacles are not unique but broadly shared among developing economies, strengthening the external validity and wider relevance of this study’s conclusions.

To validate and contextualize the hierarchical relationships identified through ISM, this study draws on empirical evidence from India’s green finance market:

-

-

India saw an estimated USD 10.2 billion in green bond issuances in 2023, primarily targeting renewable energy and infrastructure, as per Climate Bonds Initiative and RBI disclosures [22].

-

-

Case studies from IFC indicate that green-certified buildings in Tier-2 Indian cities achieved 20–30% energy savings post-implementation, supporting the importance of measurable environmental outcomes [23].

-

-

Regulatory reforms such as SEBI’s Business Responsibility and Sustainability Reporting (BRSR) mandate have promoted ESG transparency and partially addressed greenwashing and disclosure gaps [24].

These data corroborate the ISM findings that regulatory standardization, environmental tracking, and investment transparency are essential prerequisites for sustainable green finance adoption in India.

6.1. Results

The 9 finalized elements were divided into 5 levels, starting Level I at the top. The interpretation of the model starts from the bottom most level, comprising the strong driver. The top most level contains the most dependent element. The direction of the arrows defines the contextual relationship of influence. The following points of interpretation can be drawn with respect to the model output.

-

-

Regulatory deficiencies in developing countries (Element 4) at level V influence access to financial products (Element 6) at level IV. The investors in green projects face uncertainty and risk due to regulatory shortcomings in developing nations, such as lax environmental regulations and a lack of standardization. This may reduce the appeal and accessibility of green financial solutions. Inadequate regulations and control may foster an atmosphere that encourages fraud, exploitation, and malpractice. Financial institutions may find it challenging to uphold norms for accountability, transparency, and consumer protection when operating in such environments. They are hesitant to issue specialized products like green bonds or loans in the absence of clear legislation or incentives. Furthermore, the creation of novel financial services and products that are suited to the particular requirements of marginalized communities may be hampered by regulatory shortcomings. Potential providers could be reluctant to enter these markets in the absence of clear regulations and protections, which would worsen the lack of access to financial services. As a result, it becomes more difficult for governments and companies in underdeveloped nations to obtain the capital required for sustainable projects since access to green financing solutions is limited.

-

-

Regulatory deficiencies in developing countries (Element 4) at level V influence data gaps and technological barriers (Element 7) at level IV. There are large gaps in the data available to evaluate financial performance and environmental implications in the absence of clear data disclosure and monitoring standards. The weak regulatory frameworks and ineffective enforcement practices frequently make it more difficult to gather, examine, and share important data across a range of industries. Consequently, this hinders the uptake and application of innovative technology that might propel economic expansion and social advancement. In addition to technological obstacles like restricted access to sophisticated technologies, this dearth of trustworthy data makes it difficult to monitor and assess green funding programs. Inadequate regulations may discourage innovators and possible investors from entering these sectors by fostering an atmosphere of uncertainty. The difficulties in gaining access to and utilizing cutting-edge technology are made worse by this lack of investment, which feeds a vicious cycle that increases the technological gap between developed and developing countries. As a result, investors are exposed to greater risks, and the lack of information and technology to make wise judgments slows the growth of green financing.

-

-

Access to financial products (Element 6) at level IV influences limited investor awareness (Element 3) at level III. People are empowered to make well-informed decisions about their wealth management and financial planning strategies when financial institutions and providers give a wide variety of investment options in addition to thorough information and educational materials. However, the range of investment options accessible to prospective investors is limited by the restricted availability of financial products in green financing. Investor knowledge stays low when few or poorly understood green financial solutions are available. Investors are less likely to become aware of these products’ advantages, dangers, and returns if they are not easily accessible. This lack of exposure maintains the cycle of low awareness, which impedes the expansion of green investments and the wider market adoption of sustainable financial practices. This dynamic emphasizes how crucial it is to have a transparent and inclusive financial environment that places a high value on investor education and fair access to investment options.

-

-

Data gaps and Technological Barriers (Element 7) at level IV influence limited investor awareness (Element 3) at level III. In green finance, data gaps and technology obstacles impede the gathering and sharing thorough, trustworthy data on financial returns and environmental effects. Investors struggle to obtain accurate and current information about sustainable investment prospects to completely comprehend the risks and rewards of green investments without strong data collection and analysis procedures and efficient technology solutions for information dissemination. The adoption of sustainable investment methods is ultimately hampered by this information gap, which impairs their capacity to make wise judgments. Consequently, investors continue to be uninformed or doubtful of the possibilities of green financing, which restricts their involvement in the industry. Technological barriers, such as insufficient digital infrastructure, data privacy concerns, and platform compatibility problems, can impede the seamless exchange of information crucial for investor education and awareness.

-

-

Data gaps and technological barriers (Element 7) at level IV influence measuring environmental returns (Element 8) at level III. The availability of large data gaps and technology constraints is one of the main obstacles to precisely estimating the environmental benefits and returns linked to green funding. The challenge of accurately evaluating the actual efficacy of green projects in the absence of standardized data on environmental impacts is made difficult by the lack of complete and trustworthy data sets as well as the limitations imposed by existing technical capabilities. Establishing baseline conditions, monitoring progress over time, and quantifying the observable impacts on environmental indicators like carbon emissions, resource consumption, and biodiversity preservation become difficult without strong and reliable data collection methods. This problem is made worse by inadequate methods for monitoring and reporting environmental effects, which raise questions about the true advantages. The development and legitimacy of green financing are hampered by the inability of stakeholders and investors to assess the effectiveness of green projects due to a lack of trustworthy data and instruments.

-

-

Circular economy integration (Element 9) at level IV influences measuring environmental returns (Element 8) at level III. Due to the difficulty of monitoring long-term, systemic effects, incorporating a circular economy into green finance poses difficulties in quantifying environmental returns. The emphasis on resource efficiency, waste reduction, and reuse in circular economy models makes it challenging to clearly and consistently measure the direct environmental benefits. The results of the circular economy frequently necessitate the use of complex data and cutting-edge technologies to monitor, in contrast to traditional linear models, where impacts are simpler to quantify. This makes it more difficult to assess environmental returns accurately and reduces investor confidence in the efficacy of these investments.

-

-

Greenwashing (Element 2) at level III influences high costs (Element 5) at level II. Greenwashing can raise the perceived risks and expenses of green funding. Transaction costs increase when stakeholders and investors require more due diligence and examination because they are concerned about possible greenwashing. Investment is discouraged by the higher total cost of green projects due to the additional layer of regulatory compliance and verification. As investors and project developers work to assure credibility and transparency, the possibility of greenwashing further erodes market trust and raises costs. Restoring this trust and rehabilitating the brand’s reputation can be costly and time-consuming, involving significant expenditures in public relations, marketing, and real sustainability projects. In the end, greenwashing can have serious financial repercussions since it not only falls short of the claimed cost-cutting and environmental advantages but also exposes the company to possible legal risks and harms its brand, which eventually raises operating expenses.

-

-

Measuring environmental returns (Element 8) at level III influences high costs (Element 5) at level II. Green financing requires sophisticated data collection, monitoring systems, and third-party verification, making it difficult and expensive to measure environmental benefits. This multifaceted approach is aimed at precisely measuring the environmental advantages that result from these investments, because these processes are inherently complex, it is difficult and expensive to measure ecological repercussions exactly. The data collection phase alone demands meticulous attention to detail, as it necessitates the methodical collection of a wide range of data regarding the project’s environmental footprint, resource consumption, and waste generation. This undertaking frequently calls for the use of specialized tools and the participation of skilled workers, which raises the related expenses even more. Accurately evaluating the environmental impact is made more expensive by the absence of standardized measures. Operational costs can also be increased by hiring subject matter experts, buying specialist equipment, and possibly changing procedures to conform to sustainable standards. Project developers and investors must spend money on knowledge and technology to monitor results, which adds a lot of overhead. These high measurement costs can discourage investment in green projects since it becomes more difficult to measure and justify the financial and environmental returns, which reduces the appeal of green financing.

-

-

High costs (Element 5) at level II influence lack of regulation standardization (Element 1) at level I. Businesses find it more difficult to grow green initiatives while navigating a complicated web of conflicting laws and regulations due to inconsistent legislation across different jurisdictions and industries. The establishment of standardized standards is hampered by the financial burden of compliance and the intrinsic complexity of various regulatory environments. Businesses and investors might not have the funds to handle a disjointed regulatory environment with different laws and compliance standards in different areas if green initiatives are costly to execute. Therefore, the absence of standardization raises the cost of green initiatives, deterring investment and delaying acceptance.

6.2. Policy Recommendations

-

-

Strengthening Regulatory Frameworks (Addresses Element 4, influencing Elements 6 and 7)

Enhancing their regulatory frameworks and enforcement capacities should be a top priority for emerging nations. Create and implement clear, strict, consistent regulatory frameworks for green finance. This covers standardized reporting forms, compliance monitoring, and explicit rules for environmental effect disclosures. This could also entail investing in regulatory body capacity-building projects, working with international organizations, and implementing best practices from more advanced financial markets. Developing countries can encourage wider access to green financial products, which will support economic growth, financial inclusion, and general social development. Reducing regulatory flaws will boost investor and financial institution trust in the system, increase accessibility to green financial products, and promote sustainable investments in developing nations.

-

-

Addressing Data and Technological Gaps (Addresses Element 7’s influence on Elements 3 and 8)

Invest in reliable data collection methods and cutting-edge monitoring technology to close information gaps and lower technological hurdles. Establishing thorough and open regulatory frameworks that support data collection and technological development must be a top priority for policymakers in emerging nations. Closing the knowledge and resource gaps may entail encouraging public-private collaborations, encouraging research and development projects, and simplifying bureaucratic procedures and creating unified databases to house financial and environmental information about green projects. Developing countries can expedite the adoption of revolutionary technologies and create more robust data ecosystems by addressing regulatory shortcomings head-on. This will ultimately enable them to realize their full economic and social potential. Enhanced technology capabilities and data transparency will empower investors to quantify environmental returns precisely, make well-informed decisions, and increase trust in green financing.

-

-

Promoting Awareness Among Investors (Responds to Element 3 as a dependent variable influenced by Elements 6 and 7)

These data gaps and technology obstacles must be addressed to facilitate better informed decision-making and promote efficient environmental policies and practices. To close these gaps and improve our knowledge of environmental returns, coordinated efforts are required to improve data collection techniques, use cutting-edge technologies like artificial intelligence, big data analytics, and remote sensing, and encourage cooperation among researchers, legislators, and industry stakeholders. Put focused training initiatives and educational campaigns in place to increase prospective investors’ knowledge of green financial solutions. The advantages, dangers, and financial gains of sustainable investments ought to be highlighted in these campaigns. Investors can obtain more trustworthy and useful information by creating an atmosphere that facilitates data availability and technology, ultimately leading to better decision-making and the uptake of sustainable investment. Raising awareness will promote involvement in green financing and broaden its adoption, assisting in breaking the circle of inadequate investor understanding.

-

-

Promoting the Integration of the Circular Economy (Addresses Element 9 → Element 8)

The integration of circular economy principles at the strategic level encourages cross-functional collaboration and knowledge sharing, enabling a more holistic approach to environmental performance measurement. Create regulations that encourage using circular economy concepts in environmentally friendly initiatives. Encourage the development of cutting-edge techniques for calculating the long-term environmental benefits of circular economy projects. Offering monetary rewards and technical support to initiatives implementing waste minimization and resource efficiency techniques can guarantee more accurate assessment and draw in investors.

-

-

Mitigating Greenwashing Risks (Linked to Element 2’s effect on Element 5)

Independent verification agencies should be established to certify green initiatives to ensure transparency and legitimacy. Companies claiming environmental benefits should be subject to strict due diligence and auditing procedures. These steps will cut transaction costs, rebuild market trust, and increase the affordability and investor attraction of green financing by lowering the dangers of greenwashing.

-

-

Reducing High Measurement Costs (Addresses Element 8 → Element 5 → Element 1)

Provide financial assistance for the expenses of data gathering, monitoring, and third-party verification for green projects, especially for startups and SMEs. By offering financial assistance to implement standardized criteria and assessment frameworks, project costs can be reduced overall, increasing the accessibility and appeal of green financing to investors and companies.

-

-

Harmonizing Regulations across regions (Addresses Element 5 → Element 1)

To lower the cost of compliance, work toward regional and global standardization of green finance laws. To enable the smooth expansion of green initiatives, harmonize regulations, certifications, and reporting requirements throughout jurisdictions. Global adoption of green finance will be accelerated, cross-border investments will be encouraged, and standardized laws will improve cost efficiency.

6.3. Specific Recommendations

To improve the practical utility of policy guidance, specific recommendations are delineated below for key stakeholder groups:

For Regulators:

-

-

Develop and enforce unified green finance frameworks and taxonomies, referencing best practices in disclosure requirements and climate risk stress testing.

-

-

Streamline approval processes for green bonds and clarify incentives for sustainable project financing.

For Banks and Financial Institutions:

-

-

Implement green credit risk assessment protocols, specialized lending products, and sector-specific training to address green project appraisal.

-

-

Collaborate with fintechs to promote inclusive access and transparency in green lending.

For SMEs:

-

-

Design support programs for capacity-building on climate reporting, facilitate access to dedicated green loan/grant schemes, and reduce compliance burdens for smaller firms.

For Investors:

-

-

Improve transparency through third-party certification, credible ESG reporting, and dedicated information portals; develop risk mitigation tools (e.g., guarantees) to build investor confidence.

7. Conclusions

It is vital to observe how systems approach in problem solving and decision making can first help to reduce the level of complexity prevailing in the system due to the presence of multiple elements and multiple interactions among them. Then, with the interpretation subjected to the concerned stakeholders, it aids in developing various options to reach to the solution. Hence, the interpretation task of the model becomes delicate. Multiple ways exist to reach the ultimate dependent element, starting from the lower end. The complex issues surrounding green financing in India are highlighted in this paper, with particular attention paid to the interaction of legislative shortcomings, data gaps, low awareness, exorbitant costs, and the possibility of greenwashing. A clear hierarchy of these issues was created using ISM, which identified regulatory shortcomings and financial product accessibility as the main motivators. The results highlight the importance of strong legal frameworks, technology innovations, and standardized procedures to improve transparency and simplify matters. Resolving these problems will increase investor trust, make it easier to assess environmental returns precisely, and reduce expenses overall. Additionally, including the concepts of the circular economy and reducing the likelihood of greenwashing can improve the legitimacy and allure of green finance programs. To speed up sustainable financial practices, policymakers must give data openness, regulatory harmonization, and capacity-building initiatives top priority.

This study offers novel insights using ISM to model the structural interdependencies among key barriers to green finance, moving beyond prior studies that often treat these factors in isolation. The model reveals a cascading influence, with regulatory deficiencies acting as foundational drivers that shape downstream issues like data gaps, investor awareness, and cost structures. Notably, placing greenwashing as a reinforcing factor rather than a root cause provides a more nuanced understanding of systemic vulnerabilities. This hierarchical perspective helps clarify the sequencing of policy priorities, particularly in contexts with fragmented regulatory environments. By grounding the interpretive model in contextual realities and supported by empirical references, the study enhances the theoretical depth and practical utility of existing green finance literature. Despite relying on expert-driven modeling, triangulation with real market data enhances the validity of the findings. Incorporating bond issuance volumes, project performance data, and regulatory actions offers practical grounding to the ISM-derived insights. This dual strategy involving both interpretive modeling and empirical referencing helps increase contextual reliability and mitigates concerns related to theoretical abstraction.

Green funding is still a vital initiative in the collective effort to lessen the negative effects of human activity on the environment, despite the difficulties presented by the complex requirements. The need for transparent and verifiable environmental performance indicators will only grow as society’s awareness of sustainability continues to develop, highlighting the need for strong and thorough measurement frameworks.

The ISM technique, which is interpretive and dependent on the experts’ opinions, is one of the study’s limitations. The results may not adequately reflect India’s dynamic and ever-changing green finance issues. Furthermore, the study’s primary focus on the Indian context may limit its generalizability to other areas with different social, economic, and regulatory contexts. Notably, while ISM structures challenges hierarchically, it does not inherently quantify the relative severity, frequency, or likelihood of each challenge. Integrating quantitative tools such as the Analytic Hierarchy Process (AHP), fuzzy logic modeling, or expert-based weighting within or alongside the ISM framework would enable prioritization of obstacles based on their practical impact or urgency. Such hybrid approaches are increasingly utilized in sustainability and finance research to offer actionable rankings for decision-makers. Future work can enhance the utility of this study by adopting multi-method prioritization strategies to guide resource allocation and policy interventions more effectively. Another limitation is the lack of empirical support for the suggested links, as integrating data from the real world could provide stronger findings. In order to evaluate and improve the links found in this work, future research can broaden the scope by integrating empirical studies and data-driven approaches like system dynamics or structural equation modeling. A more comprehensive picture of the difficulties in global green funding can be obtained through comparative studies conducted in various nations or areas. Additionally, investigating how cutting-edge technology like blockchain and artificial intelligence may be used to solve the complexity of green finance can provide creative answers for efficiency and scalability.

Author Contributions

Conceptualization, S.S.; Methodology, H.K.; Software, H.K.; Validation, S.S. and H.K.; Formal Analysis, H.K.; Investigation, S.S.; Writing—Original Draft Preparation, S.S.; Writing—Review & Editing, H.K.; Visualization, S.S.; Supervision, H.K.

Ethics Statement

Not Applicable.

Informed Consent Statement

Not Applicable.

Data Availability Statement

Not Applicable.

Funding

This research received no external funding.

Declaration of Competing Interest

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

References

-

1.

Sachs JD, Woo WT, Yoshino N, Taghizadeh-Hesary F. Why is green finance important? Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3327149 (accessed on 19 March 2019).

-

2.

Amidjaya PG, Widagdo AK. Sustainability reporting in Indonesian listed banks: Do corporate governance, ownership structure and digital banking matter?

J. Appl. Account. Res. 2020,

21, 231–247.

[Google Scholar]

-

3.

Lee CF, Baral P. Green Finance Opportunities in ASEAN; UNEP Report: Nairobi, Kenya, 2017.

-

4.

Liu R, Wang D, Zhang L, Zhang L. Can green financial development promote regional ecological efficiency? A case study of China.

Nat. Hazards 2019,

95, 325–341.

[Google Scholar]

-

5.

Ali EB, Anufriev VP, Amfo B. Green economy implementation in Ghana as a road map for a sustainable development drive: A review.

Sci. Afr. 2021,

12, e00756.

[Google Scholar]

-

6.

Haines A, Smith KR, Anderson D, Epstein PR, McMichael AJ, Roberts I, et al. Policies for accelerating access to clean energy, improving health, advancing development, and mitigating climate change.

Lancet 2007,

370, 1264–1281.

[Google Scholar]

-

7.

Mumtaz MZ, Smith ZA. Green finance for sustainable development in Pakistan.

IPRI J. 2019,

19, 1–34.

[Google Scholar]

-

8.

Taera EG, Lakner Z. Sustainable Finance: Bridging Circular Economy Goals and Financial Inclusion in Developing Economies.

World 2025,

6, 44.

[Google Scholar]

-

9.

Awan U, Sroufe R, Shahbaz M. Industry 4.0 and the circular economy: A literature review and recommendations for future research.

Bus. Strateg. Environ. 2021,

30, 2038–2060.

[Google Scholar]

-

10.

Berensmann K, Lindenberg N. Green finance: Across the universe. In Corporate Social Responsibility, Ethics and Sustainable Prosperity; World Scientific: Singapore, 2019; pp. 305–332.

-

11.

Krushelnytska O. Introduction to Green Finance; World Bank. Global Environment Facility (GEF): Washington, DC, USA, 2017.

-

12.

Jhamb A. FinTech Adoption and Financial Inclusion in Rural India.

J. Neonatal Surg. 2025,

14, 3054–3062. doi:10.63682/jns.v14i32S.7884.

[Google Scholar]

-

13.

Duvendack M, Sonne L, Garikipati S. Gender inclusivity of India’s digital financial revolution for attainment of SDGs: Macro achievements and the micro experiences of targeted initiatives.

Eur. J. Dev. Res. 2023,

35, 1369–1391.

[Google Scholar]

-

14.

Islam MA, Yousuf S, Hossain KF, Islam MR. Green financing in Bangladesh: challenges and opportunities–a descriptive approach.

Int. J. Green Econ. 2014,

8, 74–91.

[Google Scholar]

-

15.

Rashid MHU, Uddin MM. Green financing for sustainability: analysing the trends with challenges and prospects in the context of Bangladesh.

Int. J. Green Econ. 2018,

12, 192–208.

[Google Scholar]

-

16.

Amran A, Nejati M, Ooi SK, Darus F. Exploring issues and challenges of green financing in Malaysia: Perspectives of financial institutions. In Sustainability and Social Responsibility of Accountability Reporting Systems: A Global Approach; Springer: Berlin, Germany, 2018; pp. 255–266.

-

17.

Falcone PM, Sica E. Assessing the opportunities and challenges of green finance in Italy: An analysis of the biomass production sector.

Sustainability 2019,

11, 517.

[Google Scholar]

-

18.

Chen JM, Umair M, Hu J. Green finance and renewable energy growth in developing nations: A GMM analysis.

Heliyon 2024,

10, e33879.

[Google Scholar]

-

19.

Desalegn G, Tangl A. Enhancing green finance for inclusive green growth: A systematic approach.

Sustainability 2022,

14, 7416.

[Google Scholar]

-

20.

Lee JW. Green finance and sustainable development goals: The case of China.

J. Asian Financ. Econ. Bus. 2020,

7, 577–586.

[Google Scholar]

-

21.

Ozili PK. Green finance research around the world: a review of literature.

Int. J. Green Econ. 2022,

16, 56–75.

[Google Scholar]

-

22.

Bhattacharyya R. Green finance for energy transition, climate action and sustainable development: overview of concepts, applications, implementation and challenges.

Green Financ. 2022,

4, 1–35.

[Google Scholar]

-

23.

Mohanty S, Nanda SS, Soubhari T, S VN, Biswal S, Patnaik S. Emerging research trends in green finance: A bibliometric overview.

J. Risk. Fina. Manag. 2023,

16, 108.

[Google Scholar]

-

24.

Ayaz G, Zahid M. Trends, shifts and future prospects of sustainable finance research: A bibliometric analysis.

Sustain. Account. Manag. Policy J. 2024,

15, 1094–1117.

[Google Scholar]

-

25.

Krastev B, Krasteva-Hristova R. Challenges and trends in green finance in the context of sustainable development—A bibliometric analysis.

J. Risk. Fina. Manag. 2024,

17, 301.

[Google Scholar]

-

26.

Agarwal R, Bhadauria A, Kaushik H, Swami S, Rajwanshi R. ISM-MICMAC-based study on key enablers in the adoption of solar renewable energy products in India.

Technol. Soc. 2023,

75, 102375.

[Google Scholar]

-

27.

Manera K, Hanson CS, Gutman T, Tong A. Consensus methods: nominal group technique In Handbook of Research Methods in Health Social Sciences; Springer: Singapore, 2019; pp. 737–750.

-

28.

Delbecq AL, Van de Ven AH. A group process model for problem identification and program planning.

J. Appl. Behav. Sci. 1971,

7, 466–492.

[Google Scholar]

-

29.

Vahedian-Shahroodi M, Mansourzadeh A, Shariat Moghani S, Saeidi M. Using the nominal group technique in group decision-making: A review.

Medi. Educ. Bull. 2023,

4, 837–845.

[Google Scholar]

-

30.

Kaushik H, Rajwanshi R. Examining the linkages of technology adoption enablers in context of dairy farming using ism-micmac approach.

Res. World Agric. Econ. 2023,

4, 68–78.

[Google Scholar]

-

31.

Bhadauria A, Rajwanshi R, Agarwal R, Kaushik H. Examining the interlinkages among the virtual experiential technique’s influencing factors in the ecommerce industry: An ism and micmac approach.

Rama. Int. J. Bus. Res. 2022,

7, 67–82.

[Google Scholar]

-

32.

Kaushik H, Kaushik S. A study on the associations among the factors influencing digital education with reference to Indian higher education.

Educ. Inf. Technol. 2024,

29, 14999–15023.

[Google Scholar]

-

33.

Warfield JN. An Assault on Complexity; Battelle, Office of Corporate Communications: Columbus, OH, USA, 1973.

-

34.

Saxena J, Sushil, Vrat P. Policy and Strategy Formulation: An Application of Flexible Systems Methodology; GIFT Pub.: New Delhi, India, 2006.

-

35.

Warfield JN, Cárdenas AR. A Handbook of Interactive Management; Iowa State University Press Ames: Ames, IA, USA, 1994.

-

36.

Srivastava S, Kaushik H, Khemani S, Kaur J. Analysing the total interactions amid elements of entrepreneurial education.

Rev. Educ. 2025,

13, e70055.

[Google Scholar]

-

37.

Kaur J, Srivastava S, Kaushik H. FISM-FMICMAC-based analysis of challenges affecting potato processing by SMEs in India.

J. Agribus. Dev. Emerg. Econ. 2025. https://doi.org/10.1108/JADEE-05-2024-0160.

[Google Scholar]

-

38.

Seth S, Kaushik H. Linkages among AI elements affecting quality and value of education.

Int. J. Chang. Educ. 2025. doi:10.47852/bonviewIJCE52023973.

[Google Scholar]

-

39.

Ahmad N, Qahmash A. Smartism: Implementation and assessment of interpretive structural modeling.

Sustainability 2021,

13, 8801.

[Google Scholar]

-

40.

Kaushik H. Advocating ‘eco-village’ for sustainable development: The dayalbagh way of life. Eco Cities. 2024; 5 (1): 2773.

Coast. Manag. 2013. doi:10.54517/ec.v5i1.2773.

[Google Scholar]

-

41.

Agustin IN, Mahendra RA, Hesniati H. How does Green Finance affect the environment in the ASEAN emerging countries?

Econ. J. Emerg. Mark. 2025,

29, 70–81.

[Google Scholar]

-

42.

Ridho TK, Vinichenko MV. Evaluation of sustainable finance implementation in emerging markets.

J. Policy Soc. 2023,

1, 468–468.

[Google Scholar]