1. Introduction

In the grand blueprint of China’s rural revitalization strategy, rural finance plays an essential role, particularly consumer credit, which is gradually becoming a vital financial tool for supporting the daily lives and long-term investments of rural households. With the development of the economy and the deepening of the financial market, the financial demands of rural households for housing improvement, educational investment, healthcare, and other living needs are increasingly growing. These demands have introduced a variety of credit and service needs and driven the expansion of the consumer credit market, emerging as a pivotal force in fostering rural economic development [

1,

2].

In rural China, many households face unmet credit needs due to limited collateral and lack of credit histories [

3], which heightens lending risks for financial institutions and hinders effective credit allocation to rural areas [

4]. This challenge has led to a higher reliance on informal credit, especially for consumer credit demand, where friends, relatives, or private lenders are turned to for financial support. Nonetheless, the push for rural revitalization has led to efforts to increase the reach and flexibility of credit services. China’s 14th Five-Year Plan explicitly emphasizes the necessity of establishing and refining a modern rural financial system characterized by adaptability, competitiveness, and inclusiveness. No. 1 Central Document for the year 2024 further underscores the importance of delving deeper into rural financial services’ breadth, depth, and precision. Precisely addressing the service gaps in finance for rural areas and residents is key to optimizing inclusive financial services in agriculture and safeguarding the financial well-being of rural residents [

5]. Despite these efforts, challenges remain in providing consumer credit to rural households. The lack of innovative consumer credit products exacerbates the issue, as they fail to accommodate rural households’ diverse consumer credit needs [

6]. Moreover, rural households’ limited financial management skills and market understanding further hinder their access to credit [

7].

To address the discrepancy between the strong macro-level demand and the unfulfilled micro-level needs, it is imperative to look deeper into the nature of the consumer credit needs of rural households and the intrinsic linkages between these needs and their income structure and asset structure [

8]. The composition and diversity of rural households’ income are key factors that influence their consumer credit demand, directly impacting the household’s cash flow and debt servicing capacity [

9]. A stable and diversified income enhances a household’s consumption capacity and drives up their demand for credit. For households with a single and low income, their credit demand may be more focused on meeting basic living needs. In contrast, for those with diverse income sources and higher income levels, their credit demand may tend more towards investment and consumption upgrades.

The asset structure of rural households forms the foundation of rural household wealth [

10], including land, housing, financial assets, etc., and provides a sense of economic security, directly affecting their credit demand and ability to obtain credit [

11]. Households with more assets can often provide more collateral when applying for credit, thereby increasing the possibility of obtaining credit. The diversity of assets also means that households have more opportunities to allocate assets to meet different consumption and investment needs.

Studying the relationship between the consumer credit demand of rural households and their income and asset structures is of great significance for understanding how rural households meet their diverse living needs through credit. This not only helps to reveal the intrinsic motivations for consumer credit demand among rural households but also provides a reference for financial institutions on how to better serve the rural market, innovate financial products, and improve service quality. By deeply analyzing the financial situation of rural households, their consumer credit demand characteristics and trends can be more accurately grasped, thus providing rural households with credit products and services that are more in line with their actual needs, promoting the comprehensive development of the rural economy and the improvement of residents’ quality of life.

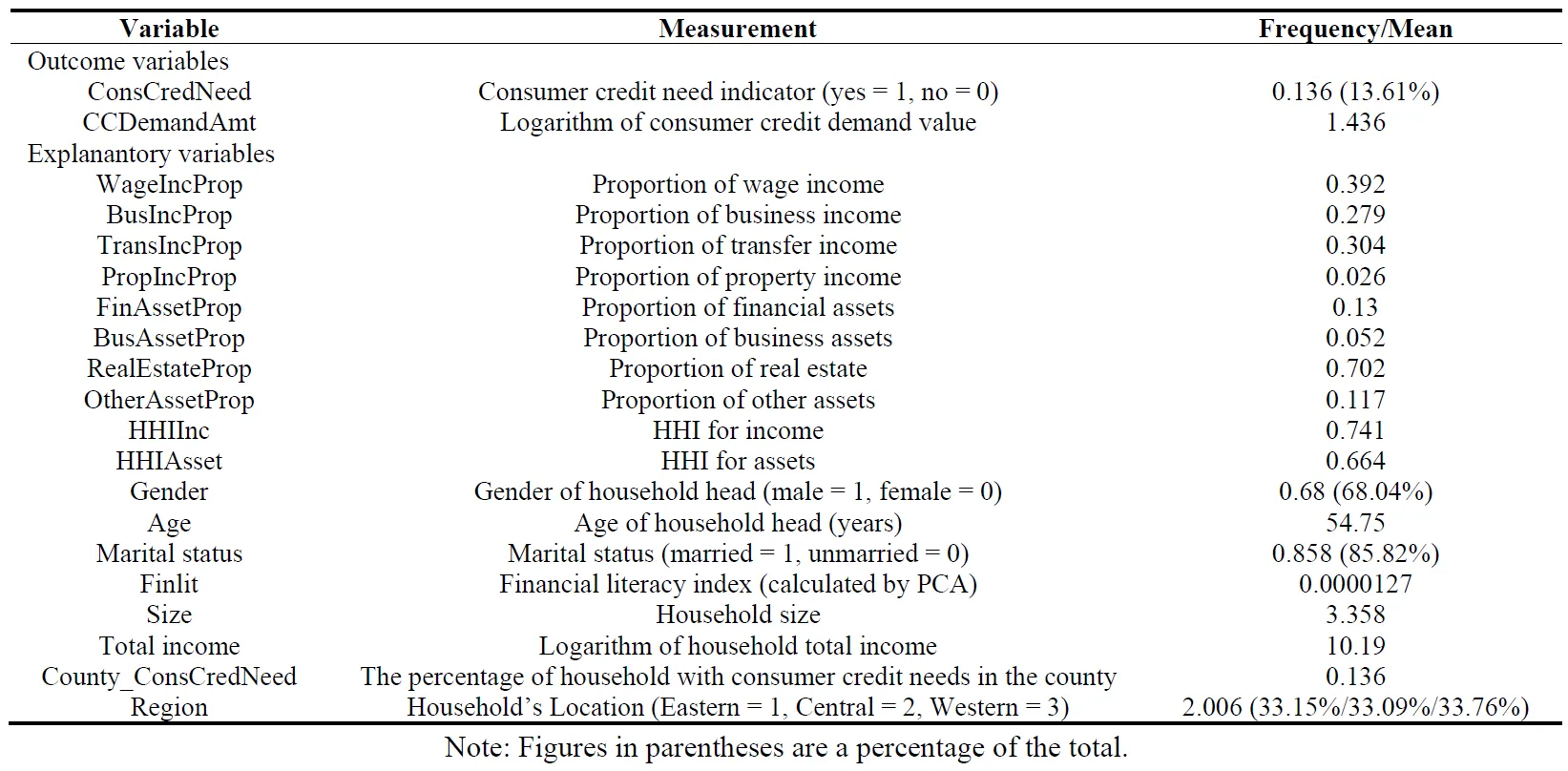

In our empirical analysis, leveraging the 2019 China Household Finance Survey (CHFS) data, we organized and calculated income and asset structures, andthe HHI indexes for both income and assets, focusing on rural households. Our aim was to construct various measures that reflect income and asset structures among these households. Given our interest in understanding rural household consumer credit demand, we chose the required amount of consumer credit as our key metric.

We established an observational sample comprising 11,386 rural households. To explore the relationship between the income and asset structures of these households and their consumer credit demand, we adopted the Heckman two-stage model. This approach helped us address potential concerns regarding the endogeneity of consumer credit amounts. In the first stage, a probit regression analyzed the factors influencing rural households’ decisions to seek consumer credit, with the inclusion of the proportion of consumer credit among peers in the same county to impose exclusion restrictions. Using the outcomes from the first stage, we derived the inverse Mills ratio, which was then incorporated into the second-stage regression. Our results indicate that households with a higher share of wage income, business income, and transfer income tend to have lower consumer credit demand level. In contrast, those with a larger proportion of financial assets exhibit greater consumer credit demand. Additionally, we explored the variations in these relationships with respect to the diversity of income and assets, as well as the potential heterogeneities brought by the household head’s age and geographical region.

Our study contributes to the existing literature by enhancing the understanding of the determinants of rural household consumer credit demand. Recent studies have examined the impact of factors such as farmers’ income [

12], consumption habits [

2], monetary policy interest rate [

13], and gender difference [

14] on rural consumer credit demand. Our study emphasizes the pivotal role of household income and asset structures, aligning with the traditional view that a household’s financial condition is a key determinant of its borrowing behavior. By revealing how specific aspects of income and asset diversification influence credit demand among rural households, our findings, however, shed light on the specific dynamics of this relationship, offering a more refined comprehension of rural household credit demand.

Moreover, our study enriches the literature on the economic behavior of rural households. The results reveal that the credit-seeking behavior of surrounding peers significantly influences a household’s choice to seek consumer credit. The effects of structure and diversity of income and assets on the amount of credit demanded are distinct, highlighting the complex economic interplays within households. The notable influence of peer behavior reflects the importance of social factors and community norms in shaping financial decisions. In contrast, the role of income and assets in credit demand amounts points to the household’s economic stability and debt management capacity. This distinction emphasizes the multifaceted nature of rural household engagement in credit markets, underscoring the need for a more profound understanding of their financial conditions, needs, and behavioral tendencies to grasp the intricacies of rural financial markets fully.

The remainder of the paper is structured as follows. Section 2 reviews the related literature. Section 3 describes the data and the measurement of key variables. Section 4 presents the empirical strategy. Section 5 delves into the empirical analysis results. Section 6 concludes the study.

2. Literature Review and Hypotheses

The credit demand of rural households in China is a multifaceted phenomenon, shaped by a complex interplay of economic, behavioral, and lifecycle factors [

15,

16,

17], which aligns with the literature on consumer credit in developed economies [

18]. Economic conditions play a foundational role in shaping credit demand. These reviews generally conclude that borrowing patterns vary widely [

19], reflecting the economic landscape in rural China [

20], characterized by lower income levels and greater income volatility [

9,

12,

21,

22]. This leads to a higher reliance on credit to smoothen consumption [

2,

23], similar to the patterns observed in the U.S. consumer credit market [

24]. The limited access to formal financial services and the prevalence of informal credit circuits, often due to a lack of collateral or credit history, impose credit constraints that echo the liquidity restrictions discussed in the literature [

20,

25,

26].

Behavioral economics offers insights into the decision-making processes of rural households when it comes to borrowing [

27]. Our study argues that the tendency to use heuristics and mental accounting, as highlighted in studies on consumer credit behavior, may lead to credit decisions that are not fully rational but are instead influenced by cognitive biases and simplification strategies [

27,

28,

29]. Rural households might resort to credit to manage immediate financial distress or to finance large purchases that provide long-term utility, such as education and healthcare, which aligns with the concept of precommitment and mental accounting [

12,

20,

30].

The lifecycle theory further enriches our understanding of rural household credit demand by illustrating how financial needs evolve over time [

31]. Younger rural families may accumulate debt to invest in homes and education, anticipating future income growth, while older households may prioritize debt repayment and savings for retirement. This pattern of credit usage is consistent with the lifecycle model, which posits that individuals plan their consumption over a lifetime to maintain a stable level of well-being [

32,

33]. Cultural and social factors also play a crucial role in shaping the credit behavior of rural households. Traditional values and expectations around family responsibilities can lead to borrowing for events such as weddings and education [

12,

34,

35]. Furthermore, the preference for informal lending arrangements within social networks, due to their accessibility and simplicity, reflects the importance of social relations in rural financial transactions [

36].

In China, rural households’ economic behaviors and production decisions are significantly influenced by their income and asset levels [

37]. As the Chinese economy transforms and rural development accelerates, the sources of income and the composition of assets for rural households have changed markedly [

38]. These evolutions have profound implications for household consumption patterns, savings behavior, and credit demand [

20].

Income levels and structures directly affect the credit demand for consumption among rural households. In recent years, the increase in rural household income has been primarily driven by the rise in wage income associated with the expansion of non-agricultural employment opportunities [

39]. According to research by Zhu et al. (2022), wage income from non-agricultural employment has become rural households’ main driver of income growth [

40]. The rise in income strengthens families’ purchasing power [

41], making them more inclined to consider credit options when faced with substantial expenses [

35]. However, the instability of wage income can also lead to an increase in precautionary savings to cope with future income uncertainty [

42], which may, to some extent, suppress the growth of consumer credit demand [

43].

Asset levels and structures also play a crucial role in the economic decisions of rural households. The deepening of rural land system reforms has brought additional asset benefits to rural households through the transfer of land contracting rights and homestead use rights [

44]. Li et al. (2019) point out that the transfer and capitalization of land assets have enhanced the wealth effect of rural households, improving their creditworthiness and thus reducing the barriers to borrowing [

45]. Moreover, as the rural financial market develops, the holding of financial assets by rural households is also increasing [

46], providing more investment channels and collateral options [

47], which in turn increases their likelihood of obtaining credit [

48]. Nonetheless, the demand for consumer credit among rural households is not solely determined by income and asset levels. Still, it is also influenced by various factors such as family characteristics, education levels, and health conditions.

By examining consumer credit demand through the Family Life Cycle Theory, we recognize distinct credit needs among families as they progress through different life stages, aligning with the patterns observed in Chinese rural households. The theory suggests that households’ economic requirements and spending habits evolve over time. Younger families often prioritize housing and daily necessities, while older families may focus on their children’s education and preparing for healthcare. The composition of a household’s income and assets plays a crucial role in shaping consumer credit demands during these various stages [

49]. As a result, the diverse structures of income and assets among families lead to a range of consumer credit demands, reflecting their specific needs and priorities at each life stage.

Furthermore, the Family Life Cycle Theory indicates that households’ financial conditions and resource allocation change as they move through different life stages. The concentration of income and assets can significantly impact a household’s consumption capacity and credit demand. Families with a highly concentrated income might be more likely to make substantial purchases. At the same time, those with diversified assets might not need to rely heavily on borrowing, as they can utilize various assets to meet consumption needs.

Importantly, a household’s consumer credit demands and behaviors are also influenced by the age of the household head and the regional economic context, leading to notable differences in credit needs among families in similar life stages across different regions [

50].

Applying the Family Life Cycle Theory, we gain insights into the economic behaviors and shifts in demand that underpin our hypotheses, prompting us to propose the following:

Hypothesis 1 (H1). The structures of income and assets have varying degrees of impact on the amount of consumer credit demanded by rural households, and the modes of influence are likely to differ.

Hypothesis 2 (H2). Impacts of income and asset structures on the consumer credit demand of rural households is contingent upon the concentration levels of both income and assets.

Hypothesis 3 (H3). The age of the household head and the region in which the household is located will also introduce heterogeneity in the impact of income and asset structures on the consumer credit demand of rural households.

Our empirical examination addresses a gap in the literature by investigating how the structure of income and assets, including their diversity, influences the consumer credit demand of rural households. Unlike previous studies that have largely overlooked the specific impact of asset configuration on rural household economic behavior and the financial borrowing needs of rural families [

51], our study offers an in-depth examination of the ways in which income and asset structures shape the demand for consumer credit in rural settings. By using empirical indicators that capture the amount of consumer credit demanded rather than actual credit obtained, we aim to delve deeper into how households’ borrowing tendencies are shaped by their economic conditions and how they strategize their borrowing based on the diversity of their income and assets.

Additionally, we examined how household income and asset diversity affect their reliance on external borrowing and explored how household characteristics, such as the age of the household head and the region where the household is located, interact with income and asset structures to jointly influence consumer credit demand. Through our analysis, we aim to provide a more comprehensive perspective on the credit needs of rural households, understand their behavioral patterns under various economic conditions, and offer insights to policymakers and financial institutions on how to better meet the borrowing needs of rural families. This will aid in the design of more effective financial products and services to foster rural economic development.

3. Sample and Measurements

3.1. Sample and Data

The data for this study is derived from the microdata of the fourth wave of the China Household Finance Survey (CHFS), conducted in 2019 by the Survey and Research Center at Southwestern University of Finance and Economics. Launched in 2011, the CHFS has been biennial, focusing on capturing detailed insights into household financial behaviors and conditions across China. The CHFS uses a stratified, three-stage probability proportional to size sampling method, covering 29 provinces in China and excluding certain regions. It involves selecting cities/counties, then community or village committees, and finally households, ensuring a representative sample. The 2019 survey included 34,643 urban and rural households across 170 cities and 345 districts/ counties, providing a comprehensive and diverse dataset. Our analysis focuses exclusively on rural households, and to ensure the robustness of our findings, we have applied a winsorization technique to the top 3% of observations based on household income and the top 1% based on asset ownership. This helps mitigate extreme values’ influence that could skew the results. Additionally, we have excluded a small number of cases with excessive missing data to maintain the integrity and reliability of our analysis. After these adjustments, our final dataset consists of 11,386 rural household observations, which provides a substantial and representative sample for examining the relationship between income, asset structures, and consumer credit demand within the rural sector.

3.2. Income and Asset Structures

In this study, we analyze the impact of income and asset structures on rural household consumer credit demand by examining two key dimensions: the proportion of various income and asset sources and the diversity of these income and asset streams, as measured by the Herfindahl-Hirschman Index (HHI). Specifically, the HHI in this context is applied to gauge the concentration of a household’s income and asset mix by summing the squares of the shares of each income or asset category. A higher HHI indicates a more concentrated income or asset type source, while a lower HHI indicates a more diversified portfolio.

We categorize the income into four distinct types: wage income, which is derived from employment; business income, encompassing revenues from agricultural and commercial activities; transfer income, denoting non-employment and non-business income sources like government transfers, gifts, and inheritances; property income, which includes earnings from assets such as real estate, stocks, and bonds through rents, interests, and dividends.

Similarly, we segment assets into four categories: financial assets, which are liquid assets such as bank deposits, equities, bonds, and mutual funds; business assets, representing the capital invested in the operational activities of the household, including machinery, inventory, and other business-related property; real estate, comprising immovable properties like land, houses, and shops; and other assets, a residual category for vehicles, collectibles, and other valuables not fitting into the other asset classes.

3.3. Consumer Credit Demand

Our study focuses on the consumer credit demand of rural households. Accordingly, we have selected an indicator of consumer credit demand based on the survey question: “How much money (in yuan) does your family currently need to borrow for reasons such as buying a house, purchasing a car, education, medical treatment, and daily consumption?”. Given the limitations of the data, we have not taken into account whether these credit needs will be fulfilled through formal financial institutions or the accessibility of such borrowing.

3.4. Controls

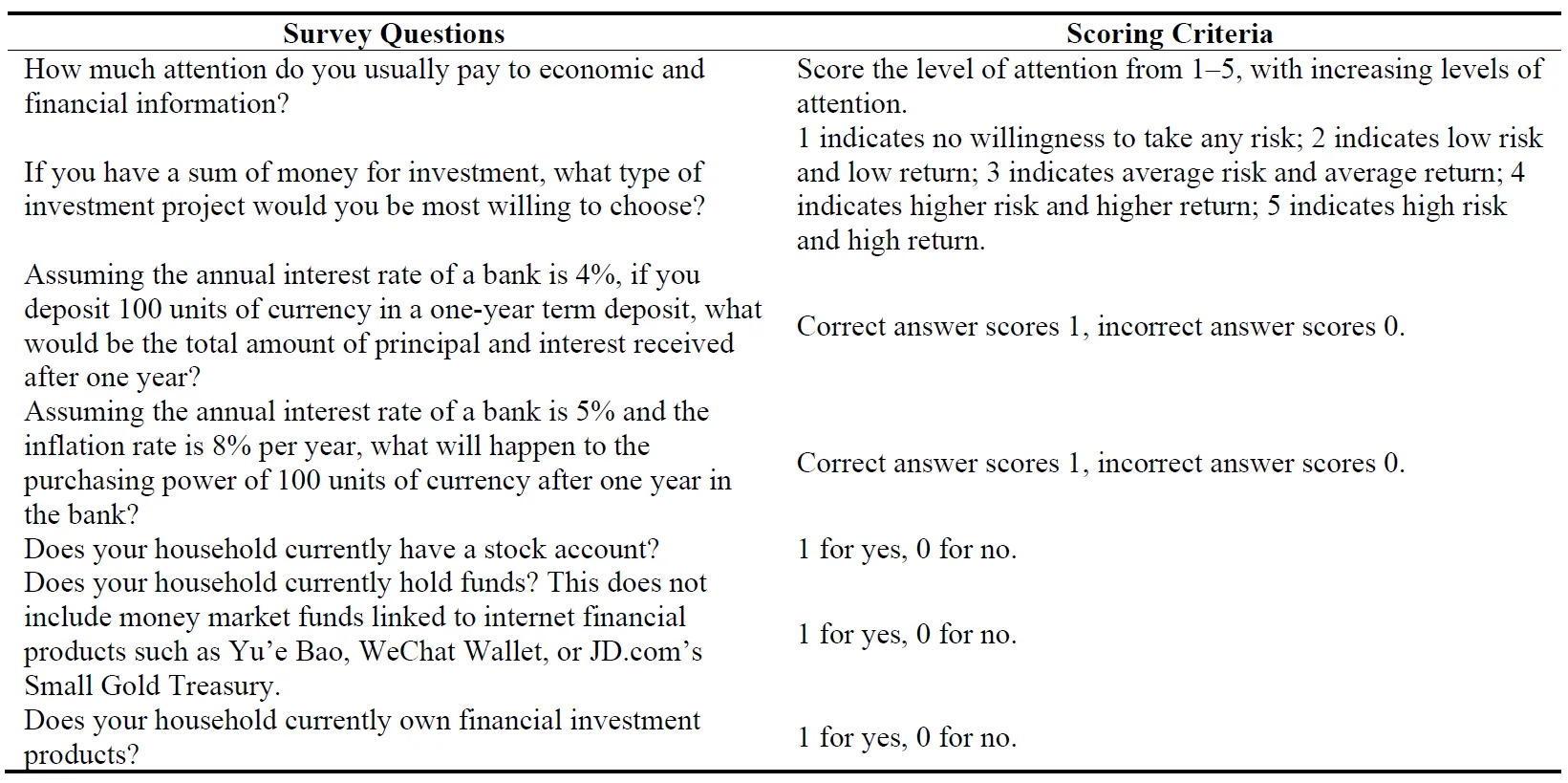

This paper presents two kinds of control variables to reduce model estimate bias from omitted variables: first, household head characteristics, including the household head’s gender, age, marital status and financial literacy; second, household characteristics, including the household size and the total income. Meanwhile, regional dummy variables are generated to control regional differences ().

Regarding the measurement of financial literacy variables, this study employs Principal Component Analysis (PCA) to extract key dimensions from seven questions in the CHFS2019 survey that effectively reflect the financial knowledge and behaviors of rural households. The specific information for each question is presented in .

. Financial literacy indicators.

Initially, the KMO test and Bartlett’s sphere test were conducted to assess the suitability of the data for PCA. Based on the criterion of eigenvalues greater than one, three principal components were retained, accounting for 19.83%, 18.73%, and 14.71% of the variance, respectively. The cumulative variance explained by these components reaches 53.27%. Factors with an explanatory power greater than 0.4, which are highlighted in bold in , are deemed significant. Consequently, the three principal components (PCs) are more closely associated with rural households’ financial knowledge, participation in financial markets, and risk perception, as shown in . Consequently, the comprehensive financial literacy index is formulated as follows:

. Outcomes of PCA for financial literacy.

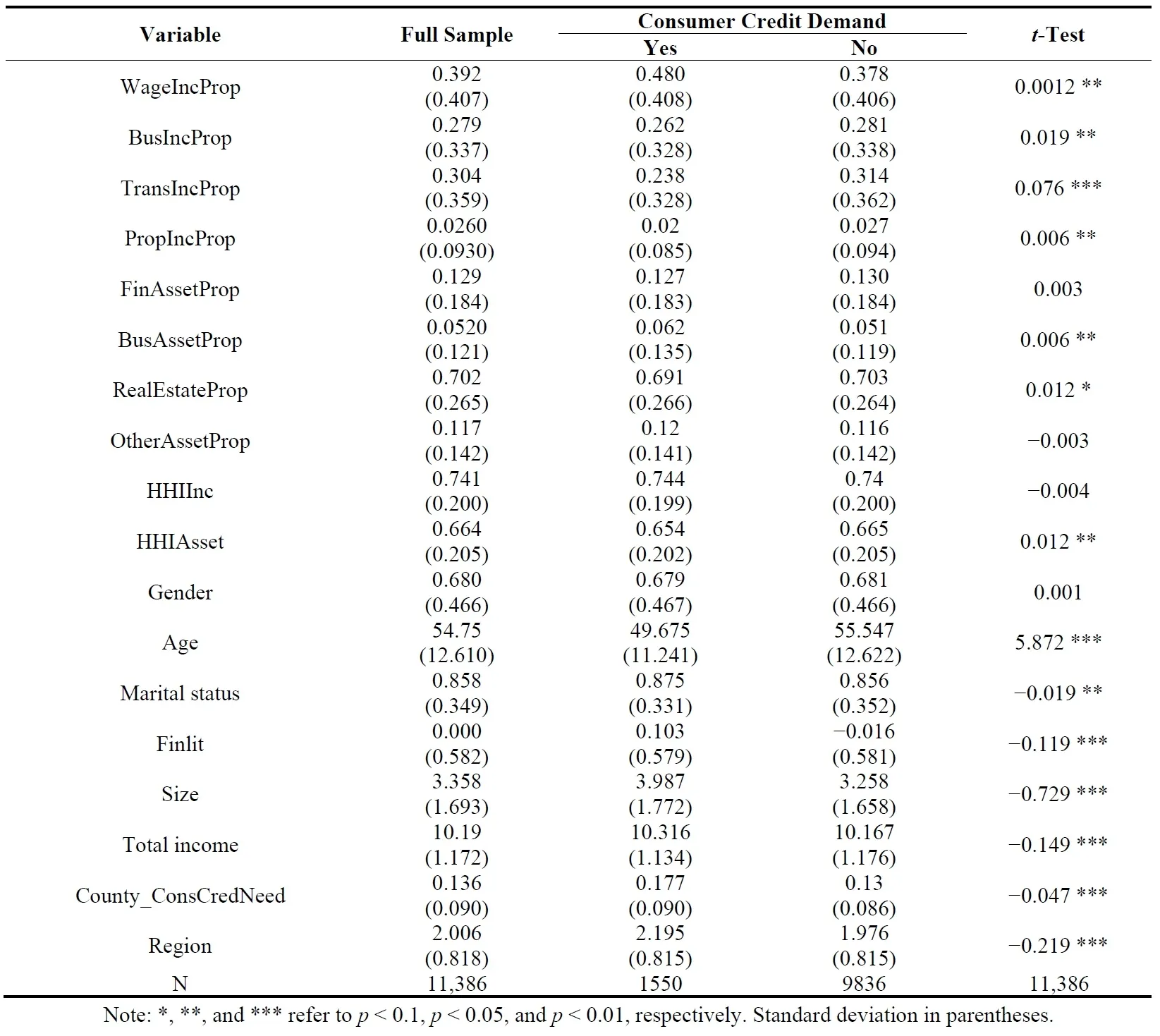

presents the descriptive statistics for all variables used in the analysis and reveals significant differences in the majority of household characteristics between households with consumer credit demand and those without.

. Descriptive statistics.

4. Empirical Strategy

To empirically investigate the relationship between the income and asset structures of rural households and their consumer credit demand, a critical consideration is the potential impact of sample self-selection bias, which may distort our understanding of the actual credit needs of these households. While our focus is on credit demand, the ability to obtain credit is often hindered by factors such as limited credit history, lack of collateral, and market information asymmetries. This suggests that some households, despite having latent consumer credit needs, may not actively seek or express their intention to borrow, making it challenging to ascertain the amount of their consumer credit demand.

Moreover, as our analysis does not consider the various ways rural households might satisfy their consumer credit needs, factors such as the hollowing out and aging of villages, which disrupt informal lending channels, could lead to self-selection biases in reporting consumer credit demands. Consequently, this may result in a non-random sample, with only 1550 out of the total surveyed households, representing 13.6%, indicating a need for consumer credit.

Thus, we employ a Heckman two-stage model. This approach allows us to correct for the endogeneity that arises from the non-random selection of households into the group that has expressed a consumer credit demand. In the first stage of the Heckman two-stage procedure, we examine the factors that determine whether a rural household seeks consumer credit. By accounting for this selection process, we aim to obtain more accurate estimates of the relationship between income and asset structures, and the levels of consumer credit demand reported by rural households in the second stage.

4.1. First-Stage Regressions: Determinants of Consumer Credit Need

In the first stage of the Heckman two-stage procedure, we examine the factors that determine whether a rural household chooses to seek consumer credit (ConsCredNeed) using the following probit regression:

where

ConsCredNeed is a binary indicator reflecting the household’s expressed need for consumer credit, derived from the survey question: “Does your family currently need to borrow for reasons such as buying a house, purchasing a car, education, medical treatment, and daily consumption?”. The vector

Xi encompasses the set of control variables that influence both the need to borrow and the amount of credit demanded. The vector

Zi includes additional variables for the selection model, which are potential determinants of consumer credit needs.

Lennox et al. (2012) argue that it is crucial to apply exclusion restrictions in the Heckman two-stage regression to ensure the identification of the model [

52]. This means that at least one variable in the first-stage model should influence the amount of consumer credit demanded solely through its impact on the decision to borrow. In this study, it is defined as the proportion of county-level consumer credit needs, representing the fraction of other rural households within the same county that has a need for consumer credit.

Drawing on previous research [

53], we posit that there are no direct economic pathways through which these county-level proportions affect the amount of consumer credit demanded beyond their influence on the borrowing decision itself. The need for consumer credit (

ConsCredNeed) is likely to be influenced by the consumer credit-seeking behavior of other households within the same county, as an increase in positive attitudes towards consumer credit and shifts in consumption and borrowing patterns among peers can significantly influence a household’s intent to borrow. However, the consumer credit-seeking behavior of others does not directly affect the amount of consumer credit demanded by an individual household. Thus, the Z variable is highly correlated with the endogenous variable and is theoretically uncorrelated with the error term in the second-stage equation, meeting the exclusivity requirement.

4.2. Second-Stage Regressions: Income & Asset Structures and Consumer Credit Demand Amount

To examine the relation between income and asset structures and household consumer credit demand amount, we estimate the following second-stage regression:

where

CCDemandAmt is the consumer credit demand amount of the household and

IncProp, and

AssetProp are the proportions of various income and asset sources, as defined in Section 3.

The set of control variables in our analysis is derived from established research [

3,

9,

54], which has consistently identified key demographic and economic factors that influence household credit demand. We account for the characteristics of the household head, such as gender, age and marital status, as these are often linked to life cycle stages, risk aversion, and economic stability, which in turn can affect the credit amount demanded to finance major life events like marriage, education, or raising children [

55]. The financial literacy of the household head is included as a control variable because it is a significant predictor of how effectively the household head can understand and utilize credit products, thereby impacting the amount demanded for credit [

26,

54]. Total household income is recognized as a direct determinant of the ability to repay loans, thus influencing the amount of credit a household may seek [

9]. Household size is also considered, as it is indicative of the household’s financial responsibilities and consumption needs; larger households typically have greater expenses and may require more substantial credit lines to meet those needs [

56]. The IMR, calculated based on the estimations from Equation (2), is incorporated to address the potential endogeneity associated with the decision to seek consumer credit. We have incorporated robust standard errors to address the potential issue of heteroskedasticity within our model.

5. Empirical Analysis

5.1. Baseline Regression

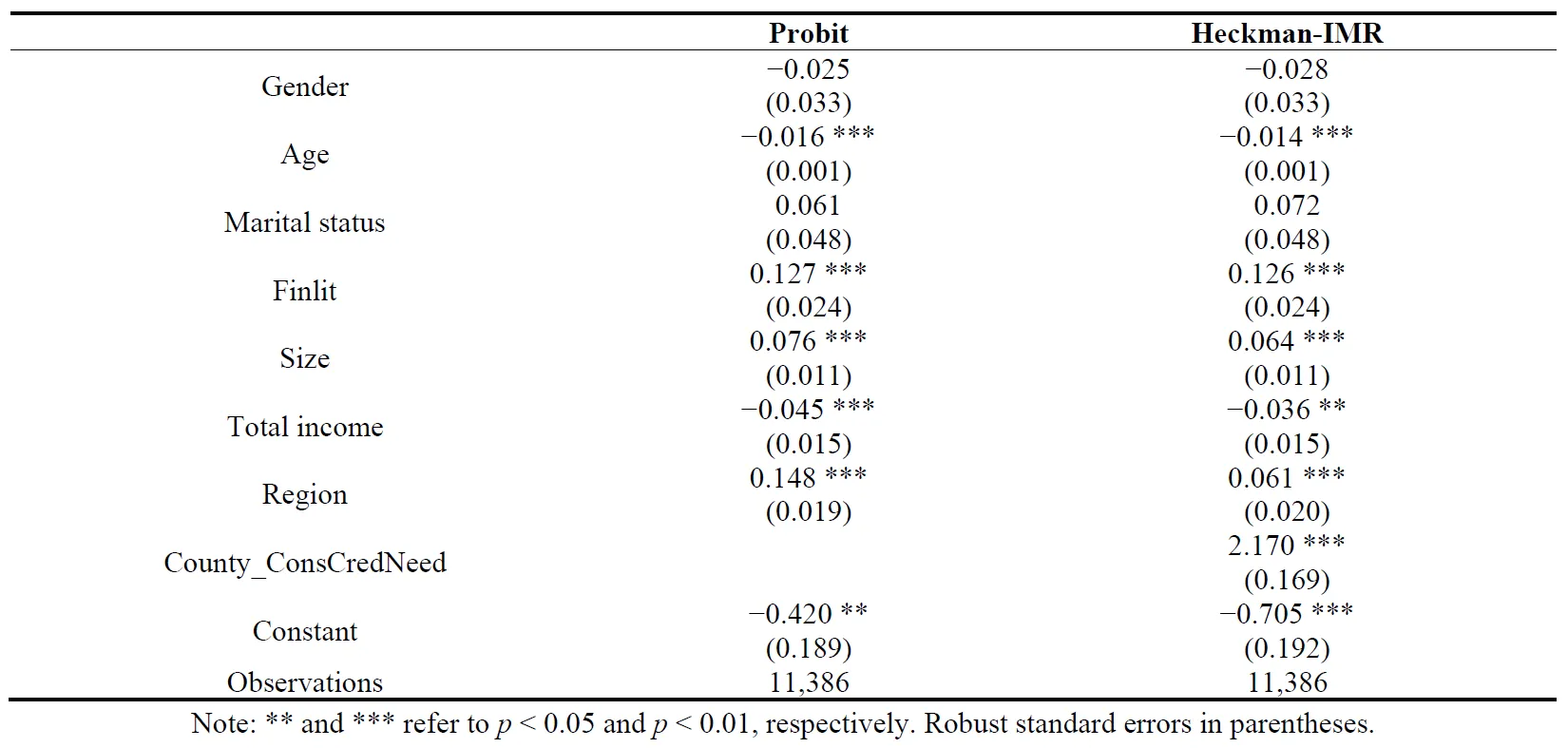

presents the findings from the estimation of Equation (3). In line with existing literature, financial literacy is confirmed as a significant predictor of consumer credit needs. Households with a need for consumer credit tend to have a younger household head and a larger household size [

57]. Additionally, households with a consumer credit need will likely report lower total income. The coefficients of the explanatory variables maintain their sign and significance when the Z variable is included, indicating that the selected Z variable exerts a substantial influence on households’ consumer credit needs. Utilizing the estimation results from Equation (3), we derive IMR for households’ consumer credit needs and integrate the ratio into the second-stage regression.

. First-stage probit model: Determinants of consumer credit need.

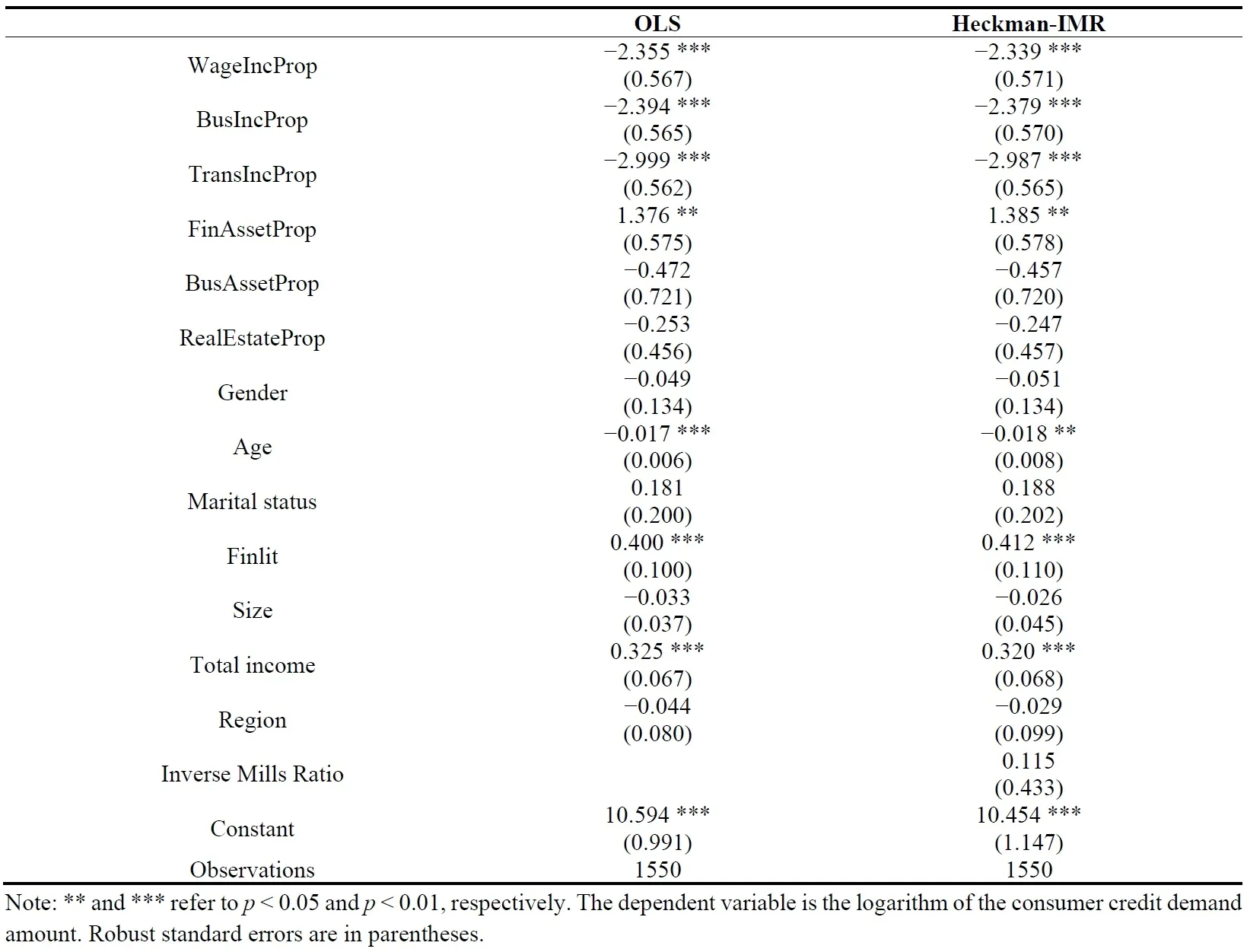

details the second-stage regression outcomes. Column 1 displays the results from a straightforward OLS regression, while Column 2 showcases the regression estimates after incorporating the IMR account for the endogeneity of consumer credit selection. Prior to the regression analysis, we conducted a covariance test to ensure the robustness of our model. The variance inflation factors (VIFs) for all variables, including the IMR, varied between 1.03 and 3.59, with the exception of the income proportion variables. The average VIF was 5.76, which indicates that multicollinearity was not a significant concern in our model. Although there is a notable similarity in the income proportions among Chinese rural households, the significant coefficients of all income proportion variables suggest that multicollinearity does not pose a substantial issue.

The insignificance of IMR coefficient may suggest that sample selection bias is not a predominant issue. This implies that the decision to seek credit in the first stage does not systematically affect the second stage, which pertains to the amount of credit demanded. In other words, households that did not report a need for credit in the survey are genuinely not inclined to borrow, indicating that the sample is not subject to significant selection bias that would skew the results of the credit demand analysis.

The coefficients for the proportions of wage income, business income, and transfer income are all negatively signed and statistically significant at the 1% level. This indicates that an increase in these income proportions is associated with a decrease in the amount of consumer credit demanded, reflecting a lower need for external borrowing when these income sources are more stable or sufficient. Conversely, the coefficient for the proportion of financial assets is positively signed and significant, suggesting that households with a larger share of financial assets in their portfolio are more likely to demand a higher amount of consumer credit, potentially due to their ability to use these assets as collateral or their familiarity with financial instruments. The coefficients for the proportions of other assets, such as real estate and other properties, are not statistically significant, indicating that these assets may not directly influence the amount of demand for consumer credit. These results suggest that the structure of income and assets indeed has varying impacts on the amount of consumer credit demand by rural households, with different modes of influence. Therefore, H1 is verified.

. Second-stage model: Income & asset structures and consumer credit demand amount.

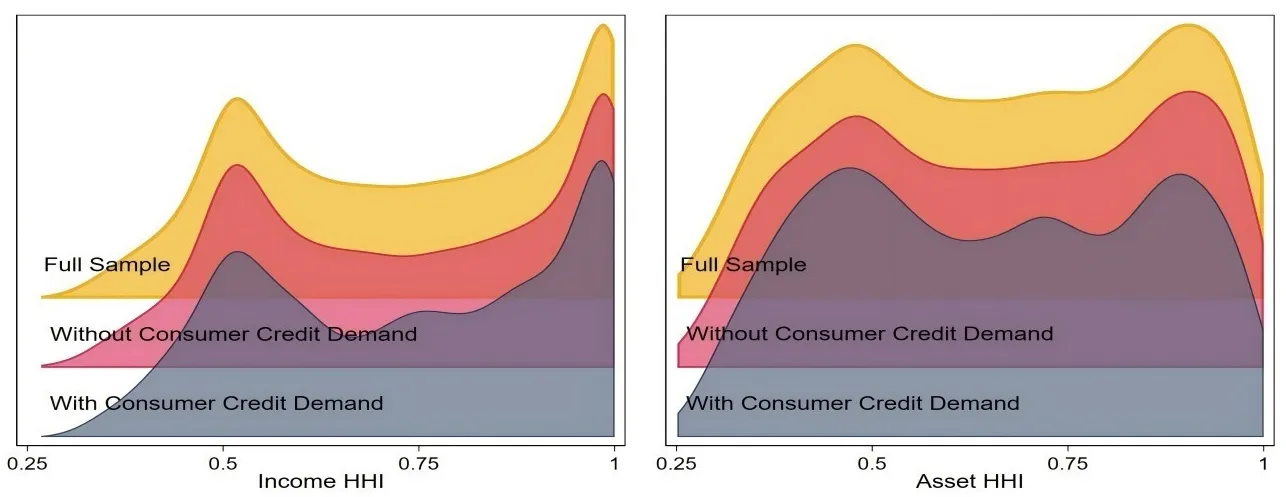

presents the distribution of the HHI for income and asset structures among rural households, highlighting two distinct patterns for each financial dimension.

For income HHI, the bimodal distribution indicates a dichotomy between households with concentrated income sources and those with a diversified income portfolio. The right peak, where HHI values approach 1, suggests a significant concentration of income from a single source. In both the full sample and the subsample without consumer credit demand, the majority of households rely predominantly on transfer income (37.5% and 39.02%, respectively), followed by wage income (34.69% and 33.19%). In contrast, households with consumer credit demand are more likely to be dominated by wage income (44.17%), with business income and transfer income being relatively equal (27.22% and 28.06%, respectively). This suggests that households seeking credit may have a greater reliance on wage income, potentially due to its regularity and predictability.

The left peak of the income HHI, with values around 0.5, indicates a more even distribution of income sources. Nearly half of the households in the full sample and those without consumer credit demand have a similar proportion of operational and transfer incomes (47.5% and 49%, respectively). Among households with consumer credit demand, a comparable share of operational and transfer incomes is observed (40%), with a notable increase in the reliance on wage income. This trend may reflect the influence of income diversity on credit-seeking behavior, as households with stable and diversified income streams might be more inclined to borrow for consumption.

Regarding assets HHI, the distribution is more uniform but still exhibits a bimodal trend. A high assets HHI, nearing 1, is predominantly associated with real estate, highlighting its dominance in the asset structure of rural households, irrespective of their consumer credit demand status. This is consistent across 96% of households in the overall sample and those without consumer credit demand.

In the left peak, where assets HHI values are around 0.45, there is an uptick in the proportion of operational assets. However, real estate remains the cornerstone of asset composition. The full sample reveals that 15.4% of households have more than half of their assets in financial assets, while 65.2% are heavily invested in real estate. For the subsamples without and with consumer credit demand, these figures are 14.75% and 70.96%, and 10.95% and 73.72%, respectively. This underscores the enduring significance of real estate in the asset portfolio of rural households, which is pivotal for grasping their credit demand dynamics.

Building on the empirical findings from Section 4, which demonstrate that income structure and asset structure have distinct effects on rural households’ consumer credit demand, we now examine the individual impacts of income diversity and asset diversity, as reflected in their Herfindahl-Hirschman Index (HHI) distributions.Given the bimodal patterns observed in both income and assets HHI distributions, we will use the median HHI values (0.754 and 0.667, respectively) to categorize the samples into two groups each. We will then conduct a Heckman two-stage analysis to compare the effects of income and asset diversity on consumer credit demand.

. Kernal Density of Income HHI and Assets HHI.

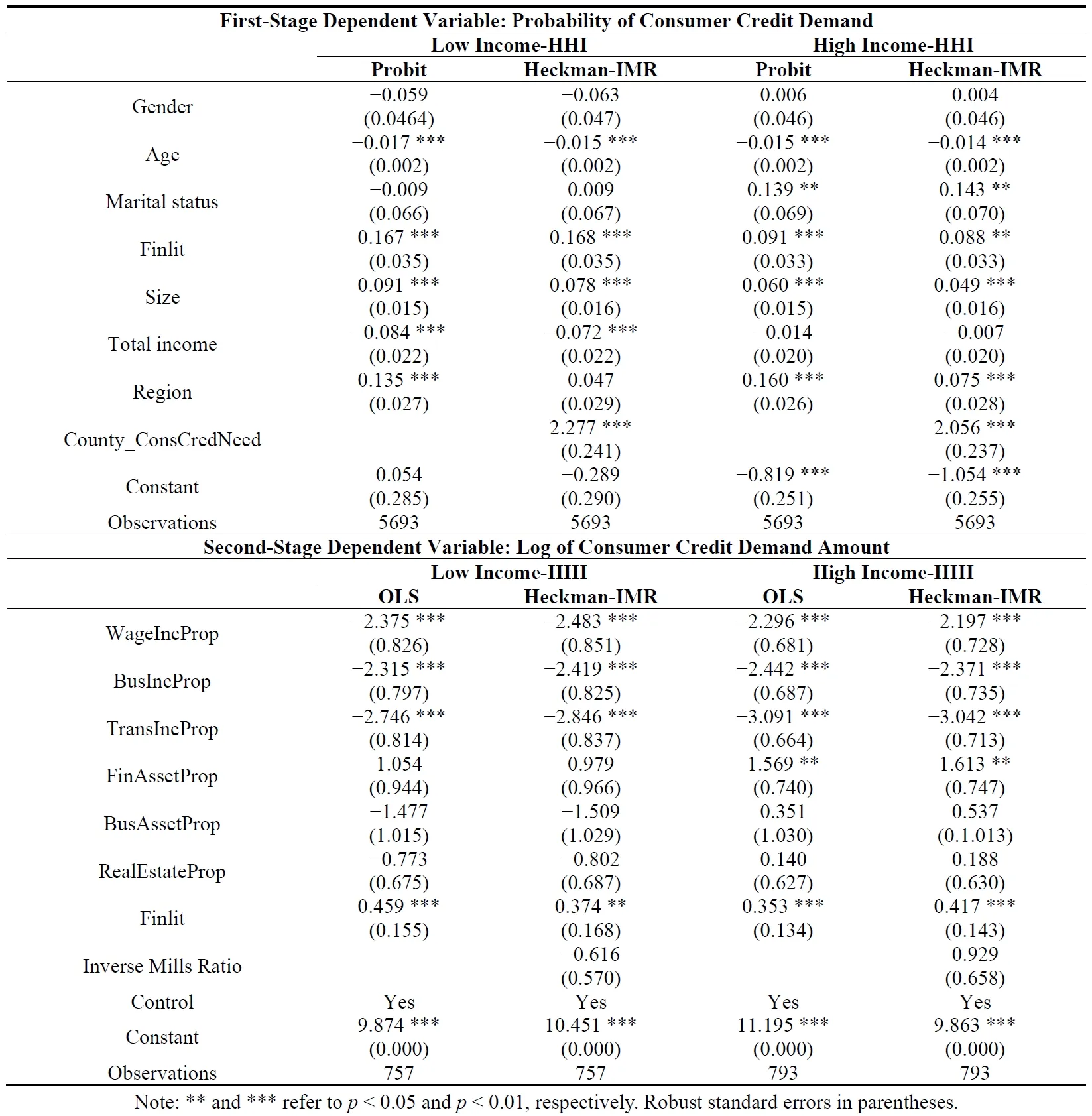

As shown in , the sample is segmented based on the median income HHI, distinguishing between a group with lower income HHI and a group with higher income HHI. This division allows for a focused examination of the impact of income diversity on consumer credit demand among rural households with varying levels of income concentration.

The first stage of the Heckman two-stage model aligns with the empirical findings from Section 4. Notably, financial literacy and the county-level consumer credit demand proportion exhibit a significant positive correlation with the likelihood of pursuing consumer credit. This suggests that both personal financial knowledge and broader market conditions within the county are crucial in shaping a household’s credit-seeking behavior. However, for the group with lower income HHI—indicating a more diversified set of income sources—the influence of financial literacy and the county-level consumer credit demand proportion is more pronounced and stronger, suggesting that these households are more sensitive to their financial knowledge and the broader credit market conditions within their county when deciding to pursue credit.

. Regression results for consumer credit demand by income HHI groups.

The second stage analysis indicates the absence of self-selection bias, with the IMR coefficients being non-significant for both groups. This suggests that the sample of households seeking credit represent the broader population across both lower and higher-income HHI groups.

In terms of the impact on the amount of credit demanded, the proportion of income components—wage, business, and transfer incomes—exerts significantly negative effects on the consumer credit demand amount for both high and low income HHI groups. This suggests that as the share of these income sources increases, households in both groups tend to demand less consumer credit, possibly because they have more stable and sufficient income streams, reducing their reliance on external borrowing. The consistency of this effect across HHI groups indicates that the need for consumer credit is inversely related to the stability and adequacy of a household’s income composition, regardless of the concentration of income sources.

For households with lower income HHI, the non-significant effect of asset components on credit demand suggests that the total asset base is not a definitive predictor of the credit amount sought once the decision to borrow is made. In contrast, among households with higher income HHI, financial assets significantly positively influence consumer credit demand. This is consistent with the notion that financial assets can act as a cushion against financial instability and as collateral, potentially increasing the credit limit households are eligible for. Meanwhile, the absence of a significant impact from other asset types, such as real estate and business assets, on credit demand indicates that although a diversified asset portfolio can enhance a household’s overall financial well-being, it does not necessarily lead to a higher demand for consumer credit.

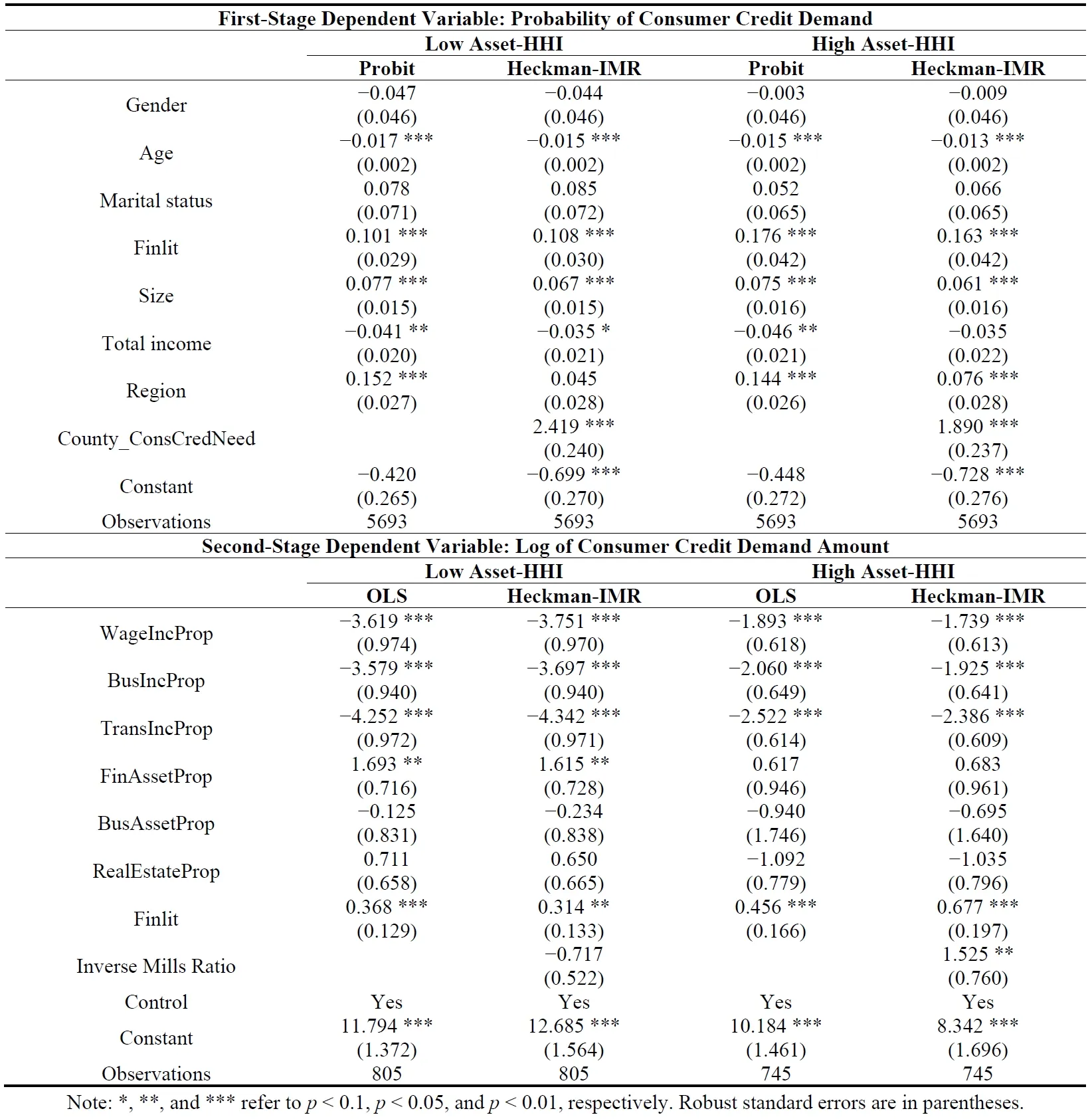

When the sample is divided based on the median assets HHI, as shown in , the analysis reveals varying patterns in the relationships we are interested in. In the first stage, financial literacy and the county-level consumer credit demand proportion both have significantly positive impacts on the decision of rural households to pursue consumer credit. However, the effect of financial literacy is more pronounced in the group with higher assets HHI, suggesting that households with more concentrated asset portfolios are more influenced by their financial knowledge when deciding to seek credit. Conversely, the proportion of county-level consumer credit demand has a more significant impact on households with a lower asset HHI. This suggests that in areas with higher overall credit demand, households with more diverse assets are more likely to seek consumer credit.

In the second stage, a significantly positive IMR coefficient for the group with a high assets HHI suggests the presence of self-selection bias. Conversely, the IMR coefficient’s insignificance for the group with a low assets HHI indicates an absence of self-selection bias. The influence of income and asset structures on consumer credit amount demanded exhibits both similarities and differences. Among the group with greater asset diversity (lower HHI), the proportion of wage, business, and transfer incomes significantly reduces consumer credit demand, with a more pronounced effect compared to the group with less asset diversity (higher HHI). This suggests that in households with more diversified assets, reliance on specific income sources plays a particularly crucial role in determining the amount of credit they seek.

Interestingly, the proportion of financial assets has a significantly positive impact on the amount of consumer credit demand only in the group with higher asset diversity. This could imply that in households with more diverse assets, financial assets are a stronger indicator of creditworthiness and borrowing capacity. For both groups, the proportions of real estate, business assets, and other assets do not significantly influence the amount of consumer credit demand. This may suggest that, while financial assets are more liquid and directly influence borrowing capacity, other asset types, though important within the overall asset portfolio, do not significantly impact credit demand decisions.Therefore, the diversity of income and asset sources within rural households introduces heterogeneity in the impact of households’ income and asset structures on their consumer credit demand amount. H2 is verified.

. Regression Results for Consumer Credit Demand by Assets HHI Groups.

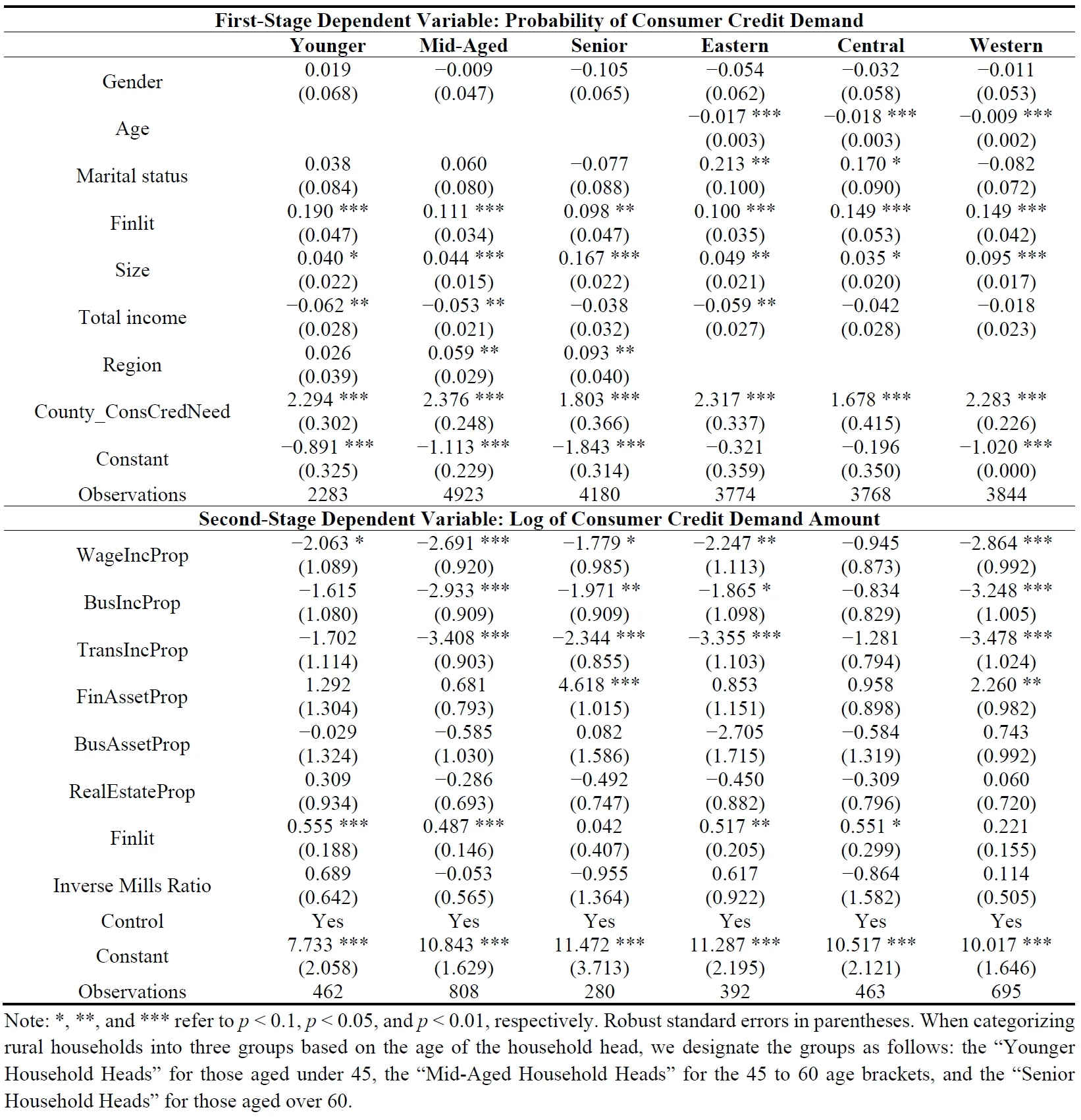

We explored the heterogeneity based on the age of the household head and the region of the household’s location. The sample was segmented into three age-based groups: individuals under 45, those between 45 and 60, and those over 60 years of age. Additionally, to account for regional disparities, the sample was categorized into three geographic regions: Eastern, Central, and Western China.

Throughout the heterogeneity analyses as shown in , it was observed that financial literacy and the county-level consumer credit demand proportion positively influenced the decision to seek consumer credit, with no evidence of sample selection bias across groups. Despite wage income, younger household heads showed no association between income or asset structure and the amount of consumer credit demanded. Both middle-aged and senior household heads saw a significant negative effect on consumer credit demand from all income components. Senior household heads were also positively affected by the proportion of financial assets.

In terms of regional disparities, in both Eastern and Western regions, all income components negatively affected the amount demanded for consumer credit. Moreover, a higher proportion of financial assets was linked to increased consumer credit demand in the Western region. Conversely, within the Central region, neither income nor asset composition significantly influences the amount of consumer credit demand.

These findings suggest that the lack of correlation between income or asset structure and consumer credit demand amount among younger household heads may reflect a higher degree of financial flexibility or alternative financial strategies that are not captured by traditional income and asset measures. For mid-aged household heads, the significant negative impact from all income components could be attributed to a more conservative approach to borrowing, possibly due to mid-life financial commitments or a preference for existing savings over additional debt. The positive influence of financial assets on credit demand among senior household heads highlights the role of liquid assets in enabling access to credit. This could be particularly important for this age group, which may have limited opportunities for income growth but still require credit for various purposes.

Regional differences in the impact of income and assets on consumer credit demand amount may be related to varying economic conditions, financial market development, and cultural attitudes towards borrowing. The reduced demand for consumer credit in Eastern households due to transfer incomes could be a result of more generous social welfare systems or a cultural preference for self-sufficiency. In contrast, the negative effect of all income components in Western households might suggest a higher reliance on income for daily expenses, leaving less room for additional borrowing. In the Central region, the lack of significant effects from income or asset structures on credit demand could indicate a more homogeneous financial situation or the presence of other factors that influence consumer credit demand, such as local cultural norms or access to financial services.

. Heterogeneity analysis results.

6. Conclusions and Discussions

The development of consumer credit in rural China has been a significant aspect of the country’s economic transformation, reflecting the growing demand for financial services among rural households. The landscape of consumer credit has evolved to include various aspects of daily life, such as housing, healthcare, education, investment, vehicle purchases, weddings and funerals, and daily consumption needs. As of the end of 2021, the narrow sense consumer credit balance had grown from 4.2 trillion yuan in 2014 to 17 trillion yuan, indicating a substantial expansion of consumer credit availability for the population, including rural residents. The demand for consumer credit among rural households is evolving. With the rise in income and asset levels, and the diversification of income and assets, rural households are expected to show different patterns of demand for consumer credit, which help integrate and allocate their income and consumption from the perspective of the family life cycle.

Therefore, our study fills the research gap and contributes to the literature by employing the Heckman two-stage approach to examine the influence of income and asset structures on the consumer credit demand amount of rural households in China. The first stage, utilizing a Probit regression model, reveals that household characteristics significantly affect the need for consumer credit, with county-level credit demand proportion serving as exclusion restriction, indicating the impact of peer credit-seeking behavior on borrowing decisions. The second stage examines the impact of income and asset structures on the amount of consumer credit demanded, highlighting the variability in the presence of self-selection bias across different samples. This approach allows us to control for potential endogeneity and provides insights into how the proportions of income components and financial assets, moving in opposite directions, significantly influence the amount of consumer credit demanded. In contrast, other asset types, such as real estate, show no significant effect. Further, the examination of income and asset diversity through the HHI indexes demonstrates varying impacts of income and asset structures on credit demand, depending on the concentration levels of income and assets. Additionally, our analysis of heterogeneity based on the age of the household head and geographic region highlights the diverse influences on the amount of consumer credit demand, underscoring the importance of tailoring financial products and policies to meet the specific needs of rural households. This comprehensive understanding can aid in fine-tuning supply-side measures and enhancing rural consumption, thereby fostering a sustainable and self-reliant economic cycle within the country.

While capable of further exploring the intricacies of rural household consumer credit behaviors, including the impact of online digital credit, our study faces limitations in its analysis. Despite the CHFS’s extensive coverage of household financial data in China, we are constrained by the lack of detailed and nuanced data required for a deeper investigation into these topics.

Nonetheless, our findings align with previous studies [

58,

59] and provide critical insights that can inform the development of consumer credit products for rural households, potentially enhancing both the quantity and quality of their consumption. It underscores the intricate link between the structure and diversity of income and assets and the demand for consumer credit. Financial institutions are encouraged to tailor their credit services to the diverse financial profiles of rural households, including flexible repayment options for those with multiple income sources.Furthermore, the study’s findings on the heterogeneity based on the age of household heads and regional disparities indicate the need for financial products that are sensitive to the economic and cultural nuances of different regions and the life stages of household heads. For instance, younger household heads may have different financial needs and aspirations compared to their older counterparts, requiring a more nuanced approach to consumer credit product design. Similarly, regional differences in economic development, cultural practices, and access to financial services should be considered when developing credit products to ensure they are accessible and relevant to the local population. In addition to this, there is a need for financial education programs that can empower rural households to make informed credit decisions. These programs should be tailored to address the unique needs and challenges of rural consumers, including clear guidance on understanding interest rates, loan terms, and the importance of building a credit history.This tailored approach is essential for stimulating economic growth and unleashing the consumption potential in rural areas, thereby contributing to the overarching goal of rural revitalization.

Acknowledgments

This work was supported by the Fundamental Research Funds for the Central Universities, Zhongnan University of Economics and Law (2722024BQ045).

Author Contributions

Conceptualization, R.C. and Y.L.; methodology, H.S.; formal analysis, R.C.; investigation, Y.L.; writing—original draft preparation, Y.L., H.S. and R.C.; writing—review and editing, H.S., R.C. and Y.L.; supervision, H.S.; funding acquisition, H.S. All authors have read and agreed to the published version of the manuscript.

Ethics Statement

Not applicable.

Informed Consent Statement

Not applicable.

Funding

This project was funded by the Fundamental Research Funds for the Central Universities, Zhongnan University of Economics and Law (2722024BQ045).

Declaration of Competing Interest

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

References

-

1.

Zhang L, Ren S. Promoting the healthy development of consumer finance to unleash consumption potential.

Manag. World 2022,

38, 107–116+130.

[Google Scholar]

-

2.

Fu Q, Huang Y. The heterogeneous impact of digital finance on rural financial demand: Evidence from the China Household Finance Survey and Peking University’s Digital Inclusive Finance Index.

Financ. Res. 2018,

11, 68–84.

[Google Scholar]

-

3.

Tian H, Wang A, Zhu Z. Digital empowerment: The impact of internet usage on rural household credit and its heterogeneity—An examination and analysis based on the choice experiment method.

Agric. Technol. Econ. 2022,

4, 82–102.

[Google Scholar]

-

4.

Wang J, Xiao Q, Li J. Financing of new types of agricultural business entities: Dilemmas, causes, and strategies—Based on a survey of 131 comprehensive agricultural development industrialization development loan interest subsidy projects.

Agric. Econ. Issues 2018,

2, 71–77.

[Google Scholar]

-

5.

Ma J, Li Z. Does digital financial inclusion affect agricultural eco-efficiency?

A case study on China. Agronomy 2021,

11, 1949.

[Google Scholar]

-

6.

Wang X, Zhao Y. The development of digital finance and the disparity in financial accessibility between urban and rural households.

China Rural Econ. 2022,

1, 44–60.

[Google Scholar]

-

7.

Li W, Chen R, Zhang H. Enhancing stability and achieving high-quality development in rural credit cooperatives through inclusive finance: Evidence from Shaanxi Province, China.

Appl. Econ. 2024,

56, 5412–5427.

[Google Scholar]

-

8.

Yao J, Zang X, Zhou B. Heterogeneity in the marginal propensity to consume of Chinese residents and the release of consumption potential: An analysis from the perspective of household credit and asset allocation.

Econ. Perspect. 2022,

8, 45–60.

[Google Scholar]

-

9.

Chen X, Mi Y, Yang T, Shi X. The inverted “U” relationship between farmers’ income and credit quantity: Its theoretical interpretation.

Agric. Technol. Econ. 2021,

6, 4–17.

[Google Scholar]

-

10.

Sun T. Examining the supply-side structural reform of inclusive finance in rural areas through the balance sheet of rural households.

China Rural Econ. 2017,

5, 31–44.

[Google Scholar]

-

11.

Jack W, Kremer M, De Laat J, Suri T. Credit access, selection, and incentives in a market for asset-collateralized loans: Evidence from Kenya.

Rev. Econ. Stud. 2023,

90, 3153–3185.

[Google Scholar]

-

12.

Zhang X, Dong J. An empirical analysis of farmers’ borrowing behavior and potential demand: Based on 762 survey questionnaires from farmers in Shandong Province.

Agric. Econ. Probl. 2017,

38, 57–64+111.

[Google Scholar]

-

13.

Yin Z, Luo C, Wang Y. The efficiency of monetary policy interest rate transmission in China under the digitalization background: Micro-evidence from the digital consumer credit market.

Manag. World 2023,

39, 33–48+99.

[Google Scholar]

-

14.

Wang X, Zhang J. An empirical measurement of the contribution of gender differences to the profitability of consumer credit in China: Evidence from commercial bank credit card business.

Chin. Manag. Sci. 2022,

30, 221–230.

[Google Scholar]

-

15.

Hu S, Guo Y, Yang T. Information asymmetry, financial integration, and credit fund allocation: An empirical study based on farmer survey data.

Agric. Technol. Econ. 2016,

2, 81–91.

[Google Scholar]

-

16.

Yu G. Rural credit investment, labor force transfer, and urban-rural income disparity: Theory and empirical evidence.

Agric. Technol. Econ. 2021,

11, 78–92.

[Google Scholar]

-

17.

Ke M, Jiang S, Zhang L. Analysis of the influencing mechanism of early repayment behavior in farmer loans.

Agric. Technol. Econ. 2021,

10, 53–63.

[Google Scholar]

-

18.

Peón D, Guntín X. Bank credit and trade credit after the financial crisis: Evidence from rural Galicia.

J. Bus. Econ. Manag. 2021,

22, 616–635.

[Google Scholar]

-

19.

Qiu Z, Luo Y, Jiang Y, Wu C. Will financial technology subvert traditional finance? An economic interpretation of big data credit.

Int. Financ. Stud. 2020,

8, 35–45.

[Google Scholar]

-

20.

Wang H, Kong R. Has formal lending promoted rural household consumption? An empirical analysis based on the PSM method.

China Rural Econ. 2019,

8, 72–90.

[Google Scholar]

-

21.

Wu L, Xu Z. The poverty reduction and income increase effects of inclusive finance in rural China: A regression discontinuity analysis based on microdata of 4023 households.

South. Econ. 2018,

5, 104–127.

[Google Scholar]

-

22.

Wu W, Wu K, Wang J. Financial literacy and household debt: An analysis based on micro-survey data of Chinese residents’ households.

Econ. Res. J. 2018,

53, 97–109.

[Google Scholar]

-

23.

Yin Z, Zhang H. Financial accessibility, internet finance, and household credit constraints: An empirical study based on CHFS data.

Financ. Res. 2018,

11, 188–206.

[Google Scholar]

-

24.

Dobridge C. High-cost credit and consumption smoothing.

J. Money Credit Bank. 2018,

50, 407–433.

[Google Scholar]

-

25.

Ma J, Qi H, Wu B. The impact of rural financial institution marketization on financial support for agriculture: Suppression or promotion? Evidence from the reform of rural credit cooperatives into rural commercial banks.

China Rural Econ. 2020,

11, 79–96.

[Google Scholar]

-

26.

Wu Y, Song Q, Yin Z. Analysis of farmers’ formal credit access and credit channel preferences: An explanation from the perspective of financial knowledge and education level.

China Rural Econ. 2016,

5, 43–55.

[Google Scholar]

-

27.

Chen F. Social capital, financing psychology, and farmers’ borrowing behavior: A logical analysis and empirical test from the perspective of behavioral economics.

South Financ. 2018,

4, 51–63.

[Google Scholar]

-

28.

Cheng Z, Huang N. How does digital finance affect the savings rate of Chinese residents? An analysis based on the dual-channel mental accounting theory.

Econ. Perspect. 2024,

1, 93–110.

[Google Scholar]

-

29.

Xie J, Tu X, Ye S. Financial lending, psychological wealth, and farmers’ consumption.

Financ. Econ. Res. 2017,

32, 85–94+126.

[Google Scholar]

-

30.

Lu X, Wu Y. Inflow of land, farmers’ demand for agricultural credit, and credit constraints: An analysis based on data from the China Household Finance Survey (CHFS).

Financ. Res. 2021,

5, 40–58.

[Google Scholar]

-

31.

Xu Y, Zhang Y, Shi S. Liquidity constraints, income inequality, and farmers’ consumption.

Reform 2023,

3, 133–147.

[Google Scholar]

-

32.

Yang J, Zou J. Consumer smoothing and the heterogeneity of consumption structure: An analysis based on the life-cycle model.

Econ. Res. J. 2020,

55, 121–137.

[Google Scholar]

-

33.

He Z, Song X. How does the development of digital finance affect residents’ consumption?

Financ. Trade Econ. 2020,

41, 65–79.

[Google Scholar]

-

34.

Tan Y, Zhang Z. Social networks, informal finance, and multi-dimensional poverty of rural households.

Financ. Res. 2017,

43, 43–56.

[Google Scholar]

-

35.

Lin L, Wang W, Gan C, Cohen D, Nguyen Q. Rural credit constraint and informal rural credit accessibility in China.

Sustainability 2019,

11, 1935.

[Google Scholar]

-

36.

Sun H, Hartarska V, Zhang L, Nadolnyak D. The influence of social capital on farm household’s borrowing behavior in Rural China.

Sustainability 2018,

10, 4361.

[Google Scholar]

-

37.

Hu L, Shu W, Zhou Y. The effectiveness and future direction of property rights reform in promoting the development of new rural collective economy.

Agric. Econ. Probl. 2024,

2, 87–97.

[Google Scholar]

-

38.

Chen X. Fully leveraging the role of rural collective economic organizations in common prosperity.

Agric. Econ. Probl. 2022,

5, 4–9.

[Google Scholar]

-

39.

Du X. Current income and income distribution of rural residents in China—Also on the income levels and disparities among rural residents in various grain function zones.

China Rural Econ. 2021,

7, 84–99.

[Google Scholar]

-

40.

Zhu Q, Zhu C, Peng C, Bai J. Can informatization promote income growth for farmers and reduce income disparities?

Econ. J. 2022,

22, 237–256.

[Google Scholar]

-

41.

Chen Y, Fan Y. An empirical analysis of the dynamic poverty reduction effects of rural financial development.

Stat. Decis. 2021,

37, 162–165.

[Google Scholar]

-

42.

Jain M, Kostyshyna O, Zhang X. How do people view wage and price inflation?

J. Monet. Econ. 2024,

145, 103552.

[Google Scholar]

-

43.

Dettling L, Hsu J. Minimum wages and consumer credit: Effects on access and borrowing.

Rev. Financ. Stud. 2021,

34, 2549–2579.

[Google Scholar]

-

44.

Yang Z, Wen F. From working to entrepreneurship—The upgrade of rural labor transfer forms with farmland transfer.

Manag. World 2020,

36, 171–185.

[Google Scholar]

-

45.

Li H, Zhang X, Li H. Has farmer welfare improved after rural residential land circulation?

J. Rural Stud. 2022,

93, 479–486.

[Google Scholar]

-

46.

Lu Y, Zhang J. Factors influencing the financial asset selection behavior of rural households: An analysis based on CHFS microdata.

Manag. World 2018,

34, 98–106.

[Google Scholar]

-

47.

Zhang X, Dong W, Han K. The impact of inclusive finance on household financial asset selection and mechanism analysis.

Contemp. Financ. Econ. 2020,

1, 65–76.

[Google Scholar]

-

48.

Wang X. Social networks, private lending, and rural household financial asset selection: An empirical analysis based on data from the China Household Finance Survey.

Financ. Trade Res. 2017,

28, 47–54.

[Google Scholar]

-

49.

Zhao H, Wu D. A Comparative Study of Two Income Decomposition Methods under the Permanent Income Hypothesis.

Quant. Tech. Econ. 2019,

36, 38–58.

[Google Scholar]

-

50.

Zhang Y, Lu Y. The Impact of Payment Digitization on Household Consumption—Also Discussing Digitalization of Payment and Household Debt.

Stud. Int. Financ. 2024,

10, 15–25.

[Google Scholar]

-

51.

Wang H, Qin G, Wang B, Zhu Y. Social capital, financial lending, and multi-dimensional poverty of rural households: Based on micro-survey data from three provinces in the Qinba mountain area.

China Popul. Resour. Environ. 2019,

29, 167–176.

[Google Scholar]

-

52.

Lennox C, Francis J, Wang Z. Selection models in accounting research.

Account. Rev. 2012,

87, 589–616.

[Google Scholar]

-

53.

Wen T, Zhu J, Wang X. The “elite capture” mechanism of agricultural loans in China: A stratified comparison between poor and non-poor counties.

Econ. Res. J. 2016,

51, 111–125.

[Google Scholar]

-

54.

Dong X, Dai Y, Zhu C. The impact of financial literacy on household borrowing decisions: An empirical analysis based on CHFS2013.

J. Southeast Uni. 2019,

21, 44–52, 146–147.

[Google Scholar]

-

55.

Wu Y, Li C, Li X, Yi D. The impact of digital finance development on the traditional private lending market and its mechanisms.

Manag. World 2020,

36, 53–64+138+65.

[Google Scholar]

-

56.

Liu S, Liu M. Household borrowing, operational scale, and farmers’ land management preferences: A perspective from the differentiation of small, medium, and large farmers.

Resour. Environ. Yangtze River Basin 2021,

30, 1969–1981.

[Google Scholar]

-

57.

Guo X, Liu H, Wu Z. Income inequality and household borrowing behavior: Does the motive for households to borrow for the pursuit of social status really exist?

Econ. Theory Bus. Manag. 2016,

5, 84–99.

[Google Scholar]

-

58.

Xie J, Wu J. Digital finance, credit constraints, and household consumption.

J. Central South Uni. 2020,

26, 9–20.

[Google Scholar]

-

59.

Li J, Li H. How does consumer credit affect household consumption?

Econ. Rev. 2017,

2, 113–126.

[Google Scholar]