1. Introduction

Rural locations, historically centered around farming and resource-dependent activities, have witnessed substantial economic transformations in recent decades, especially in industrialized countries [

1]. The ongoing pressure for transformation becomes particularly pronounced in rural economies where core industries heavily rely on natural resources, given the escalating scarcity and increased social value associated with these resources [

2]. This is especially evident in regions where agricultural value chains remain of crucial importance.

The necessity for adaptation to these pressures often implies a demand for radical change or transformation. While a transition denotes a significant shift in established patterns that leaves fundamental actors and processes changed but largely intact [

3], transformation entails the establishment of entirely new businesses and processes. The transformation of a business often necessitates a concurrent transformation of its environment, involving “new relationships, policies, innovations, and institutional arrangements” [

3] (p 350). Successful reorientation demands the utilization of specific resources and dynamic capabilities of companies, as well as coordination among firms and other organizations within their business environment [

4] because “development pathways consist of cumulative actions of individuals and stakeholder groups” [

5] (p 125).

However, industries heavily reliant on resource exploitation and scale effects might be caught in path dependencies [

5], “resource lock-in” and “truncated technological developments” [

3,

6]. In other cases, diversified ecosystems of industries and businesses surrounding resource-dependent industries may harbor the potential for active transformation.

Against this background, this paper asks what strategies industries and businesses pursue that successfully exploit the transformative potential of a resource dependent location and what prevents other industries and businesses there from doing the same. We ask, in other words, from an actor-centered perspective, which industries and stakeholders possess the willingness, resources, and capabilities to transform their businesses and regional business fields to stabilize the local growth regime under severe disruptions. While analyses of such processes often focus either on selected industries from a corporate perspective [

7] or on entire business fields or value chains from an overarching institutional perspective [

8], our approach combines the enterprise perspective with a meso-level field approach in an actor-centered framing.

We apply this perspective to a German hog production region facing transformative pressures due to global competition, social and ecological burdens, and shifting consumer demands. Vilas-Boas et al. [

9] have conceptualized the “Brazilian pig production system” as a socio-technical system where so-called boundary elements “enable individuals and organizations with different mandates and interests to work beyond and cross boundaries”. We understand the spatially concentrated meat and livestock business field in our actor-centered research as an outwardly open and changeable dynamic field, subject to strong transformation pressures and conceptualize it as actor-oriented SAF [

10]. In this SAF, stakeholders from the business sector and the public sector with different resource endowments and capabilities try to transform or stabilize the field [

11]. Within this framework, we analyze at hand interviews with experts and stakeholders from the region and its meat value chain, whether and how the regional meat value chain can remain viable if the livestock and meat sector declines. We find that even if the powerful representatives of the “old” core and their networks do not prevent transformation, the region may no longer be home to the primary industries of the transformed field in the future. But then, too, challengers from former support activities who use their valuable resources to steer away from cost competition towards new markets could provide the regional field with future-proof capacities and capabilities.

The paper begins with an outline of the conceptual basis of our analysis in chapter two, followed by the material and methods chapter, which describes the case of the regionally concentrated meat value chain as well as the development of interview guidelines and the conduct of the interviews. The structure and genesis of the field, actors and strategies working towards stabilization, and possible development paths in the event of destabilization are then discussed in the results chapter on the basis of the interview data. The discussion chapter interprets the observations in light of the conceptual framework, preceding a final chapter of conclusions.

2. Theory and Conceptual Framework

In approaching our research question, we adopt an actor-centered perspective while maintaining awareness of the institutional context. Our conceptual framework thus synthesizes the resource-based perspective [

12] and the dynamic capability concept [

13] at the micro-level with the sociologically based meso-level concept of Strategic Action Fields (SAFs; [

11,

14]). We view SAFs as an application-oriented concept that amalgamates insights into the interaction of stakeholders in value chains and business networks for the analysis of transformation processes.

According to the resource-based perspective, the sustainable competitiveness of enterprises and locations can be attributed to their mastery of enterprise- or location-specific resources, deemed valuable, rare, imperfectly imitable, and non-substitutable [

12]. These resources can be broadly applicable or industry-specific, originating either at the outset or evolving during the production process [

15]. Resource-dependent industries often derive benefits from locally available natural resources. Firms leverage their unique resource bundles as the foundation for developing new strategies and securing lasting competitive advantages [

4]. To maintain specific competitiveness, transforming businesses seek to capitalize on their distinct resources within new processes and activities. The location specificity of these resources influences whether a company remains at its location during transformation [

15]. Therefore, analyzing the unique resources of a location and its firms is crucial in order to understand and master transformation processes [

4].

Sustaining competitiveness in changing and turbulent environments requires dynamic capabilities [

4]. Dynamic capabilities represent internal organizational patterns facilitating knowledge integration, coordination, learning processes, and adaptation to evolving contextual factors, all in pursuit of enduring business goals [

13]. Essential dynamic capabilities include the ability to sense opportunities, acquire and integrate necessary resources and skills, and coordinate and cooperate with other businesses and institutions [

16]. This mobilization of external resources in order to support the improvement of activities, processes, technologies, and products and services is discussed under the concept of open innovation [

17,

18], which involves the integration of external impulses from customers, suppliers, universities, and other stakeholders in a field. Intense collaborations across multiple industries in developing new products, services, or business models are termed cross-industry innovation or cooperative innovation [

19].

The overall structure of network relationships with competitors, suppliers, customers, service providers, and institutional organizations has been found to be among the many determinants of the innovative capacity of enterprises [

20]. Even if businesses possess valuable resources and the necessary dynamic capabilities, successful transformation may be impeded without sufficient support in their environment. Value chains are an important part of the institutional environment of companies, but the conventional view of linear value chains oversimplifies their complexity and the diverse activities at each stage. The Global Value Chains (GVCs) approach has highlighted the coordination or governance of value chains and their dependence on structure [

21]. However, the GVC approach emphasizes the continuous development of value chains via upgrading processes, products, functions, and chains [

22] rather than fundamental disturbances and subsequent radical transformations.

Drawing from network-related theories allows for a more dynamic perspective on value chains within their business environment. The significance of networks of people and organizations for the competitiveness of value chains or locations has long been recognized and described in various ways. Marshall’s concept of “industrial atmosphere” portrays regionally concentrated production networks that confer locational advantages to firms within these structures [

23]. This fosters knowledge circulation or “local buzz” [

24,

25] and facilitates “communities of practice,” informal links between members with shared expertise [

26]. Spatial proximity also gives rise to specialized institutions that promote stable network relationships and knowledge flows [

26,

27,

28,

29]. However, downsides of tight networks and narrow institutions have also been identified, such as certain stakeholder groups controlling “political pathways” and retaining power for extended periods [

5].

Granovetter [

30] introduced the distinction between weak, bridging, and strong ties to account for the ambiguous character of networks. Strong and rigid network relationships, or if local production networks rely heavily on intra-regional interactions alone, pose a risk of lock-in into unfavorable technological paths [

20,

31]. Tight networks and strong (mutual) dependencies often impede the timely transformation of processes and technologies, even though exogenous shocks are seen as opportunities for dissolving such path dependencies [

31].

The SAF concept by Fligstein [

14] integrates various aspects of management and network theory as well as political (process) theory [

32] to better incorporate agency, power and strategy into the analysis of technological transformations from a macro- and meso-level perspective [

10]. SAFs can be viewed as parts of larger socio-technological systems, providing a meso-level perspective on transformation processes in institutionally complex, multi-level environments. Examples of SAFs include value chains, social movements, or government systems. Mooney [

33] discusses the potential transformation of the food system through food policy councils within the SAF framework. The actors involved in SAFs encompass not only incumbents and challengers but also governance units responsible for overseeing compliance with field rules and facilitating the smooth functioning of the system, such as trade associations. These field-internal governance units differ from external state structures operating on another level and holding jurisdiction over the SAF [

11].

External shocks, changes in dependent fields, and macro-level events like cultural, economic, or legal changes in the larger socio-technical system can destabilize SAFs. During transformation processes, incumbents may lose their advantages to new and smaller but flexible challengers [

11]. Incumbents might attempt to prevent transformation, and interconnected dependencies may impede alternative production systems, resulting in lock-ins. Typically, incumbents hold more influence, while challengers occupy less privileged positions. Incumbents can thus act as crucial agents of change, and the stability of SAFs depends on the strategic actions of individual actors. Political regulation and collaboration among powerful actors can coordinate transformation processes.

3. Materials and Methods

We analyze the perspectives and strategies of stakeholders within an established value chain in an old industry that is under strong transformative pressure. The case we analyze is livestock and meat value chains in a livestock-intensive region in north-western Germany that need to adapt to new societal demands and market conditions. We use data from interviews with different actors from the networks involved in livestock and meat production to gain insights into their perspectives on constraints and opportunities for future development.

3.1. The Case: Location and Value Chains

In Germany, a concentrated food industry has historically positively influenced the economic growth of rural locations [

34,

35]. Among the spatially concentrated branches, the meat industry stands out as a low-technology sector under intense price pressure with relatively low wages [

36]. Its competitiveness in high-wage countries like Germany is, in part, sustained by tariff and non-tariff protective measures [

37,

38]. Over the past decade, livestock density has decreased in most of Germany but increased in a North-West region specializing in the sector [

39]. The spatial proximity of livestock and slaughterhouses, driven by economies of scale and technological advancements, fuels concentration dynamics [

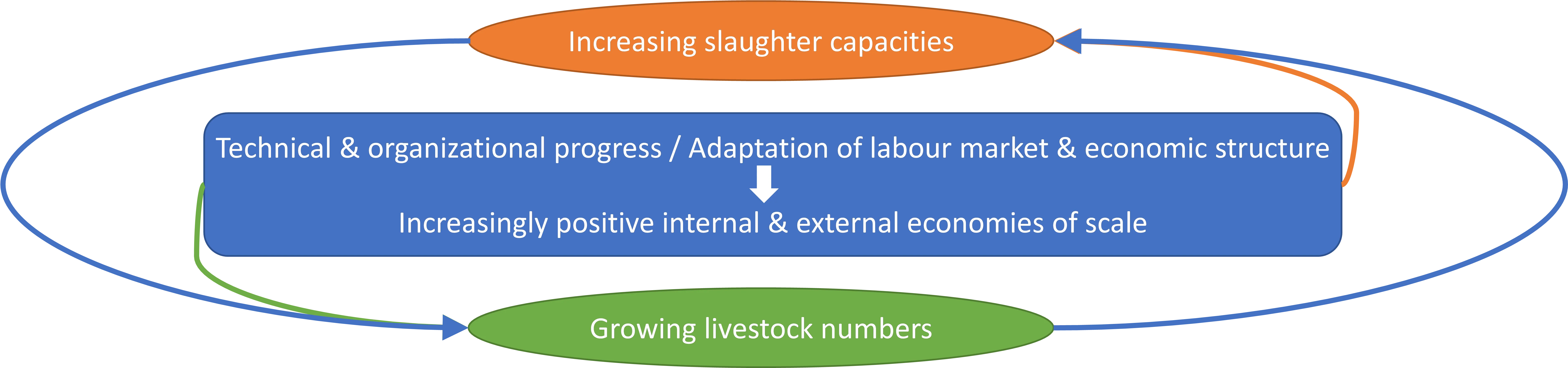

40] (). Growing local availability of specialized services, for example, from veterinarians, and increasingly specialized labor markets additionally generate positive externalities of concentrated production [

41]. The region, spanning contiguous districts in the border region of Lower Saxony and North Rhine-Westphalia, hosts a highly concentrated pig and poultry production sector, employing about 8% of the labor force in 2019, compared to just under four per cent in comparable other non-urban districts in western Germany.

. The positive mutual reinforcement in growth between livestock-production and slaughter capacities.

This concentration raises significant social challenges related to animal welfare, working conditions, and environmental protection [

42]. Nitrogen and phosphorus contamination, societal criticism of animal husbandry practices, and recent scrutiny of the meat-processing industry underscore the need for regulatory measures [

43,

44]. According to various specialists, shrinking the number of livestock and additional regulations will be inevitable to maintain standards and safeguard the environment’s soil, air, and water quality [

45,

46,

47,

48]. Implementing such measures, coupled with potential decreases in domestic meat consumption, may impact farms significantly, making them uneconomical and accelerating structural shifts [

49]. The reduction of animal farming can then have cascading effects on the entire value chain, affecting other economic sectors within and beyond the livestock and meat production domain.

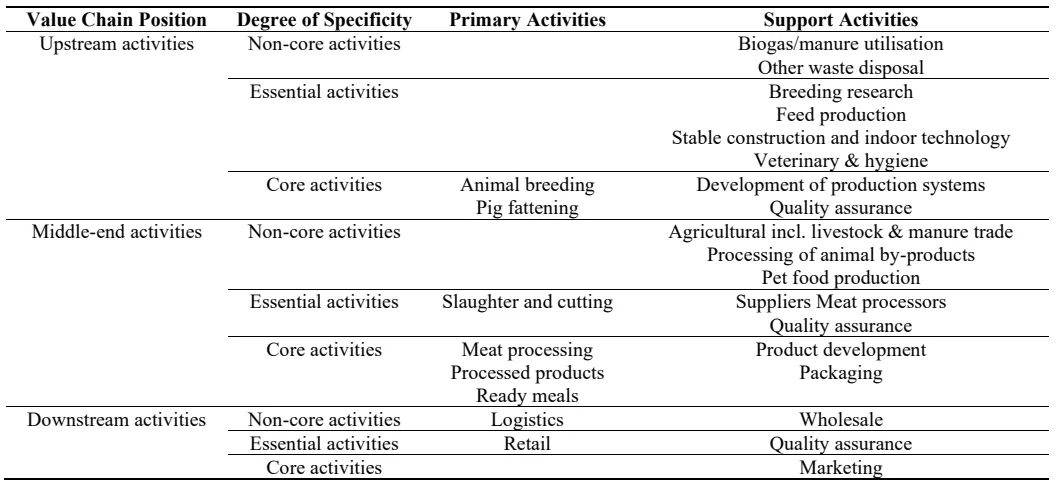

To reflect the complexity of the livestock and meat value chain, depicts it based on a compilation of classification approaches for value chain activities [

50]. Accordingly, at each location of the value chain(s), i.e., upstream, middle, and downstream, one can differentiate non-core, essential, and core as well as primary and support activities. Even non-core support activities like processing of animal by-products might well be important for the competitiveness of the production system, and could become crucial for value chain transformation.

. The livestock and meat value chain according to combined classification approaches for value chain activities.

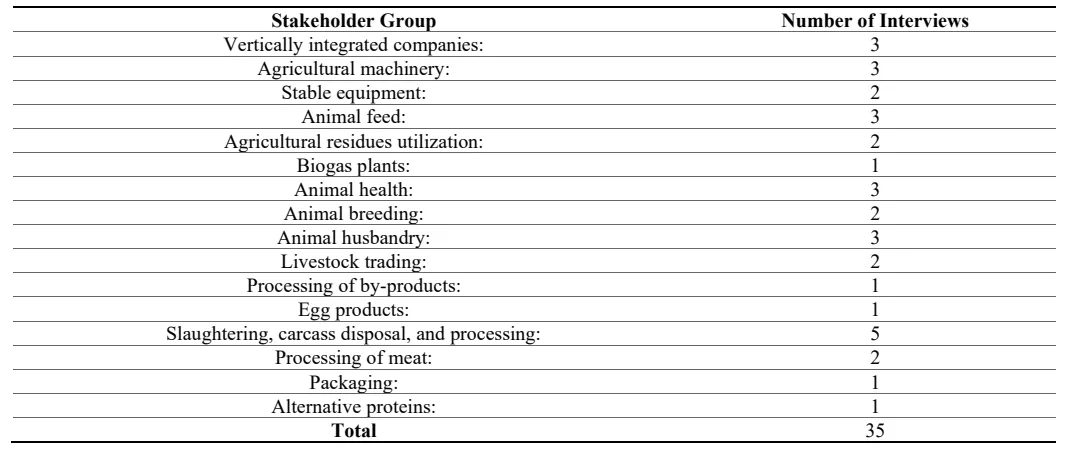

Between January and August 2021, we conducted 21 interviews with local experts for the region and its economy and the livestock and meat value chain, and 35 interviews with stakeholders, i.e., with owners and managers of businesses from the various production stages and industries in the field (). Interviewees were selected in a snowball system. Therein, interviewees were asked which other personalities and organizations they considered to be particularly knowledgeable or influential in the regional field.

Stakeholder selection concentrated on important industries and companies in the livestock value chain that had been identified through internet research and an analysis of the Creditreform database

1. Selected were representatives of businesses that had been recognized as specifically influential either as incumbents or as challengers of the field. Experts are individuals possessing factual and experiential knowledge within the research domain, capable of providing valuable insights into contextual conditions that may affect actor actions [

51]. For the interviews, experts were selected for their relevance to and knowledge of regional development and livestock farming, ensuring diverse viewpoints. The interviewed experts came from various organizations and institutions, including politics, public administration, professional networks, trade chambers, and research institutions. The interviews with experts and stakeholders lasted, on average, for 82 min.

. Interviewees from the livestock and meat value chain by industries.

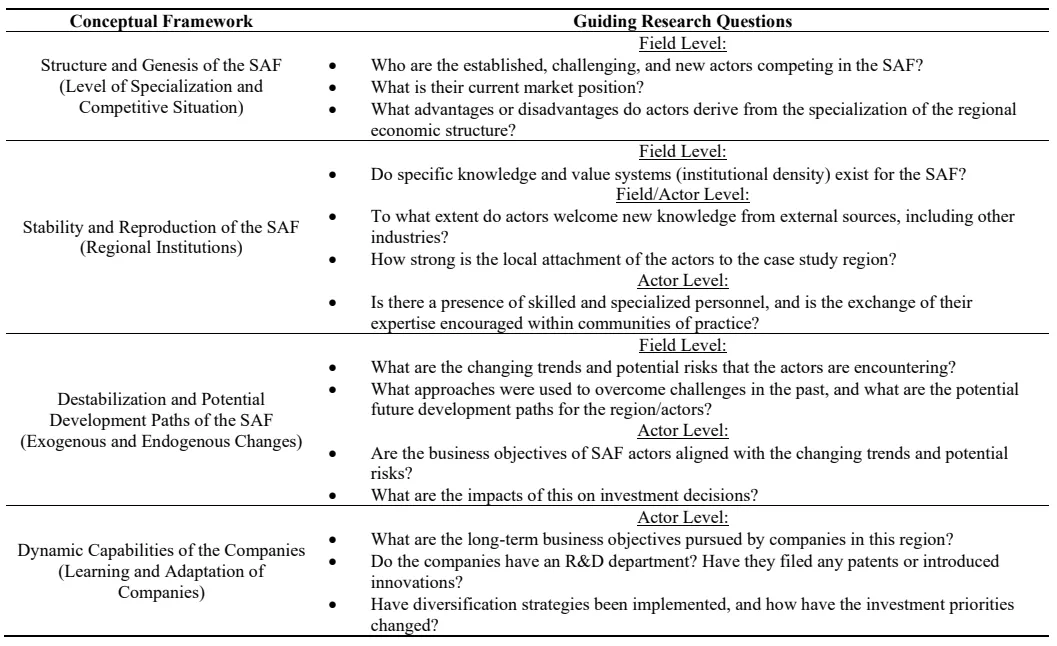

The interviews aimed to gain insight into the structure, dynamics, and transformation capacity of the SAF. The interviews followed a deductively developed conceptual framework based on the theories outlined in Chapter 2. depicts this framework that directed the interview structure and provided the basis for formulating guiding research questions. If required, a differentiation was drawn between questions targeted at the field level and those that were directed toward the actor level.

To turn these guiding research questions into efficient interview prompts, open-ended questions were developed that were aligned with the observation areas and indicators. These prompts were tailored for both experts and company stakeholders to investigate diversification strategies, expectations regarding SAF stabilization or transformation, and other relevant topics. Experts were asked questions such as, “From your viewpoint, what predominant development trends or corporate strategies can you identify in the sector?” and “Which trends or strategies do you believe are especially promising for the future?” They were also asked about shifts in the corporate landscape and investment focus.

Stakeholders were presented with questions such as, “To what extent and in what areas does your company/farm invest in opportunities beyond its core business?” and “Could you describe the nature of information exchange between your company/farm and others?” In addition, stakeholders were asked to envision their company’s/farm’s outlook ten years from now and highlight expected differences from the present. These and other open-ended questions aim, among other things, to uncover insights about diversification strategies pursued by companies and their perceptions regarding SAF stability or transformation.

Qualitative content analysis principles, as proposed by Mayring [

52] and Mayring and Fenzl [

53], were used to analyze the interview data. This process involved assigning relevant content to codes that represent the overarching base categories. The coding process aimed to condense the data while preserving informative insights. The text segments that were coded were compared and interpreted based on the theoretical aspects represented by the codes.

. Guiding research questions for the interviews in the context of the conceptual framework.

4. Results

This chapter presents the findings derived from expert interviews and stakeholder responses. The initial section explores the “General Characteristics of the SAF” and sheds light on the competitive landscape as perceived by experts in the region. Following this, the section titled “Stability and Reproduction” delves into the normal functioning of the SAF, highlighting how companies utilize their resources to enhance competitiveness. The subsequent section, “Destabilization and Potential Development Paths”, outlines the dynamic capabilities and strategies articulated by interviewees to navigate anticipated rapid changes.

4.1. General Characteristics of the SAF According to Local Experts

Local experts identify the region as a vital catalyst for employment growth, value creation, and innovation, often likening it to the “Silicon Valley” of modern agricultural production. The concentration of companies is seen as instrumental in fostering efficient value chains, collective knowledge, and collaboration within formal and informal networks. Noteworthy aspects highlighted by experts include the prevalence of SMEs, the existence of “Hidden Champions”—successful market leaders with a national and international presence—and the establishment of start-ups engaged in alternative protein production. These start-ups, frequently originating from the Netherlands, the USA, and Israel, often emerge from university environments, particularly in fields like computer science, artificial intelligence, food/biotechnology, and engineering.

This narrative portrays the SAF as an open, dynamic, connected, and innovative cluster, suggesting the presence of valuable network resources and dynamic capabilities crucial for maintaining competitiveness, even amidst a potential shift away from livestock farming. Acknowledging the need for transformation, experts point to negative external effects such as concerns about animal welfare, human health, and environmental impact. The competition for usable land has led to increased land prices, and attracting skilled workers has become challenging, especially in the agricultural and food sectors.

4.2. Stability and Reproduction of the SAF

Experts and stakeholders affirm that regional agribusiness has enjoyed a prolonged period of relatively stable growth in recent years, with few external shocks posing serious threats. Stakeholders reflect on 15 years of continuous growth, attributing the resilience of family-owned businesses to factors such as high equity ratios and reinvestment of primary funds. However, some experts note a lack of a start-up culture and venture capital, which could impede certain innovation efforts.

Innovation projects are often supported by public research funding, with the Federal Government’s innovation program earning praise. The “Seedhouse” start-up accelerator in Osnabrück and the “innovate!convention” in Lower Saxony are recognized as significant platforms for connecting companies with start-ups. While research collaborations are highlighted as key for innovation, stakeholders note the complexity of state funding as a hurdle for risk-taking research. Stakeholders call for more dedication from scientists and policymakers, emphasizing the need for practical project support alongside fundamental research funding.

Many stakeholders referred to research collaborations as a primary avenue for innovation. These collaborations were made possible through partnerships with research institutions and joint projects. According to interviewees, state support provided via the “Bundesanstalt für Landwirtschaft und Ernährung” (BLE)

2 and collaboration with universities offer direct benefits to companies. Regional, national, and international partners contribute to research collaborations in the SAF. Universities from different cities are among the key collaborators. According to experts, practice-oriented local academic institutions like the Competence Center of Applied Agricultural Engineering (COALA) at the Osnabrück University of Applied Sciences (HS OS), the German Institute of Food Technologies (DIL), and the Private University of Applied Sciences (PHWT) facilitate industry-academia cooperation.

According to experts, universities such as the University of Osnabrück (UOS) and HS OS are also successful in attracting and training young talent. Enterprises from the field interlink with universities and use traditional recruitment methods and platforms such as StepStone in order to recruit skilled labor. Stakeholders suggest that a reliable commitment in and for the region helps to maintain a stable workforce. Employee retention is realized by firms that care for employee satisfaction. Strategies include involving employees in decision-making and offering career prospects, flexible working, and remote working. In-house training and early contact with candidates are common.

Stakeholders stress the importance of political and administrative connections for knowledge exchange, with interest groups playing a vital role in influencing policymakers. Interest groups, such as the “Agrar- und Ernährungsforum Oldenburger Münsterland e. V”. (AEF)

3 play a vital role in influencing policymakers. Local political support is particularly emphasized, although opinions on the effectiveness of political influence vary.

One expert observes a rise in “chain thinking” among stakeholders, symbolizing their willingness to support initiatives like the “Initiative Tierwohl” (ITW)

4 aimed at promoting animal welfare in livestock farming or the “Niedersächsischer Weg” (Lower Saxony Path)

5, both involving business, politics, administration, and civil society. Formal and informal networks are interconnected with each other. Informal communication between stakeholders is considered crucial, often facilitated through events such as “Niedersachsen Abend” (Lower Saxony Evening)

6 or informal discussions. Trust arising from informal connections is seen as reducing transaction costs and accelerating decision-making processes. However, stakeholders acknowledge that informal exchange depends on individuals, and too much of it may lead to collaboration fatigue or resistance to change.

4.3. Destabilization of the SAF and Adaptive and Transformative Stakeholder Strategies

Despite its current stability, experts and stakeholders concur that the field faces increasing economic transformation pressures. Challenges include heightened competition, societal demands for sustainability and animal welfare, and potential disruptions from innovations in alternative proteins. While some experts believe existing technological solutions can address societal demands effectively, others foresee the need for radical transformations.

Shifting societal expectations often prompts tighter legal regulations. Frequently named in the interviews were the German air pollution control regulation known as the Technical Instructions on Air Quality Control (“TA Luft”) and the revised Fertilizer Application Ordinance (“DüV”). Such anticipated changes in regulations are expected to prompt a decline in livestock numbers by up to 50%. According to some experts, comprehensive transformation of animal husbandry requires significant state subsidies due to costs that exceed market coverage. The absence of a definite political framework and prospects, particularly for agricultural businesses, is an ongoing issue of stakeholder concern. This uncertainty has resulted in decreased investment activity, succession planning concerns, and imminent business closures, according to stakeholders.

On the one side, there is increasing demand for sustainability and animal well-being. On the other side, there is ongoing pressure for low prices and large-scale supply. Stakeholders stress that they have to meet the demands of large retailers reliably. They have to supply large quantities of good quality at “reasonable prices”. If they do not, they quickly risk being replaced by other suppliers, even from abroad. Almost all interviewees acknowledge the significant competitive pressure, both nationally and internationally. Several experts caution that the strategic emphasis on “cost leadership” might not be sustainable anymore due to limited potential for further cost reduction at current sites. It is expected that Germany’s cost leadership will weaken against Spain, the USA, and Brazil. The interviewees state that there is a lack of new market entrants. Intensified competition rather leads to market closure, displacement, further acquisitions, or mergers, particularly among smaller slaughterhouses. Stakeholders confirm that the focus on pure price competition demands great efforts for ever-shrinking margins. The labor market experiences intensified competition as well. According to stakeholders, labor shortages affect enterprises in different ways. Revenue generation and growth of enterprises in the field are impacted by labor shortage. Hiring is difficult due to image-related obstacles, which make it challenging to attract academically trained workers. This relates the challenges of competition to the challenges of shifting societal expectations.

In expert perspective, the rise of alternative proteins (insect-based, plant-based, or cell-based) raises even more fundamental questions about the future relevance of animal-friendly meat production. Some experts believe that the positive agglomeration effects that result from the concentration of agricultural and food companies could position the region as an alternative protein production hub. Yet, realizing this potential demands substantial education and investment. Experts are concerned that decision-makers underestimate the relevance of the new technologies, potentially leading to a regional lag. Conversely, doubts are raised as to whether the region’s structure is appropriate for producing alternative proteins, especially when considering the distinct requirements of cell-based protein manufacturing. The potential technological breakthroughs in cellular agriculture might pose a challenge for established companies.

To address these challenges and deal with the transformation pressure, stakeholders adopt various strategies. provides an overview of which industries along the value chain have been related to which strategies in the interviews.

. Strategies (horizontal axis) of adaptation and transformation attributed to industries at different stages of the value chain.

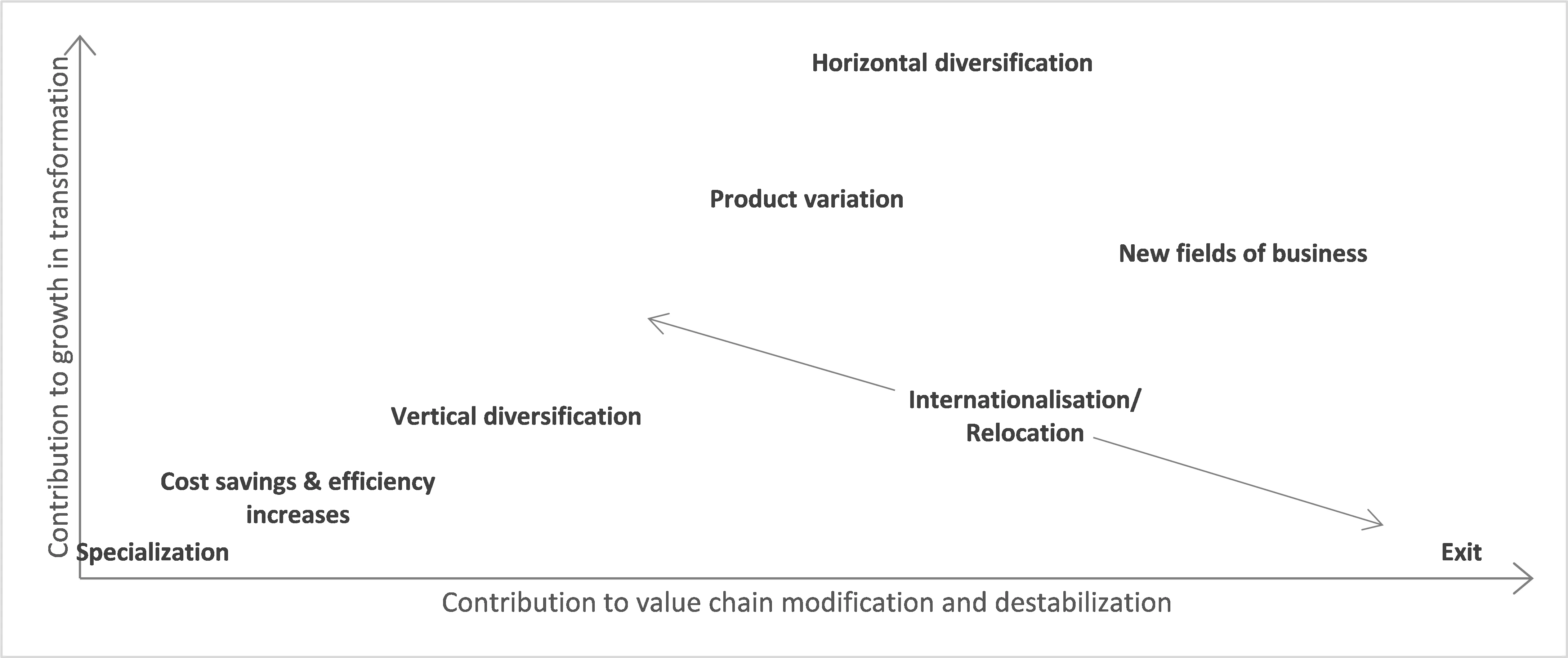

As indicated, these strategies can be grouped into those that tend to stabilize the existing SAF (cost reduction and efficiency improvement, specialization and technological innovation, vertical diversification, internationalization without relocation), modify it (product variation, horizontal diversification, and radical innovation) or destabilize it (entering new business fields, internationalization with relocation). The growth-oriented interviewees do not consider the destabilizing exit strategy.

4.3.1. Field Stabilizing Strategies

Nearly half of the experts view optimizing existing production systems as a viable path. Stakeholders in animal husbandry, slaughter, butchering, and meat processing highlight ongoing efforts in cost reduction and efficiency improvement. Significant investments in facilities, production technologies, and housing systems are made to achieve economies of scale and optimize operational processes. “Automation” and “robotization” are leveraged for cost and labor savings, enhancing energy management.

Specialization (in niche markets) and intensive technological innovations in these specific fields have been observed in businesses engaged in barn equipment, agricultural and land technology, animal health, egg products, slaughter, and meat processing. Some companies are focusing on producing high-quality, locally-sourced products, catering to “specific demands”. Many experts point to a single medium-sized slaughterhouse in this respect. It promotes alternative husbandry practices with “good animal welfare conditions”, the processing of “specific breeds” such as the Bentheimer pig, and implementing comprehensive cross-stage traceability of animal data. A traditional sausage manufacturer collaborates with this slaughterhouse. Originally launched as an online platform for sausages and meat products, the brand has since expanded to encompass two physical outlets. Another company provides end-to-end automation solutions customized for the food and feed industry, such as project planning, software development, commissioning, and post-sales services. Its exceptional specialization and expertise in the field distinguish it from competitors, especially in the software sector, according to its representative.

Other businesses supply additional products. Almost all of the firms surveyed expressed their intention to expand their product range. Examples in the consumer goods field include the development of innovative convenience products or improved recipes customized to suit the retail industry’s preferences. A major slaughter company headquartered in NRW has launched an animal welfare initiative. This program collaborates with selected farmers via contractual agreements to market pigs raised in alternative husbandry environments but contributes only minimally to total revenue as the company seems to be unable to scale it up, according to expert assessment. Companies in the agricultural trade diversify into the production of additives, animal health products, and other chemical substances. Other suppliers often offer new products and services in response to new demands on the buyer side as well. Mixed feed producers, for example, create feed formulations that reduce nitrogen and phosphorous content in the excrements. Similarly, collaboration with business partners can lead to new developments or additional products. In that case, mixed feed producers may include locally sourced protein plants or processed animal protein from beneficial insects in feed for pigs and poultry.

Vertical diversification pathways emerge among feed and pharmaceutical industries, animal husbandry, slaughter as well as the processing and packaging sectors. Experts describe increased vertical integration in the largest slaughter and meat processing enterprises in Germany. Most of them have undergone a partial integration of the processing, production, sausage manufacturing, and packaging stages. Sometimes, acquisitions serve diversification. The largest German slaughter company, for example, acquired the leading domestic sausage producer, increasing its vertical integration. It now operates as a principal supplier and simultaneously as a competitor to specialized sausage producers.

Additionally, slaughter and processing companies are increasingly entering the livestock trading market. Pig farms exhibit an increased interest in vertical integration, while the poultry sector has long embraced near-complete integration. Farmers also experiment with direct marketing of products via on-farm or online outlets. Online marketing is supported by innovative software solutions providing integrated logistics and direct marketing tools. External developers are showing increasing interest in this sector. Modernized agricultural operation services can effectively support the vertical integration of farms.

According to experts, businesses involved in poultry meat and egg production, agricultural technology, slaughter, processing, disassembly, livestock equipment, and biogas plants have expanded their export activities or entered new international markets prior to the onset of COVID-19. In line with this, most of the stakeholders interviewed report that they are also involved in international markets as their companies grow. Investment strategies often focus on modernizing in Germany and expanding internationally. Internationalization is often perfectly aligned with the “old” SAF.

4.3.2. Field Modifying Strategies

According to many experts, however, there still is a strong sense of “local commitment” even among companies with strong international aspirations, specifically among the many family-owned businesses. Nevertheless, experts also acknowledge that these regional ties may weaken in the medium and long term. Generational transitions, where companies might be sold to others, could be specifically critical in this respect. Some experts believe that a relocation of companies may then negatively affect the agricultural sector. From the reversed perspective, the strong agricultural sector is considered a “testing ground” for businesses from other sectors of the value chain who might, therefore, be negatively affected by a decline in farming. This is confirmed by some company representatives. Other stakeholders choose to keep production local because they see precise knowledge of local markets and regulations, as well as the expertise concentrated in the local labor market, as a major competitive advantage. This does not mean that they are not active in international markets.

Horizontal diversification is are alternative response to transformative pressure. Broadening the field of activity is generally considered advantageous by stakeholders, as it increases the appeal to potential business collaborators and buffers risks of individual markets. Some farms are diversifying into other livestock or crop production, tourism, or energy. This includes innovative diversifications, for example, via the cultivation of algae, quinoa, and protein crops, the construction of elevated platforms for poultry farming, and collaboration on chicken recognition technology. Sometimes diversification is also triggered by legislative changes, such as the ban on hen cage farming.

According to experts, the meat processing sector could gain strength with disruptive innovation in the field of alternative protein sources and plant-based meat substitutes even though the market is still niche, having challenges related to scalability, suitable nutrients, and consumer approval. One traditional sausage manufacturer from the SAF is regarded as a “pioneer” in this respect. The company has adapted to changing consumer demands by “streamlining” its existing product range while simultaneously exploring alternative avenues. In 2013, the company launched vegetarian and vegan product lines, which are now among the leaders in the segment in Germany. At first, traditional sausage manufacturers perceived this move towards plant-based options as “betrayal” according to experts. However, witnessing the success of these alternatives convinced them to follow suit and explore plant-based protein processing. A major slaughter firm in NRW, which previously focused on vertical integration, now operates a separate plant-based product division, producing vegetarian and vegan meat alternatives. Some meat processors have relabeled themselves as “protein producers”. A leading German poultry breeder and processor from the SAF launched a vegan brand in 2015 to penetrate the alternative protein sector. The company has secured distribution rights for plant-based egg substitutes from a U.S. firm for the European market. They also invest in venture capital with promising start-ups in niches like cell-cultured meat, vegan fish, insect-based burgers, and plant-based goods. Additionally, they established a joint venture with a globally active fund that focuses on plant-based food firms, intending it to be their production and distribution arm in Europe. The production facilities for alternative proteins of this company have been established outside the region due to more favorable conditions and, probably, subsidies there.

4.3.3. Field Destabilizing Strategies

Although meat and sausage manufacturers can utilize some of their specific competencies for advancements in alternative meat products, the development may lead to reduced value-depth in the SAF as livestock-farming and upstream industries like stall construction and technology could ultimately become redundant. The transformation towards alternative proteins is contingent on regional conditions and requires government support to foster research tasks in the area, according to experts and stakeholders in the SAF.

Prior knowledge is also crucial for new business field establishment, as witnessed by a business representative who was surprised by the complexity and volatility of a market that was previously unfamiliar to her. This company then decided to further specialize in its initial market. There are, however, success stories in new business field establishments. The large poultry breeder that has diversified into alternative proteins also ventured into the human and animal “health” sector. However, these subsidiary companies are also not located within the SAF region. A stall maker from the SAF invested in digital support for advanced control systems, transitioning from a provider of components to a centralized data hub. A leading agricultural machinery company launched a “Company Builder” aimed at AI-driven digital agribusiness models. The headquarters of this new venture is situated in a neighboring metropolis, attracting digitalization talent better than the rural SAF region. Some companies have diversified beyond their agricultural origins. An automation developer has expanded beyond animal nutrition controls, and a decentralized energy supplier has transitioned from its agricultural roots into an international combined heat and power system developer. Principally, strategies like radical innovation and new business field establishment tend to result in relocation. For internationalization, this may be specifically true if it responds to legal limitations and the decline of the domestic market.

Farmers and mixed feed producers seem to move into new business fields rarely. In the interviews, one feed and pharmaceutical manufacturer based in Lower Saxony stood out for the expansion of its product range, even branching out into a new market segment within the region. Farmers could potentially shift towards becoming “landscape managers” according to experts. The transition from animal husbandry would then have to be guided by advisory bodies, such as agricultural chambers, from the expert perspective.

5. Discussion

The findings from the interviews confirm that the SAF has to undergo a transformative process to ensure its continued viability and sustained contribution to regional growth. The interviews have also demonstrated that the different stakeholders pursue different strategies within this context. The potential of these strategies to contribute to value chain transformation and regional growth in transformation remains to be discussed. We do this here within our conceptual framework, considering expert assessments of the regional growth regime. These assessments confirm the ambiguity of tight networks of ‘old’ industries and their environment for growth and transformation (compare Chapter 1).

While a minority of the experts and stakeholders attribute the ongoing concentration process within the livestock and meat sector to the scale-dependent growth of livestock farming and meat processing as mutually dependent industries (see ), the prevailing sentiment among local experts emphasizes the creation of valuable resources during this concentration process. These experts highlight shared expertise in diverse fields such as livestock farming, facility construction, veterinary medicine, and machinery manufacturing, which collectively contribute to the region’s competitiveness. This integration is seen as fostering knowledge exchange and enhancing overall competitiveness within the SAF.

However, aligned with the understanding of livestock concentration as a scale-driven growth process, strategies emphasizing cost reduction and efficiency improvement dominate primary activities in the value chain (see ). This strategic focus on cost-leadership is deemed essential to maintain competitiveness in the globalized meat sector, according to insights from the interviews. The SAF is recognized as an innovative cluster where continuous innovation is imperative to sustain cost-leadership, aligning with the sector’s competitive dynamics. Simultaneously, there is a consensus among experts and stakeholders that the current SAF, primarily oriented towards cost leadership, might be insufficient to contribute to sustainable regional growth in the face of escalating international competitive pressures as well as new societal demands, evolving regulations, and potential disruptions from innovations in alternative proteins.

As transformation pressures intensify, strategies centered around the stabilization or conservation of existing practices may become counterproductive for perpetuating growth during transformation, as depicted in . Attempting to conserve the old SAF is recognized as a risky proposition, given the anticipated radical changes in the business environment.

. Regional growth in transformation and value chain modification/destabilization depending on stakeholder strategies.

On the other side, the interviews highlight that strategies of radical change can destabilize the SAF, putting its existing strengths at risk (see ). The emergence of new business fields, such as alternative proteins or animal pharmaceuticals, is discussed, revealing that these ventures may not necessarily benefit from the advantages of the existing SAF. New skill requirements may drive the relocation of new branches of established companies, possibly in the context of internationalization, and challengers in fields like cell-based meat alternatives may choose not to establish themselves within the region. Consequently, from a regional perspective, disruptive innovations, the market-entry of new challengers, and radical re-orientations by incumbents bear considerable risks for future growth when the existing SAF faces substantial pressure.

Required are strategies that transform the value chain in a way that meets the new challenges while preserving the specific competitive advantages that the location has gained. The greatest opportunity for this lies in strategies like product variation and horizontal diversification that modify the value chain but do not completely destabilize it (see ). Then the valuable labor market resources, networks, communities of practice, and collaborative structures can be transformed but preserved and leveraged.

The ability of stakeholders to successfully apply strategies such as product variation or horizontal diversification depends on the nature of the most valuable resources and the dynamic capabilities within their businesses and industries. Stakeholders primarily involved in livestock and meat production have often pursued cost-reduction strategies for several decades, often relying on very specific resources. Given their lack of multifunctional capacities and capabilities, they continue to prioritize responding to competitive pressures by improving technical efficiency and implementing technological solutions to meet new societal demands. In this context, the viability of the SAF is perceived to be intimately tied to the livestock sector, and a decline in livestock farming is viewed as a direct threat to the existence of the SAF.

Conversely, experts and stakeholders from businesses and industries possessing dynamic capabilities for transformation prioritize challenges arising from societal demands and potentially disruptive innovations over competitive pressures. For these actors, a focus on price competition is considered economically unsustainable, leading them to explore alternative strategies. These businesses exhibit a greater willingness to deviate from established development paths. Large companies with substantial management capacity and access to strategic resources, as well as medium and high-tech companies with flexibility, play a pivotal role in driving such transformative efforts. These participants in the field that are crucial for transformation often belong to support activities within the meat value chain (compare ). The slaughtering sector, in contrast, is dominated by large international corporations and could contribute to the transformation of the value chain but may prefer strategies of internationalization and relocation that would rather contribute to its further destabilization.

The interviews also suggest an alliance between incumbents in the livestock sector facing the challenges of significant reorientation and representatives of public authorities closely linked to agriculture. Highlighting the disadvantages of tight networks, this alliance tends to support solutions that stabilize the existing SAF rather than changing it for the sake of a successful transformation because the transformation could indeed hurt the core industries of the value chain the most. If the representatives of the ‘old’ core industries succeed in preventing transformation and structural change, it will be to the detriment of the location’s competitive advantage in the medium and long term.

In either case, it appears probable that the region may no longer host the core industries of the transformed field in the future. The SAF would then lose its regionally integrated character. This would not be unusual if one looks at other value chains. For example, in Germany, many rural, high-growth locations benefit from a high density of automotive suppliers, even if the major automakers themselves are located elsewhere. Valuable resources and dynamic capabilities can also be shared between companies in locations that do not cover entire value chains but specialize in certain stages of the value chain.

In summary, the discussion section sheds light on the contested nature of current growth mechanisms within the SAF, the imperative for transformation, and the divergent strategies pursued by stakeholders in response to evolving challenges. It highlights the specific value of networks and collaboration, as well as their potential downsides during transformation. And it also suggests that there may be losers in the transformation process; but if these potential losers manage to preserve the status quo, it will be to the detriment of the entire region. In any case, the economic character of the value chain, which has been of paramount importance to the region, is likely to change significantly in the medium and long term.

6. Conclusions

This study has investigated the preconditions for the transformation of a region with an established resource-dependent industrial core under severe transformation pressure from an actor-centered perspective. It has asked which stakeholders possess the will, resources, and capabilities to transform both their businesses and the regional economy, thereby stabilizing the local growth regime amidst severe disruption. Based on interviews with stakeholders and experts, we explored the potential transformations of livestock value chains in a region characterized by an exceptionally concentrated livestock and meat sector. The conceptual framework guiding the study was derived from resource-based and dynamic capability theories at the micro level, complemented by the concept of Strategic Action Fields (SAF) at the meso level.

The interviews suggest that the development of the established livestock and meat value chain has been driven not only by scale-dependent growth but also by the creation of successful collaborations, shared labor markets, and communities of practice. However, they also revealed that it is precisely those industries at the core of the scale-driven concentration process in the livestock and meat sector whose scale-dependent or conservative strategies, if supported by their powerful networks, threaten the transformation of the SAF. At the same time, the opportunities for the livestock sector to leverage resources and skills beyond agriculture are limited due to the specific characteristics of the sector.

The characterization of the SAF as a cluster with classic dynamic capabilities and valuable transferable resources primarily aligns with support activities rather than the primary activities of the value chain. Family-owned, technology-intensive companies within these support activities exhibit strong local ties and a readiness to implement transformative strategies, including diversification and reorientation. Even if radical transformation succeeds, the region might no longer host the core industries of the transformed field. However, successful industrial SAFs need not be regionally confined, and valuable resources and dynamic capabilities can be harnessed within clusters specializing in specific stages of value chains.

Attempting to conserve the “old” SAF at all costs would likely incur substantial long-term expenses. To counter the imminent risk of losing growth potential due to lock-ins, product variation and horizontal diversification in local enterprises should be encouraged. Economic and political stakeholders in the livestock and meat sectors have to embrace new opportunities, transitioning from cost competition to innovative markets that enable higher wages and the development of future-proof competencies. Effective communication by policymakers and leading regional companies about impending transformations, alongside the provision of reliable framework conditions, is crucial. Encouraging established and emerging companies to invest in new activities is imperative, mitigating the risk of companies relocating due to skill misalignments. Educational efforts, especially in vocational schools and local universities, play a crucial role in meeting evolving business requirements. Ultimately, successful diversification depends on stable economic conditions. Thus, if possible, it is advisable to pursue the structural transformation during a positive economic phase. Failing to achieve diversification jeopardizes the unique endogenous locational advantages and diminishes future growth prospects.

The combination of micro-level theories from a management perspective with a sociologically grounded, meso-level field theory proved successful in designing the interviews, analyzing the data obtained, and drawing insightful conclusions. It should be noted, however, that there are limitations to the interview approach. The mentioned companies, farms, and stakeholders do not represent the entire value chain. Biased conclusions may arise due to the selection of certain, influential stakeholders or if strategies are not mentioned by interviewees due to their apparent self-evidence. This study was accompanied by a second study using secondary data from labor market statistics and regression-based simulations [

40]. Its results confirm that the region has considerable growth potential and that the decline of the agricultural core of the meat and livestock value chain could release resources that could then compensate for this decline in other industries. However, it remains silent on the micro-level mechanisms that drive such a favorable development. The two studies are, therefore, complementary. To address potential biases, mixed-method approaches with different data sources are recommended for all analyses of transformation processes from micro-meso perspectives.

Acknowledgments

We thank the interviewees for their participation and for their detailed and knowledgable replies to our questions. Without them, this research would not have been possible.

Author Contributions

Conceptualization, A.M., V.B. and J.E.; Interviews, V.B. and J.E.; Interview Analysis, V.B. and J.E.; Writing—Original Draft Preparation, V.B.; Writing—Review & Editing, A.M. and V.B.; Visualization, V.B. and A.M.; Project Administration, A.M.; Funding Acquisition, J.E. and A.M.

Ethics Statement

Not applicable.

Informed Consent Statement

Informed consent on the use of interview data for publication was obtained from all interviewees involved in the study.

Funding

This work was funded by the German Federal Ministry of Food and Agriculture (BMEL) based on a decision of the Parliament of the Federal Republic of Germany, granted by the Federal Office for Agriculture and Food (BLE; grant number: 28N1800005).

Declaration of Competing Interest

The authors declare that they had no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper at the time they worked in the project. Verena Beck today works for a company in the meat value chain but held a position at a university in between.

Footnotes

1. Creditreform is a company that offers, on a commercial basis, databases with information on all companies in Germany and abroad that are subject to a publication obligation.

2. The Federal Agency for Agriculture and Food, known as the “Bundesanstalt für Landwirtschaft und Ernährung” (BLE), operates under the Federal Ministry of Food and Agriculture (BMEL) and is responsible for shaping policies, supporting research, and implementing initiatives related to agriculture, food production, and rural development (https://www.ble.de/DE/Startseite/startseite_node.html).

3. The “Agrar- und Ernährungsforum Oldenburger Münsterland e. V.” (Agriculture and Nutrition Forum Oldenburger Münsterland) is an association from the region that aims to promote dialogue and collaboration within the agricultural and nutritional sectors, and between the sector and politics and the wider public. It wants to support the development of practical solutions that enhance the resilience and sustainability of rural landscapes and food systems (https://aef-om.de/).

4. The Initiative Tierwohl (ITW) is a cross-sector alliance of the German meat industry, which aims to improve the quality of life of animals in conventional poultry and pig farming by providing financial support. (https://initiative-tierwohl.de/).

5. The Lower Saxony Path is an agreement between agriculture, nature conservation and politics. The paper commits the stakeholders to implementing specific measures for improved nature, species and water protection. (https://www.ml.niedersachsen.de/download/155559/Der_Niedersaechsische_Weg_-_Broschuere_nicht_vollstaendig_barrierefrei_.pdf).

6. The Lower Saxony Evening at the International Grüne Woche is traditionally used for networking in the agricultural and food sector. Grüne Woche in Berlin is one of the leading international trade fairs for food, agriculture and horticulture. (https://www.gruenewoche.de/de/).

References

-

1.

Ashmead CP, Kelly EC. In flux: Social adaptability in two former timber towns transitioning to new economies.

J. Rural Stud. 2023,

102, 103076.

[Google Scholar]

-

2.

Liu L, Cavaye J, Ariyawardana A. Supply chain responsibility in agriculture and its integration with rural community development: A review of issues and perspectives.

J. Rural Stud. 2022,

93, 134–143.

[Google Scholar]

-

3.

Halseth G, Ryser L, Markey S, Martin A. Emergence, transition, and continuity: Resource commodity production pathways in northeastern British Columbia, Canada.

J. Rural Stud. 2014,

36, 350–361.

[Google Scholar]

-

4.

Grande J. New venture creation in the farm sector—Critical resources and capabilities.

J. Rural Stud. 2011,

27, 220–233.

[Google Scholar]

-

5.

Stotten R, Schermer M. Wilson GA. Lock-ins and community resilience: Two contrasting development pathways in the Austrian Alps.

J. Rural Stud. 2021,

84, 124–133.

[Google Scholar]

-

6.

Haley B. From Staples Trap to Carbon Trap: Canada’s Peculiar form of Carbon Lock-In.

Stud. Polit. Econ. 2011,

88, 97–132.

[Google Scholar]

-

7.

Karlsson M, Hovelsrud GK. “Everyone comes with their own shade of green”: Negotiating the meaning of transformation in Norway's agriculture and fisheries sectors.

J. Rural Stud. 2021,

81, 259–268.

[Google Scholar]

-

8.

Bui S, Cardona A, Lamine C, Cerf M. Sustainability transitions: Insights on processes of niche-regime interaction and regime reconfiguration in agri-food systems.

J. Rural Stud. 2016,

48, 92–103.

[Google Scholar]

-

9.

Vilas-Boas J, Klerkx L, Lie R. Connecting science, policy, and practice in agri-food system transformation: The role of boundary infrastructures in the evolution of Brazilian pig production.

J. Rural Stud. 2022,

89, 171–185.

[Google Scholar]

-

10.

Kungl G, Hess DJ. Sustainability transitions and strategic action fields: A literature review and discussion.

Environ. Innov. Soc. Transit. 2021,

38, 22–33.

[Google Scholar]

-

11.

Fligstein N, McAdam D. Toward a General Theory of Strategic Action Fields.

Sociol. Theory 2011,

29, 1–26.

[Google Scholar]

-

12.

Barney J. Firm Resources and Sustained Competitive Advantage.

J. Manag. 1991,

17, 99–120.

[Google Scholar]

-

13.

Teece DJ, Pisano G, Shuen A. Dynamic Capabilities and Strategic Management.

Strat. Manag. J. 1997,

18, 509–533.

[Google Scholar]

-

14.

Fligstein N, McAdam D. A Theory of Fields; Oxford University Press: Oxford, UK, 2015.

-

15.

Margarian A. The Hidden Strength of Rural Enterprises: Why Peripheries Can Be more than A City Centre’s Deficient Complements. Chapter 2. In The Rural Enterprise Economy; Leick B, Gretzinger S, Makkonen T, Eds.; Routledge: London, UK, 2022; pp 19–34.

-

16.

Dias CS, Rodrigues RG, Ferreira JJ. Agricultural entrepreneurship: Going back to the basics.

J. Rural Stud. 2019,

70, 125–138.

[Google Scholar]

-

17.

Teece DJ. Explicating Dynamic Capabilities: The Nature and Microfoundations of (Sustainable) Enterprise Performance.

Strat. Mgmt. J. 2007,

28, 1319–1350.

[Google Scholar]

-

18.

Chesbrough HW. Open Innovation: The New Imperative for Creating and Profiting from Technology, [Nachdr.]; Harvard Business School Press: Boston, MA, USA, 2010.

-

19.

Leker J, Song Ch. Die Prognose von Konvergenzentwicklungen zur Identifikation attraktiver Innovationsfelder. In Motoren der Innovation; Schultz C, Hölzle K, Eds.; Springer Fachmedien Wiesbaden: Wiesbaden, Germany, 2014; pp. 3–22.

-

20.

Grabher G. Rediscovering the social in the economics of interfirm relations. In The Embedded Firm: On the Socioeconomics of Industrial Networks, Repr; Grabher G, Ed.; Routledge: London, UK, 1993; pp. 1–31.

-

21.

Fernandez-Stark K, Gereffi G. Global value chain analysis: A Primer. In Handbook on Global Value Chains; Ponte S, Gereffi G, Raj-Reichert G, Eds.; Edward Elgar Publishing: Cheltenham, UK, 2019; pp. 54–76.

-

22.

Matheis TV, Herzig C. Upgrading products, upgrading work? Interorganizational learning in global food value chains to achieve the Sustainable Development Goals.

Ecol. Perspect. Sci. Soc. 2019,

28, 126–134.

[Google Scholar]

-

23.

Marshall A. Industry and Trade: A Study of Industrial Technique and Business Organization and of Their Influences on the Condition of Various Classes and Nations; MacMillian and Co. Limited: London, UK, 1919.

-

24.

Grabher G. Cool Projects, Boring Institutions: Temporary Collaboration in Social Context.

Reg Stud. 2002,

36, 205–214.

[Google Scholar]

-

25.

Storper M, Venables AJ. Buzz: Face-to-Face Contact and the Urban Economy.

J. Econ. Geogr. 2004,

4, 351–370.

[Google Scholar]

-

26.

Wenger E. Communities of Practice; Cambridge University Press: Cambridge, UK, 1998.

-

27.

Brown JS, Duguid P. Balancing Act: How to Capture Knowledge Without Killing It.

Harv. Bus. Rev. 2000,

78, 73–80.

[Google Scholar]

-

28.

Gertler MS. Tacit Knowledge and the Economic Geography of Context, or The Undefinable Tacitness of Being (There).

J. Econ. Geogr. 2003,

3, 75–99.

[Google Scholar]

-

29.

Malmberg A, Power D. (How) Do (Firms in) Clusters Create Knowledge?

Ind. Innov. 2005,

12, 409–431.

[Google Scholar]

-

30.

Granovetter M. The Strength of Weak Ties.

Am. J. Sociol. 1973,

78, 1360–1380.

[Google Scholar]

-

31.

Martin R, Sunley P. Path dependence and regional economic evolution.

J. Econ. Geogr. 2006,

6, 395–437.

[Google Scholar]

-

32.

McAdam D. Political Process Theory. In The Wiley-Blackwell Encyclopedia of Social and Political Movements; Della Porta D, Klandermans B, McAdam D, Snow DA, Eds.; Wiley: Hoboken, NJ, USA, 2013; pp. 1–4.

-

33.

Mooney PH. Local governance of a field in transition: The food policy council movement.

J. Rural Stud. 2022,

89, 98–109.

[Google Scholar]

-

34.

Margarian A. Strukturwandel in der Wissensökonomie: Eine Analyse von Branchen-, Lage- und Regionseffekten in Deutschland; Johann Heinrich von Thünen-Institut: Braunschweig, Germany, 2018.

-

35.

Möller J, Tassinopoulos A. Zunehmende Spezialisierung oder Strukturkonvergenz?: Eine Analyse der sektoralen Beschäftigungsentwicklung auf regionaler Ebene.

Jahrbuch für Regionalwissenschaft 2000,

20, 1–38.

[Google Scholar]

-

36.

Birke P, Bluhm F. Migrant Labour and Workers' Struggles: The German Meatpacking Industry as Contested Terrain. Glob. Labour J. 2020, 11.

-

37.

Guimarães MH. Non-Tariff Measures in The European Union: Evidence from the Agri-Food Sector.

Agric. Econ. Rev. 2012,

13, 21–34.

[Google Scholar]

-

38.

Santeramo FG. Agri-food trade and non-tariff measures.

Agrekon 2019,

58, 387–388.

[Google Scholar]

-

39.

Efken J, Osterburg B. Der Markt für Fleisch und Fleischprodukte.

Ger. J. Agric. Econ. 2018,

67, 56–75.

[Google Scholar]

-

40.

Margarian A. Analysing evolutionary growth regimes of regional economies and transformative shocks: Proposal for a regression-based counterfactual simulation approach to local inter-industry structural change.

Struct. Change Econ. Dyn. 2024,

70, 18–32.

[Google Scholar]

-

41.

Roe B, Irwin EG, Sharp JS. Pigs in Space: Modeling the Spatial Structure of Hog Production in Traditional and Nontraditional Production Regions.

Am. J. Agric. Econ. 2002,

84, 259–278.

[Google Scholar]

-

42.

Dumont B, Fortun-Lamothe L, Jouven M, Thomas M, Tichit M. Prospects from agroecology and industrial ecology for animal production in the 21st century.

Animal 2013,

7, 1028–1043.

[Google Scholar]

-

43.

Ackermann A, Heidecke C, Hirt U, Kreins P, Kuhr P, Kunkel R, et al. Der Modellverbund AGRUM als Instrument zum landesweiten Nährstoffmanagement in Niedersachsen; Johann Heinrich von Thünen-Institut: Braunschweig, Germany, 2015.

-

44.

Spiller A, Gauly M, Balmann A, Bauhus J, Birner R, Bokelmann W, et al. Wege zu einer gesellschaftlich akzeptierten Nutztierhaltung: Gutachten des Wissenschaftlichen Beirats für Agrarpolitik; Wissenschaftlicher Beirat Agrarpolitik beim BMEL, Ed.; Bundesministerium für Ernährung und Landwirtschaft (BMEL): Berlin, Germany, 2015.

-

45.

Nutztierstrategie: Zukunftsfähige Tierhaltung in Deutschland. Bundesministerium für Ernährung und Landwirtschaft (BMEL): Berlin, Germany, 2019. Available online: https://www.nationales-tierwohl-monitoring.de/fileadmin/nationales_tierwohl_monitoring/andere_pdfs/BMEL-Nutztierstrategie.pdf (accessed on 28 June 2024).

-

46.

Reinhard A, Angrick M, Bade M, Balzer F, Bertram A, Bilharz M, et al. Klimaschutzplan 2050: Klimaschutzpolitische Grundsätze und Ziele der Bundesregierung; BMU, Ed.; Publikationsversand der Bundesregierung: Berlin, Germany, 2016.

-

47.

Anker HT, Baaner L, Backes C, Keessen A, Möckel S. Comparison of Ammonia Regulation in Germany, The Netherlands and Denmark; IFRO Report No. 276, 2018.

-

48.

Gaigné C, Le Gallo J, Larue S, Schmitt B. Does Regulation of Manure Land Application Work Against Agglomeration Economies? Theory and Evidence from the French Hog Sector.

Am. J. Agr. Econ. 2012,

94, 116–132.

[Google Scholar]

-

49.

Haß M, Banse M, Deblitz C, Freund F, Geibel I, Gocht A, et al. Thünen-Baseline 2020–2030: Agrarökonomische Projektionen für Deutschland; Johann Heinrich von Thünen-Institut: Braunschweig, Germany, 2020.

-

50.

Hernández V, Pedersen T. Global value chain configuration: A review and research agenda.

BRQ Bus. Res. Q. 2017,

20, 137–150.

[Google Scholar]

-

51.

Bogner A, Menz W. Expertenwissen und Forschungspraxis: Die modernisierungstheoretische und die methodische Debatte um die Experten. In Das Experteninterview: Theorie, Methode, Anwendung; Bogner A, Littig B, Menz W, Eds.; VS Verlag für Sozialwissenschaften: Wiesbaden, Germany, 2002; pp. 7–29.

-

52.

Mayring P. Qualitative Inhaltsanalyse: Grundlagen und Techniken, Neuausgabe; Beltz Verlagsgruppe: Weinheim Basel, Germany, 2010.

-

53.

Mayring P, Fenzl T. Qualitative Inhaltsanalyse. In Handbuch Methoden der Empirischen Sozialforschung; Baur N, Blasius J, Eds.; Springer Fachmedien Wiesbaden: Wiesbaden, Germany, 2019; pp. 633–648.